PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066530

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066530

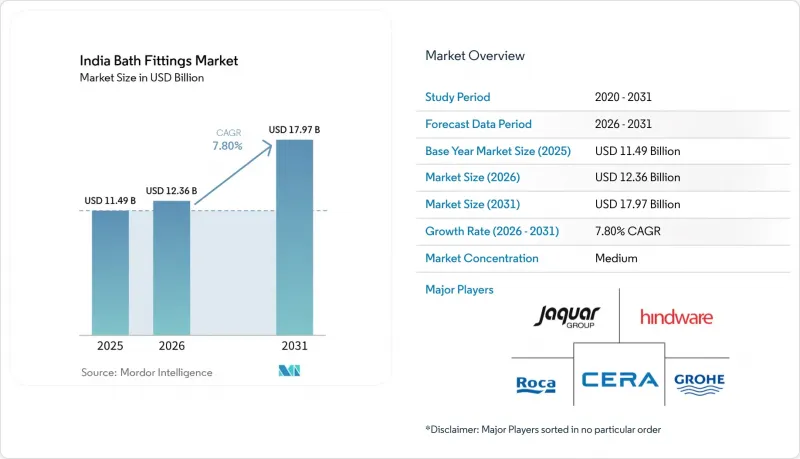

India Bath Fittings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india bath fittings market size is expected to increase from USD 11.49 billion in 2025 to USD 12.36 billion in 2026 and reach USD 17.97 billion by 2031, growing at a CAGR of 7.8% over 2026-2031.

This report is Segmented by Product Type (Faucets, Showerheads & Systems, Bathtubs, Other Bath Accessories and Fittings), Market Type (Organized, Unorganized), Price Range (Economy, Mid-Range, Premium), End User (Residential, Commercial), Distribution Channel (B2C and B2B), and Geography (North India, South India, West India, East & Northeast India). Market Forecasts are Provided in Terms of Value (USD).

India Bath Fittings Market Trends and Insights

PMAY-Led Urban Housing Completions Sustain Fixture Demand

PMAY Urban crossed 96.65 lakh completed homes by February 2026, which set a structural floor for fixture demand as each eligible unit requires basic tap and sanitation infrastructure. The next leg of demand will track beneficiary occupancy and handover timelines, since final utility connections and essential services determine when installation orders convert at scale in individual projects. Andhra Pradesh has been among the highest delivery states, which supports sustained volumes of faucets, showers, cisterns, and accessories in local procurement pipelines across 2026. PMAY U 2.0 targets an additional one crore homes by 2029, with new sanctions already underway as of mid 2025, which extends visibility for the Indian bath fittings market into the late 2020s. The PMAY framework links closely with sanitation and water conservation reforms under AMRUT 2.0 and Bharat Tap, which together are nudging municipal procurements toward certified water-efficient fixtures over the medium term. As these programs scale, the Indian bath fittings market benefits from long cycle replacement demand due to maintenance intervals and upgrades in high-use public and affordable housing assets.

Premiumization and Aesthetic Upgrades in Bathrooms

Premium features are moving beyond metros as developers and homeowners in tier-2 cities adopt spa-style showers, concealed diverters, and coordinated finish suites that elevate perceived value in new projects and renovations across the Indian bath fittings market. Lixil's plan to expand from 350 to 500 stores highlights how funnel depth is growing outside top metros, and large B2B orders often span thousands of bathrooms per high-rise development, which keeps premium lines visible and available in local markets. Hindware's focus on premiumization through Experience Centers and a three-tier brand architecture keeps price ladders clear for consumers and architects who want sensor taps, rain showers, and smart controls in curated combinations. Premium growth also reflects higher awareness of water-efficient and sustainable products as IGBC credits and BIS star ratings become part of design briefs in urban projects. As portfolios skew to touchless and low-flow products, users report better hygiene and lower water bills, which reinforces premium uptake through word of mouth and developer specifications in 2026. These dynamics continue to separate India's path from commodity-led cycles as premiumized SKUs sustain value creation for the India bath fittings market through 2031.

Compliance Costs for Chrome and Nickel Plating, ETP, and Permits

Compliance costs are rising for electroplating, including requirements for effluent treatment plants and adherence to discharge norms for chromium and nickel, which raises fixed and recurring costs for small and mid-scale units that lack integration. Environmental compliance places pressure on units that previously competed on price alone, which narrows the cost gap with organized players that amortize these systems across larger volumes. The effect is more acute for value-tier SKUs where price ceilings are strict, which reduces flexibility to pass through higher treatment and monitoring costs to channel partners. As state pollution control boards and urban local bodies step up oversight in 2026, frequent audits and documentation add administrative load to production schedules and delivery commitments. These requirements dampen the speed at which sub-scale manufacturers can respond to tender-led demand that prefers companies with proven compliance records.

Other drivers and restraints analyzed in the detailed report include:

- Hospitality and Healthcare Project Pipeline

- Green Building Codes (IGBC/GRIHA/NBC) Specifying Low-Flow Fixtures

- Input Cost Volatility, Brass and Plating Chemicals, and Energy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Faucets accounted for 36.45% of the Indian bath fittings market size in 2025, and the product mix shows wellness-driven momentum as bathtubs and spa fittings are projected to grow at a 7.34% CAGR through 2031. Faucets remain volume anchors across new builds and renovations, and adoption rises when brands add touchless activation and durable finishes that align with both hygiene and aesthetic preferences in urban households. Shower systems are bifurcating between rain-shower formats in premium projects and efficient handheld units in mid-tier and public buildings that prioritize three-star performance under BIS standards. Low-flow compliance at 6.8 liters per minute for three-star shower heads and optimized aerators for basin taps are influencing the specification sheets on Grade-A offices and hotels, which then filter into residential preferences over time. Bathtubs and spa fittings, while having a smaller base, benefit from developers positioning master bathrooms as wellness spaces in premium apartments and luxury hotels, which pulls coordinated accessory sales along with core fixtures in the Indian bath fittings market.

Developers show homes and hospitality brand standards are normalizing premium shower columns, thermostatic mixers, and concealed diverters, which elevate buyer expectations during home selection and upgrade cycles. Efficient dual-flush cisterns and coordinated accessories are becoming baseline in green-focused projects, as IGBC and GRIHA credits translate into practical checklists for contractors and MEP consultants. Branded accessory sets bundled with faucets and showers are increasing average ticket sizes as homeowners prefer matched finishes, which reduces piecemeal purchases that often lead to fit and finish issues. The Indian bath fittings market is also seeing a steady shift to products tested for pressure and flow stability, which support reliable performance across variable municipal water conditions in 2026. Together, these forces keep product innovation tied to both wellness and compliance outcomes, which strengthens category resilience through the forecast period.

The organized segment held 58% share in 2025 and is projected to grow at an 8.58% CAGR through 2031, which outpaces the unorganized segment and reflects consistent gains in brand-led distribution and project credentials. Exclusive stores now act as specification hubs for architects and developers, where brands demonstrate synchronized suites of faucets, showers, and accessories with documented flow and efficiency metrics under BIS and IGBC norms. Multiyear project frameworks for offices, hotels, and institutional buildings reinforce organized suppliers' advantages in service, spare parts availability, and installation support across multiple cities. New brand entries confirm the market's capacity to absorb premium tiers, as seen with Moen's partnership-led entry and Experience Center in New Delhi that targets discerning buyers and project specifiers.

Production investments underline confidence in the India bath fittings industry's demand runway, including Roca India's INR 400 crore (USD 48.2 million) program in Tamil Nadu to enhance process automation and expand fittings capacity, and Hansgrohe's plan to expand assembly capacity with a 2030 horizon for scale. As water-efficiency codes deepen, organized brands that maintain broad certification coverage and strong post-installation support are likely to attract more project-based orders than unorganized competitors that face rising compliance and documentation hurdles. These advantages compound in 2026 as public and private tenders incorporate star ratings and installation assurance requirements, which keep the organized trajectory ahead of the broader Indian bath fittings market.

List of Companies Covered in this Report:

- Jaquar Group

- Hindware

- CERA Sanitaryware

- Roca Parryware

- Kohler

- Grohe

- American Standard

- TOTO

- Delta Faucet

- Hansgrohe

- Duravit

- Somany Bathware

- Astral Bathware

- Hafele

- Johnson Bathrooms

- Prayag

- JAL (Jupiter Aqua Lines)

- Carysil

- Moen Incorporated

- RAK Ceramics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 PMAY-led urban housing completions sustain fixture demand

- 4.2.2 Premiumization and aesthetic upgrades in bathrooms

- 4.2.3 Hospitality and healthcare project pipeline

- 4.2.4 Green building codes (IGBC/GRIHA/NBC) specifying low-flow fixtures

- 4.2.5 BIS star-rating (IS 17650) nudges low-flow faucets & showers

- 4.2.6 Shift to organised players in Tier 2/3 cities

- 4.3 Market Restraints

- 4.3.1 Compliance costs for chrome/nickel plating (ETP, permits)

- 4.3.2 Input cost volatility (brass, plating chemicals, energy)

- 4.3.3 Grey/unorganised price competition in value tiers

- 4.3.4 Emerging water-efficiency codes raising spec thresholds

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Faucets

- 5.1.2 Showerheads & Systems

- 5.1.3 Bathtubs

- 5.1.4 Other Bath Accessories and Fittings

- 5.2 By Market Type

- 5.2.1 Organized

- 5.2.2 Unorganized

- 5.3 By Price Range

- 5.3.1 Economy

- 5.3.2 Mid-Range

- 5.3.3 Premium

- 5.4 By End User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Distribution Channel

- 5.5.1 B2C

- 5.5.1.1 Multibrand Stores

- 5.5.1.2 Exclusive Stores

- 5.5.1.3 Online

- 5.5.1.4 Other Distribution Channels

- 5.5.2 B2B (Direct & Project Sales)

- 5.5.1 B2C

- 5.6 By Region (India)

- 5.6.1 North India

- 5.6.2 South India

- 5.6.3 West India

- 5.6.4 East & Northeast India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Jaquar Group

- 6.4.2 Hindware

- 6.4.3 CERA Sanitaryware

- 6.4.4 Roca Parryware

- 6.4.5 Kohler

- 6.4.6 Grohe

- 6.4.7 American Standard

- 6.4.8 TOTO

- 6.4.9 Delta Faucet

- 6.4.10 Hansgrohe

- 6.4.11 Duravit

- 6.4.12 Somany Bathware

- 6.4.13 Astral Bathware

- 6.4.14 Hafele

- 6.4.15 Johnson Bathrooms

- 6.4.16 Prayag

- 6.4.17 JAL (Jupiter Aqua Lines)

- 6.4.18 Carysil

- 6.4.19 Moen Incorporated

- 6.4.20 RAK Ceramics

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

- 7.2 Targeted retrofit programs for BIS IS 17650 star-rated faucets/showers in government and Grade-A commercial assets

- 7.3 Tier-2/3 hospitality pipeline bundling (showers, mixers, water-saving kits) for multi-year project sales