PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066523

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066523

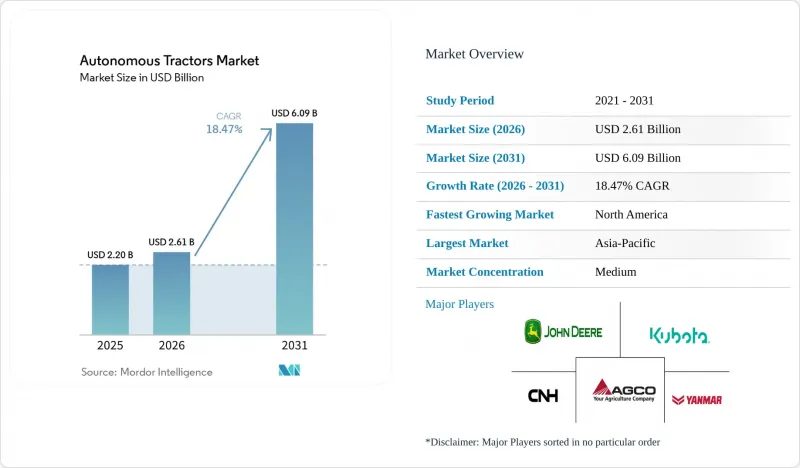

Autonomous Tractors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the autonomous tractor market size is projected to grow from USD 2.20 billion in 2025 to USD 2.61 billion in 2026 and is forecast to reach USD 6.09 billion by 2031 at 18.47% CAGR over 2026-2031.

This report is Segmented by Horsepower (Up To 30 HP, and More), by Automation Level (Fully Automated and Semi-Automated), by Drive Type (Diesel, and More), by Application (Tillage, and More), by Component (GPS/GNSS, and More), by Farm Size (Small, Medium, and Large) and by Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Autonomous Tractors Market Trends and Insights

Farm labor shortages and operator scarcity

The farm labor deficit remains the most durable demand driver for the autonomous tractor market. In fiscal year 2025, the United States Department of Labor certified more than 317,000 H-2A temporary agricultural positions in the first 3 quarters alone, which showed that the domestic labor supply still fell short of seasonal farm demand. The workforce pipeline is also narrowing as the average age of foreign-born farmworkers has continued to rise, weakening long-term labor availability. That makes adoption in the autonomous tractor market less about optional efficiency and more about maintaining field operations when operators are hard to secure. This setting favors farms that already run guidance-enabled fleets, because upgrades from supervised functions to higher autonomy can happen faster than full fleet replacement. It also supports the autonomous tractor market in regions where seasonal labor dependence has become a recurring operating risk.

Precision agriculture and connected guidance stack adoption

Precision agriculture has become the operating base on which the autonomous tractor market now builds higher-value automation. AGCO Corporation introduced the PTx FarmENGAGE platform in August 2025 to connect guidance, field data, and autonomy management across mixed-brand fleets, which showed that software integration is becoming as important as tractor hardware. Farms that already use automated steering, digital boundaries, and field records are better positioned to adopt autonomous workflows with less disruption. That lowers switching friction and strengthens the value of connected ecosystems over standalone machines. It also means the autonomous tractor market is moving toward platform competition, where data continuity and fleet compatibility matter as much as mechanical performance. As a result, manufacturers with broad digital tools can extend customer retention well beyond the initial tractor sale.

High upfront cost and uncertain return on investment for smaller farms

High initial cost remains one of the clearest limits on the autonomous tractor market, especially for farms below commercial scale. A full autonomous package usually includes the tractor, perception hardware, software, and ongoing platform costs, which stretches payback periods beyond what many smaller operations can accept. This keeps early adoption concentrated among larger grain farms and well-capitalized specialty operators that can spread fixed costs across more acres and more machine hours. The pressure becomes stronger when crop prices are volatile and cash flow visibility weakens. Subscription models and retrofit options are starting to reduce the entry burden, but broad mid-market penetration still depends on cheaper hardware and more standardized financing. Until then, cost will continue to slow the autonomous tractor market in regions dominated by smaller holdings.

Other drivers and restraints analyzed in the detailed report include:

- Government support for smart and low-emission farm equipment

- Productivity gains from 24-hour field operations and multi-machine supervision

- Safety, liability, and regulatory ambiguity for unattended field operations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 31 to 100 HP segment held 38.9% market share in 2025, and its share of the autonomous tractor market reflected the broad installed base of mid-range row-crop tractors already used across large field crops. This band remains the largest because many farms in North America and Europe already operate guidance-ready models in this range, making retrofit upgrades more practical than a complete fleet replacement. These tractors are well-suited for common sowing, spraying, and light tillage tasks that are repetitive and easier to automate under commercial conditions. That keeps demand steady even as higher-power platforms gain attention. The autonomous tractor industry still depends heavily on this range because it forms the bridge between assisted steering adoption and broader autonomy.

Above 100 HP is the fastest-growing horsepower segment and is projected to expand at 23.4% CAGR from 2026 to 2031 as very large farms shift more tillage and grain-cart operations toward driverless workflows. AGCO Corporation launched the Fendt 1000 Vario Gen4 series in late 2025 with factory-integrated OutRun autonomy, and commercial deliveries began in 2026 for models spanning 400 to 520 horsepower. Deere and Company also expanded compatibility for autonomous tillage on 8R, 8RX, 9R, and 9RX tractors, which supports higher-power field work on large commercial farms.

Semi-autonomous systems are projected to account for 67.6% of the market share in 2025. This dominance in the autonomous tractor market is attributed to the continued reliance on operators in supervisory roles for most commercial deployments. This segment includes automated steering, headland turning, and section control that dealers can install and support using familiar tools and established interfaces. Farmers also view these systems as lower-risk because responsibility remains closer to the machine operator. That makes the segment the largest commercial pathway in the autonomous tractor market today. It also fits better with current insurance and regulatory conditions in most countries.

Fully Autonomous systems are the fastest-growing segment and are forecast to rise at 22.5% CAGR from 2026 to 2031 as software, perception, and fleet management tools improve. AGCO Corporation has stated a goal of enabling a full-cycle autonomous crop production system by 2030, extending autonomy beyond tillage into seeding, spraying, and harvest coordination. The adoption path is gradual because many farms first build field boundaries, digital records, and trust through semi-autonomous use. That means the current installed base of supervised systems also serves as the feeder pipeline for later driverless upgrades. In the autonomous tractor market, this structural transition matters more than a simple comparison between current share and future growth.

Geography Analysis

Asia-Pacific held 45.8% of the autonomous tractor market share in 2025, which made it the largest region by value. Japan supports this position through advanced farm robotics development and a policy environment that has steadily moved toward the use of autonomous machinery. China benefits from broad mechanization priorities, while India adds scale through its large annual tractor sales base, even though smallholding patterns and uneven infrastructure slow the pursuit of full autonomy. YANMAR HOLDINGS CO., LTD. has continued to develop agricultural work-support technologies using artificial intelligence and edge computing, reflecting the region's push toward practical remote and autonomous farm operations. South Korea and Australia also remain important because aging farm populations and large operational footprints support adoption in different ways.

North America is the fastest-growing regional segment in the autonomous tractor market, projected to expand at a 22.6% CAGR from 2026 to 2031. The region benefits from large field sizes, high labor costs, and farm structures that can justify autonomous tillage, spraying, and grain-cart workflows. Deere & Company is scaling its autonomous tillage offering through 2026, which will support the first meaningful commercial installed base in large-scale agriculture. Canada is also supporting cleaner and more automated farm technology through public funding for the Canadian Agri-Food Automation and Intelligence Network. Mexico remains earlier in adoption because smaller farm structures reduce the immediate economics of full autonomy.

Europe remains an important part of the autonomous tractor market because it combines strong precision agriculture maturity with strict safety and regulatory oversight expectations. The European Union's climate and machinery policy is supporting investment in low-emission, digitally managed farm equipment, even though unattended use cases still face tighter compliance requirements than in some other regions. Germany, France, and the United Kingdom lead regional demand, while the Middle East and Africa remain earlier-stage markets centered on pilot activity and commercial estate farming. South America has strong long-run potential in Brazil and Argentina, but import costs, connectivity gaps, and correction reliability issues still restrain faster rollout.

- Deere & Company

- AGCO Corporation

- CNH Industrial N.V.

- Kubota Corporation

- Mahindra & Mahindra

- Monarch Tractor

- AutoNext Automation

- YANMAR HOLDINGS CO., LTD.

- CLAAS KGaA mbH

- TYM Corporation

- SDF Group

- ZETOR TRACTORS a.s. (HTC Corporation)

- Sonalika

- Kioti (daedong)

- ISEKI & Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Farm labor shortages and operator scarcity

- 4.2.2 Precision agriculture and connected guidance stack adoption

- 4.2.3 Government support for smart and low-emission farm equipment

- 4.2.4 Productivity gains from 24-hour field operations and multi-machine supervision

- 4.2.5 Retrofit autonomy kits and autonomy-ready tractor platforms

- 4.2.6 Specialty-crop mechanization in orchards and vineyards

- 4.3 Market Restraints

- 4.3.1 High upfront cost and uncertain return on investment for smaller farms

- 4.3.2 Safety, liability, and regulatory ambiguity for unattended field operations

- 4.3.3 GNSS reliability, connectivity gaps, and cyber risk in connected fleets

- 4.3.4 Implement interoperability and dealer-service readiness bottlenecks

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Horsepower

- 5.1.1 Up to 30 HP

- 5.1.2 31 - 100 HP

- 5.1.3 Above 100 HP

- 5.2 By Automation Level

- 5.2.1 Semi-Autonomous

- 5.2.2 Fully Autonomous

- 5.3 By Drive Type

- 5.3.1 Diesel

- 5.3.2 Hybrid

- 5.3.3 Battery-Electric

- 5.4 By Application

- 5.4.1 Tillage

- 5.4.2 Sowing

- 5.4.3 Harvesting

- 5.4.4 Orchard and Vineyard Operations

- 5.5 By Component

- 5.5.1 GPS/GNSS

- 5.5.2 Sensors and Vision Systems

- 5.5.3 LiDAR and Radar Modules

- 5.5.4 Control and Navigation Software

- 5.6 By Farm Size

- 5.6.1 Small ( Less than 100 ha)

- 5.6.2 Medium (100-500 ha)

- 5.6.3 Large ( More than 500 ha)

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.1.4 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Spain

- 5.7.3.5 Russia

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 Australia

- 5.7.4.5 South Korea

- 5.7.4.6 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 UAE

- 5.7.5.3 Turkey

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Rest of Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 AGCO Corporation

- 6.4.3 CNH Industrial N.V.

- 6.4.4 Kubota Corporation

- 6.4.5 Mahindra & Mahindra

- 6.4.6 Monarch Tractor

- 6.4.7 AutoNext Automation

- 6.4.8 YANMAR HOLDINGS CO., LTD.

- 6.4.9 CLAAS KGaA mbH

- 6.4.10 TYM Corporation

- 6.4.11 SDF Group

- 6.4.12 ZETOR TRACTORS a.s. (HTC Corporation)

- 6.4.13 Sonalika

- 6.4.14 Kioti (daedong)

- 6.4.15 ISEKI & Co., Ltd

7 Market Opportunities and Future Outlook