PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066454

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066454

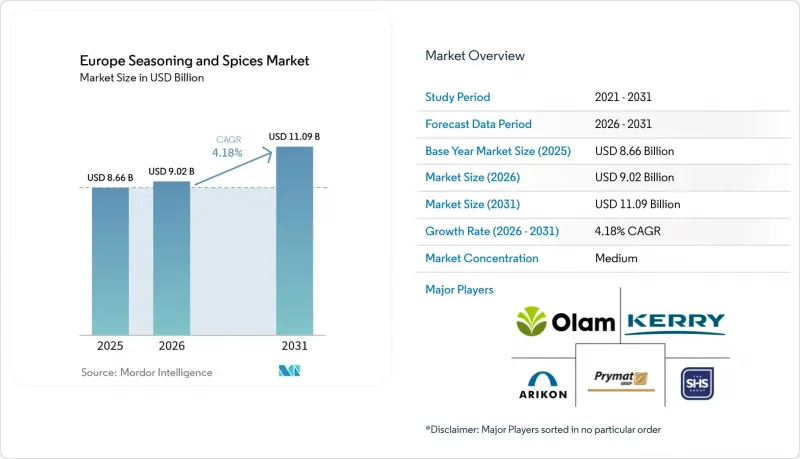

Europe Seasoning And Spices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe seasoning and spices market size was valued at USD 8.66 billion in 2025 and estimated to grow from USD 9.02 billion in 2026 to reach USD 11.09 billion by 2031, at a CAGR of 4.18% during the forecast period (2026-2031).

This report is Segmented by Type (Salt and Salt Substitutes, Herbs and Seasonings, and Spices), Category (Conventional and Organic), Application (Bakery and Confectionery, Soup, Noodles, and Pasta, Meat and Seafood and Others), and Geography (United Kingdom, Germany, France, Italy, Spain, and More). The Market Forecasts are Provided in Terms of Value and Volume (USD/Tonnes).

Europe Seasoning And Spices Market Trends and Insights

Expanding Consumer Demand for Healthier and Better-Quality Ingredients

European consumers increasingly view spices as functional ingredients with health benefits beyond flavoring. Turmeric (for anti-inflammatory properties), ginger (for digestive health), and cinnamon (for blood sugar regulation) experience growing demand. This consumer perception enables premium pricing for spices with verified potency levels. Single-estate turmeric with higher curcumin concentrations commands a 40% price premium compared to commodity-grade variants. German consumers drive this trend, with organic spices sales experiencing significant annual growth due to demand for pesticide-free certification and supply chain transparency. The health and wellness positioning elevates spices from commodity items to premium health products, enabling margin growth across the value chain. European Food Safety Authority (EFSA) health claim approvals provide regulatory support for functional spice marketing, while ISO 22000 food safety standards serve as baseline requirements for health-oriented products.

Increasing Adoption of Multicultural Diet Patterns and International Cuisines

Migration patterns and tourism have reshaped European food preferences, transforming consumer behavior across major metropolitan areas. Urban centers in Germany, France, and the Netherlands demonstrate strong adoption of Middle Eastern (baharat, za'atar), North African (harissa, ras-el-hanout), and Asian (gochujang, miso-based) seasoning blends. The trend extends beyond immigrant communities, as European consumers incorporate global flavors influenced by social media content and international travel experiences. Restaurant chains now offer fusion dishes combining traditional European techniques with international spice profiles, driving mainstream demand for previously specialty ingredients. This shift has led to premiumization in the market, with authentic imported spice blends commanding substantial price premiums compared to standard European seasonings.

Stringent and Complex Regulatory Requirements

The European Union Deforestation Regulation (EUDR), taking effect in 2024, introduces comprehensive supply chain traceability requirements for spice imports. This regulation imposes substantial compliance costs on affected suppliers, impacting their operational expenses and profit margins. The requirements particularly affect pepper, cinnamon, and nutmeg imports from Southeast Asia, where smallholder farming operations lack GPS-verified deforestation-free certification. The Corporate Sustainability Reporting Directive (CSRD) requires companies operating in the EU to report environmental and social impacts throughout their supply chains, resulting in increased administrative and audit expenses. These regulations benefit larger companies with existing compliance systems while creating entry barriers for smaller importers and specialty spice traders. The regulatory requirements accelerate market consolidation as smaller operators either exit the market or become acquisition targets for larger, compliant companies.

Other drivers and restraints analyzed in the detailed report include:

- Trend Toward Organic and Clean-Label Spices and Seasonings

- Growth in Convenience, Ready-to-Cook, and Processed Foods Industries

- Limited Availability of Organic and Sustainably Sourced Raw Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The European food ingredients market demonstrates a significant shift toward healthier alternatives, with salt and salt substitutes commanding a substantial 36.88% market share in 2025. This trend directly correlates with increasing consumer awareness about hypertension and its health implications. Kerry Group's innovative Tastesense Salt technology has emerged as a notable solution in this segment, successfully reducing sodium content by 50% while preserving the desired taste profile through a combination of potassium chloride and natural flavor enhancers.

The herbs and seasonings segment exhibits robust growth prospects, with projections indicating a 5.49% CAGR through 2031. This growth is primarily attributed to increasing consumer preference for clean-label products and their associated health benefits. Traditional Mediterranean herbs, including thyme, basil, and oregano, continue to gain market traction, while mint has evolved beyond conventional applications to establish a strong presence in the functional beverages and wellness products categories, reflecting broader consumer health trends.

List of Companies Covered in this Report:

- SHS Group

- Prymat Group

- Olam International

- Kerry Group PLC

- Arikon Group

- Sensient Technologies Corporation

- Dohler GmbH

- Kalsec Inc.

- Nedspice Group

- Solina Group

- McCormick & Company Inc.

- Ajinomoto Co. Inc.

- Fuchs Gruppe

- Bart Ingredients Co. Ltd.

- La Doria S.p.A.

- Verstegen Spices & Sauces B.V.

- Wiberg GmbH

- Givaudan S.A.

- Kotanyi GmbH

- EVG Spices

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding consumer demand for healthier and better-quality ingredients

- 4.2.2 Increasing adoption of multicultural diet patterns and international cuisines

- 4.2.3 Trend toward organic and clean-label spices and seasonings

- 4.2.4 Growth in convenience, ready-to-cook, and processed foods industries

- 4.2.5 Focus on sustainable and eco-conscious sourcing methods

- 4.2.6 Tourism and migration are broadening palate preferences

- 4.3 Market Restraints

- 4.3.1 Stringent and complex regulatory requirements

- 4.3.2 Limited availability of organic and sustainably sourced raw materials

- 4.3.3 Technical challenges in formulating new spice blends without compromising flavor

- 4.3.4 Challenges with shelf life, stability, and sensory quality

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Type

- 5.1.1 Salt and Salt Substitutes

- 5.1.2 Herbs and Seasonings

- 5.1.2.1 Thyme

- 5.1.2.2 Basil

- 5.1.2.3 Oregano

- 5.1.2.4 Parsley

- 5.1.2.5 Mint

- 5.1.2.6 Other Herbs and Seasonings

- 5.1.3 Spices

- 5.1.3.1 Pepper

- 5.1.3.2 Sesame

- 5.1.3.3 Cinnamon

- 5.1.3.4 Mustard

- 5.1.3.5 Onion

- 5.1.3.6 Garlic

- 5.1.3.7 Paprika

- 5.1.3.8 Chili Pepper

- 5.1.3.9 Other Spices

- 5.2 By Category

- 5.2.1 Organic

- 5.2.2 Conventional

- 5.3 By Application

- 5.3.1 Bakery and Confectionery

- 5.3.2 Soup, Noodles, and Pasta

- 5.3.3 Meat and Seafood

- 5.3.4 Sauces, Salads, and Dressing

- 5.3.5 Savory Snacks

- 5.3.6 Other Applications

- 5.4 By Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 Italy

- 5.4.4 France

- 5.4.5 Spain

- 5.4.6 Netherlands

- 5.4.7 Poland

- 5.4.8 Belgium

- 5.4.9 Sweden

- 5.4.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SHS Group

- 6.4.2 Prymat Group

- 6.4.3 Olam International

- 6.4.4 Kerry Group PLC

- 6.4.5 Arikon Group

- 6.4.6 Sensient Technologies Corporation

- 6.4.7 Dohler GmbH

- 6.4.8 Kalsec Inc.

- 6.4.9 Nedspice Group

- 6.4.10 Solina Group

- 6.4.11 McCormick & Company Inc.

- 6.4.12 Ajinomoto Co. Inc.

- 6.4.13 Fuchs Gruppe

- 6.4.14 Bart Ingredients Co. Ltd.

- 6.4.15 La Doria S.p.A.

- 6.4.16 Verstegen Spices & Sauces B.V.

- 6.4.17 Wiberg GmbH

- 6.4.18 Givaudan S.A.

- 6.4.19 Kotanyi GmbH

- 6.4.20 EVG Spices

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK