PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066474

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066474

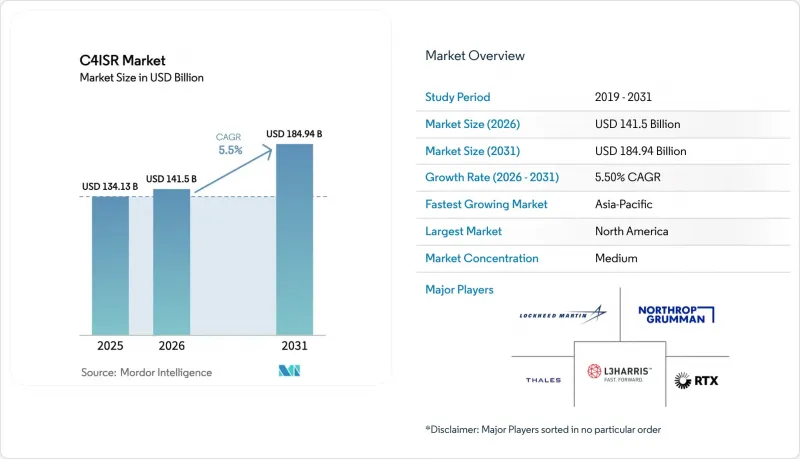

C4ISR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the C4ISR market size is expected to grow from USD 134.13 billion in 2025 to USD 141.50 billion in 2026 and is forecasted to reach USD 184.94 billion by 2031 at a 5.50% CAGR over 2026-2031.

This report is Segmented by Platform (Air, Land, Naval, and Space), Purpose (C4, ISR, and EW), Component (Hardware, Software, and Services), Installation Type (New Installation and Upgrade/Retrofit), End User (Defense and Military, and Government and Law Enforcement), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global C4ISR Market Trends and Insights

Multi-Domain C2 Programs Accelerate Interoperable C4ISR Deployments

The C4ISR market is being reshaped by joint all-domain command and control programs that connect sensors, decision-makers, and effectors across air, land, sea, space, and cyber. In fiscal 2025, the Department of Defense (DoD) requested over USD 1.4 billion for CJADC2, signaling a distinct, sustained budgetary priority for cross-service integration and decision superiority. The Government Accountability Office reported that while the effort is progressing, DoD must improve governance, lesson sharing, and data standardization to reduce duplicative work and accelerate fielding. These programs also depend on secure, scalable cloud infrastructure and upgrades to classified networks to move and process data at speed. The near-term effect on the C4ISR market is visible in demand for gateways, multi-waveform radios, cross-domain solutions, and fusion software that can operate across classification levels and coalition boundaries. As formal doctrine and infrastructure converge, JADC2-aligned architectures will increasingly influence interface standards and procurement choices in the C4ISR market.

Proliferation of Unmanned and Autonomous Platforms Increases Sensor and Data-Link Density

Unmanned systems amplify the number of sensors, data links, and decision nodes that C4ISR networks must support in contested environments. US budget allocations identify continued funding for unmanned aircraft and maritime platforms, with line items that emphasize autonomy, perception, and C2 resiliency as core mission requirements rather than optional add-ons. NATO's 2026 launch of new multinational cooperation initiatives includes a drone-based deep precision strike project that will require interoperable command, control, and data exchange across allied forces. As unmanned fleets grow, the C4ISR market faces rising demand for mesh networking, spectrum-aware communications, and edge analytics that push more processing closer to the platform. The integration of counter-UAS capabilities further underscores the need for automated sensor fusion and fire control logic operating at machine speed to manage swarms and simultaneous threats. These factors collectively expand software, gateway, and training needs across the C4ISR market in the medium term.

Integration Complexity and Data Interoperability Across Legacy and Coalition Systems

Complex integration remains the most persistent brake on deployment speed and budget efficiency in the C4ISR market. GAO's review of CJADC2 identified the need for stronger governance, shared lessons learned, and common data standards across services to avoid duplication and accelerate outcomes. Coalition operations introduce policy and technical frictions that require cross-domain solutions, compatible data formats, and classification pathways that enable timely sharing with allies. Without common frameworks, programs spend disproportionate effort on middleware, test events, and workarounds, delaying delivery of operational capability. The near-term remedy is targeted investment in interfaces, gateways, and standardized schemas anchored to program governance that enforces data discipline. As solutions take hold, the C4ISR market will benefit from faster time-to-field and broader vendor participation across joint programs.

Other drivers and restraints analyzed in the detailed report include:

- Space-Based ISR and SATCOM Architectures Shift to LEO/MEO with Resilient Mesh Networking

- Open Architectures (MOSA/CMOSS/SOSA) Enable Rapid Tech Insertion

- Cyber and EW Resilience Requirements Increase Cost, Schedule, and Accreditation Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air platforms held 35.92% shares in 2025, supported by ongoing upgrades to sensor fusion, long-range sensing, and networked targeting across leading fleets. Select retrofit programs illustrate an upgrade-first approach that installs advanced search-and-track and multi-sensor capabilities into existing aircraft without major structural changes, aligning with the efficiency focus in the C4ISR market. A growing share of the air segment is software-led, in line with multi-domain C2 efforts that require common operating views, machine-assisted targeting, and gateway capabilities. The C4ISR market is also seeing demand shift toward agile pods, open-architecture mission computers, and edge inference accelerators that unlock new algorithms without whole-aircraft redesign. Airborne networking and cross-domain data exchange requirements continue to drive procurement of multi-waveform radios and gateways that support joint fires. As integration improves, the segment will lean into open standards that lower lifecycle costs and speed iteration across diverse fleets. Program choices indicate steady refresh cycles will favor modular, software-forward upgrades across the 2026-2031 horizon.

Naval platforms are the fastest-growing with a CAGR of 7.58% through 2031, driven by persistent maritime ISR, distributed operations, and electronic protection across surface, subsurface, and coastal defense layers. The C4ISR market is registering stronger growth for maritime mesh networking, common combat system backbones, and spectrum-aware solutions that manage dense littoral environments. Programs in allied navies are also adopting modular standards that allow radar, sonar, EW payloads, and communications to be upgraded without major hull changes. This growth trend is reinforced by joint exercises that validate ashore-aboard data exchanges and over-the-horizon fire control, which depend on resilient command-and-control architectures at sea. As unmanned surface and underwater vehicles proliferate, maritime C4ISR programs will integrate more autonomy, perception, and anti-jam links into distributed kill chains. The result is a predictable cadence of software and module insertions that sustain the naval portion of the C4ISR market.

ISR represented the largest share of 43.67% in 2025, reflecting the central role of sensing, collection, and processing across air, space, land, and maritime missions. The C4ISR market is benefiting from ISR's pivot to faster revisit, lower latency, and broader spectral coverage, supported by multi-orbit space investments and open-architecture payloads. ISR demand is also rising on the ground and at sea, where border security, maritime domain awareness, and base defense require persistent detection and multi-sensor fusion. Cross-cueing between RF, EO/IR, and radar, with prioritized alerts to commanders, is now a threshold capability for ISR architectures. Allied programs emphasize interoperable ISR that can be shared at releasable levels, which influences terminal and gateway requirements. Over the forecast period, ISR software that fuses heterogeneous data at the edge will underpin capability growth across the C4ISR market.

Electronic warfare (EW) is the fastest-growing purpose segment, with a 6.77% CAGR through 2031, and its focus areas span sensing, protection, and effects in contested electromagnetic environments. Army guidance calls for modular, scalable, and adaptable EW technologies that are integrated coherently to enable machine-speed decision-making and dynamic spectrum operations, driving investment in software-defined radios, agile antennas, fast-tuning receivers, and resource managers that allocate RF components in real time. EW and cyber are increasingly converging, which elevates the need for secure-by-design firmware, continuous reprogramming, and rapid accreditation cycles. The C4ISR market is seeing stronger demand for counter-UAS capabilities that combine passive detection, electronic defeat, and integration into command-and-control workflows. The trajectory points to embedded EW across platforms and formations with open module standards that compress time-to-field.

Geography Analysis

North America held the largest share, at 33.11%, in 2025, supported by sustained US investment in multi-domain command and control, next-generation ISR, and protected communications. The scale and cadence of program funding set technical baselines that influence allied procurements and integration choices in the C4ISR market. US oversight bodies continue to emphasize governance and standards that enable joint deployment of interoperable capabilities, which shapes how vendors approach product roadmaps. Canada's spectrum management and resilience challenges signal complementary demand for unified electromagnetic operating pictures and dynamic deconfliction tools. As joint architectures mature, demand will consolidate around standards that make coalition operations more effective, policies more workable, and training more consistent across North America. The region's vendor ecosystem, spanning primes, specialized suppliers, and software firms, remains a catalyst for innovation in the global C4ISR market.

Europe is in a multi-year modernization phase that prioritizes interoperable ISR, multi-orbit communications access, and coalition-ready C2. NATO's 2026 multinational cooperation initiatives focus on ballistic missile defense enablers, drone-enabled precision strike, and airpower resilience and interoperability, all of which reinforce requirements for secure, shareable, and modular C4ISR. European programs reflect a broadening use of open standards and software-defined functions to speed capability delivery and strengthen industrial participation across allies. Border security, coastal surveillance, and air defense upgrades on Europe's eastern flank underscore the urgency of procurement. Over the period, European programs are expected to deepen links with US architectures where policy allows, while growing native capacity in sensors, terminals, and mission software. Vendors that can meet European preferences for modularity and releasable interoperability will be well-placed in the region's C4ISR market.

Asia-Pacific is poised for the fastest growth of 7.93% through 2031 as regional actors invest in ISR integration, resilient communications, and maritime C2. Programs in Japan and South Korea show increased emphasis on airborne early warning, networked command centers, and mission systems aligned with joint operations concepts. As regional forces scale autonomous systems and maritime ISR, requirements for data fusion, anti-jam waveforms, and multi-orbit terminal solutions will expand. Suppliers are also forming partnerships that combine mission systems with indigenous platforms to accelerate fielding and localized sustainment. Across the region, growth in the C4ISR market will follow the adoption of open architectures, releasable security frameworks, and test-and-evaluation pipelines that can certify complex integrations at speed. Countries that align with multi-domain standards will benefit from broader ecosystems of interoperable products and services.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- RTX Corporation

- Thales Group

- BAE Systems plc

- L3Harris Technologies, Inc.

- General Dynamics Corporation

- Leonardo S.p.A.

- Saab AB

- Elbit Systems Ltd.

- Israel Aerospace Industries Ltd.

- Airbus SE

- HENSOLDT AG

- The Boeing Company

- CACI International Inc.

- Maxar Technologies Holdings Inc.

- Kratos Defense & Security Solutions, Inc.

- Defense Research and Development Organisation (DRDO)

- Hanwha Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 NATO rearmament and modernization raise digital command, ISR, and secure comms demand

- 4.2.2 Multi-domain C2 programs (JADC2/CJADC2, ABMS) accelerate interoperable C4ISR deployments

- 4.2.3 Proliferation of unmanned and autonomous platforms increases sensor and data-link density

- 4.2.4 Space-based ISR and SATCOM architectures shift to LEO/MEO with resilient mesh networking

- 4.2.5 Open architectures (MOSA/CMOSS/SOSA) enable rapid tech insertion and shift spend to software/services

- 4.2.6 Edge AI/ML and cloud-to-tactical fusion compress kill chain and drive upgrade cycles

- 4.3 Market Restraints

- 4.3.1 Integration complexity and data interoperability across legacy/coalition systems

- 4.3.2 Cyber/EW resilience requirements increase cost, schedule, and accreditation burden

- 4.3.3 Export controls/ITAR and security of supply limit cross-border C4ISR sharing

- 4.3.4 Spectrum congestion and EMSO deconfliction constrain networked operations

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform

- 5.1.1 Air

- 5.1.2 Land

- 5.1.3 Naval

- 5.1.4 Space

- 5.2 By Purpose

- 5.2.1 Command, Control, Communications, and Computer (C4)

- 5.2.2 Intelligence, Surveillance, and Reconnaissance (ISR)

- 5.2.3 Electronic Warfare (EW)

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software

- 5.3.3 Services

- 5.4 By Installation Type

- 5.4.1 New Installation

- 5.4.2 Upgrade/Retrofit

- 5.5 By End User

- 5.5.1 Defense and Military

- 5.5.2 Government and Law Enforcement

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 France

- 5.6.2.3 Germany

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Lockheed Martin Corporation

- 6.4.2 Northrop Grumman Corporation

- 6.4.3 RTX Corporation

- 6.4.4 Thales Group

- 6.4.5 BAE Systems plc

- 6.4.6 L3Harris Technologies, Inc.

- 6.4.7 General Dynamics Corporation

- 6.4.8 Leonardo S.p.A.

- 6.4.9 Saab AB

- 6.4.10 Elbit Systems Ltd.

- 6.4.11 Israel Aerospace Industries Ltd.

- 6.4.12 Airbus SE

- 6.4.13 HENSOLDT AG

- 6.4.14 The Boeing Company

- 6.4.15 CACI International Inc.

- 6.4.16 Maxar Technologies Holdings Inc.

- 6.4.17 Kratos Defense & Security Solutions, Inc.

- 6.4.18 Defense Research and Development Organisation (DRDO)

- 6.4.19 Hanwha Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment