PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066584

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066584

GCC Home Textile - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

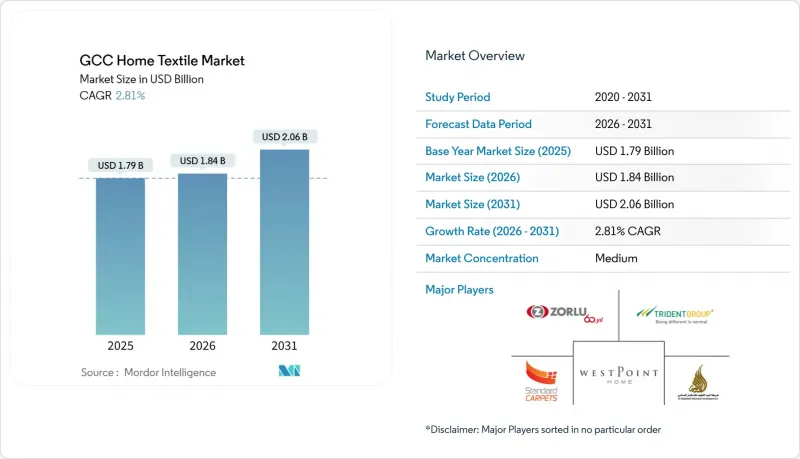

According to Mordor Intelligence, the gCC home textile market size is expected to increase from USD 1.79 billion in 2025 to USD 1.84 billion in 2026 and reach USD 2.06 billion by 2031, growing at a CAGR of 2.81% over 2026-2031.

This report is Segmented by Application(Bed Linen, Bath Linen, Kitchen Linen, Upholstery, and More), Material (Cotton, Linen, Synthetic Fibers, and More), End-User (Residential, Commercial), Distribution Channel (Offline and Online), and Geography (Saudi Arabia, UAE, Qatar, Kuwait, Oman, Bahrain). Market Forecasts are Provided in Terms of Value (USD Million).

GCC Home Textile Market Trends and Insights

Hotel Room Pipeline in KSA and UAE Lifts B2B Linen Demand

Commercial procurement remains the center of gravity for the GCC home textile market, led by hotel openings and expansions that translate into large, repeat orders for sheets, duvet covers, and towels. Chain-led signing momentum in 2025 carried into 2026, with Marriott highlighting Saudi Arabia and the UAE among its highest growth Middle East markets and reporting more than 230 organic signings across EMEA in 2025, which supports multi-year linen frameworks for new and converted properties. Procurement teams specify par stocks that typically range to six full sets per key for high-occupancy hotels, which multiplies base room counts into sizeable textile tenders that renew on 18 to 24 month cycles in premium segments. Branded residences and mixed-use luxury developments also add institutional volume, as villa and apartment operators standardize bedroom, bath, and window treatments at handover to protect brand standards. Large owners and operators favor suppliers that can demonstrate end-to-end traceability and consistent testing documentation, which further consolidates spend among vertically integrated firms that can service multi-country pipelines. As operators scale, purchase orders often pool across clusters to capture volume discounts, which strengthens demand visibility for certified suppliers in the GCC home textile market.

Housing Programs and Rising Homeownership in Saudi Arabia Boost Residential Textile Purchases.

Saudi Arabia's housing initiative and mortgage programs have lifted the owner-occupier share, which in turn stimulated initial household purchases of complete textile sets after unit handover. The Housing Program's 2024 report confirmed progress on delivery of more than 122,000 housing solutions for Saudi families, reinforcing a steady pipeline of new households entering the market for bedding, toweling, kitchen textiles, and curtains. First-time buyers typically make consolidated purchases within weeks of key collection, which compresses demand into the same quarter and benefits distributors able to maintain inventory breadth closest to new communities. As more master-planned neighborhoods go live across major cities, developers and retailers coordinate curated packages that simplify selection and standardize quality, which supports higher attach rates for mid-tier and premium lines. The procurement model for these neighborhoods often embeds a short-list of approved vendors, which channels volume to suppliers with reliable documentation and post-sale support. These housing dynamics anchor a broad base of residential demand that complements institutional cycles in the GCC home textile market.

Volatile Cotton and Freight Costs Pressure Pricing and Margins

Input and transport cost swings remain a key headwind for the GCC home textile market, since mills and distributors must manage quarterly variability in raw cotton and global shipping. Industry association updates for early 2026 point to choppy cotton pricing conditions around contract rollovers, which complicates fixed-price commitments with institutional clients that resist mid-cycle surcharges. Shipping costs stabilized from prior peaks but remain elevated compared with pre-pandemic baselines, while route disruptions across key lanes have lifted insurance and added days-in-transit on certain corridors, which challenge JIT replenishment for time-sensitive orders. Exporters documented the impact of rerouting and higher logistics expenses in 2024, with one leading South Asian mill reporting significant increases in selling costs tied to shipping detours and related premiums, which compressed margins at the supplier level. GCC importers often absorb part of these surges to preserve shelf prices for cost-sensitive residential shoppers, which reduces unit economics in promotional periods. Institutional buyers also negotiate volume flexibility into contracts, which can magnify the effect of adverse cost movements on supplier EBITDA. The combination of cotton volatility and freight variability forces more cautious buying and shorter tender tenures in the GCC home textile market.

Other drivers and restraints analyzed in the detailed report include:

- Government Economic Diversification Initiatives

- Premiumization in Luxury Hospitality, Including FR and Antimicrobial Specifications

- Fragmented Retail Landscape and Private Labels Intensify Price Competition.

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bed linen held 33% of revenue in 2025, reflecting its significant role in both residential and institutional procurement, while carpets and rugs are projected to lead product growth at a 3.72% CAGR through 2031 within the GCC home textile market size. The profile of bed linen purchases in hospitality is stabilizing at higher specifications, including T-300 percale and antimicrobial finishes for hygiene-focused environments, which lifts unit values even as replacement cycles extend in premium tiers. Hotels and serviced apartments also continue to anchor large tender volumes, where six-set par stock norms per room translate into bulk orders that repeat on 18 to 24 month cycles, supporting steady baseline demand in the GCC home textile market. Residential bed linen shoppers add seasonality around Eid and year-end periods, which benefits retailers and marketplaces that synchronize assortments and promotions with local holidays. Bath linen remains a durable mid-tier category in institutional settings, where frequent laundering and durability expectations guide specifications like GSM and pile structure, which helps suppliers segment the offer by price and performance. In the value segment, private-label bath and kitchen textiles sourced from large South Asian mills reinforce price leadership, while premium assortments play in higher thread counts, long-staple cottons, and design-led weaves.

Carpets and rugs benefit from interior fit-out cycles in villas and apartments as handovers surge, as well as periodic refreshes in hospitality lobbies and corridors aligned with renovation schedules in the GCC home textile market. Residential buyers often allocate a defined budget to area rugs when furnishing new-build properties, which supports steady unit movement even in soft retail months. Hospitality properties seek stain resistance and color fastness validated by lab reports, which advantages mills with in-house testing and reliable batch consistency. Kitchen linen and upholstery textiles are niche subcategories where house labels win share based on unit price and basic quality controls, while specialty stores differentiate with tactile experience and customization. Suppliers that sustain end-to-end traceability and maintain compliance-ready documentation meet the rising bar for institutional bids that now embed ESG and safety screens. Across product categories, certified inputs and reliable finishes have become table stakes for winning the most valuable business in the GCC home textile market.

Cotton retained a 68.42% share in 2025, supported by long-standing supply chains and material familiarity, yet alternative fibers are set to grow faster at a 5.64% CAGR (2026-2031), reflecting premiumization and eco-led choices within the GCC home textile market size. Sustainable sourcing and traceability are increasingly non-negotiable, with leading manufacturers reporting high shares of sustainably sourced cotton and building toward full targets by 2030, supported by blockchain-enabled fiber-to-shelf tracking. Linen blends attract luxury residential buyers seeking breathability in air-conditioned climates, while wool and silk remain limited to decorative uses and luxury suites where tactile feel and visual finish command premiums. Bamboo and other cellulosic fibers appeal to eco-conscious consumers willing to pay for certified towels and sheets, which gives retailers a storytelling angle and a margin buffer in curated ranges. In utility bedding, synthetic fills dominate pillows and quilts due to hypoallergenic properties and cost-of-care advantages, which align with large bed-in-a-bag programs run by global brands expanding their capacity through acquisitions in adjacent categories. Regulatory and testing initiatives, including increased focus on microplastic shedding standards aligned with ISO frameworks, are pushing suppliers to segregate material streams and maintain stronger labeling controls for GCC-bound shipments.

Cotton price volatility and freight variability continue to shape material choices and product structure for the GCC home textile market. Buyers hedge risk by maintaining mixed portfolios that include organic cotton, recycled polyester, and bamboo in select lines, which allows a quick response to input cost shifts without disrupting brand standards. Institutional buyers emphasize durability and wash performance over composition per se, which sustains demand for blended fabrics that survive high-temperature cycles while retaining feel. Retailers use material stories to differentiate tiered ranges, pairing certifications with visual merchandising to move consumers up the price ladder. Suppliers that can guarantee both compliance and consistent fabric hand in cotton-rich lines defend core volume while testing eco-forward options in new collections. This balance enables the GCC home textile industry to adapt to both price swings and rising sustainability expectations.

List of Companies Covered in this Report:

- Al Abdullatif Industrial Investment Co.

- Al Sorayai / Naseej International Trading

- Omar Kassem Alesayi Group

- Satex

- Standard Carpets Ind. LLC

- Abu Dhabi National Carpet Factory - ADNC

- WestPoint Home

- Oriental Weavers Group

- Welspun Living Ltd

- Trident Limited

- Indo Count Industries Ltd

- D'Decor Home Fabrics

- Zorlu Tekstil

- Menderes Tekstil

- Merinos HalI

- Nishat Mills Ltd

- Gul Ahmed Textile Mills Ltd

- Sunvim Group

- Luolai Lifestyle Technology

- Beaulieu International Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hotel room pipeline in KSA and UAE lifts B2B linen demand

- 4.2.2 Housing programs and rising homeownership in Saudi boost residential textile purchases

- 4.2.3 Government economic diversification initiatives

- 4.2.4 Premiumization in luxury hospitality (thread count, FR, antimicrobial specs)

- 4.2.5 SASO/GSO textile compliance tightening raises certified sourcing

- 4.2.6 UAE re-export hubs (JAFZA/Bharat Mart) compress lead times for assortments

- 4.3 Market Restraints

- 4.3.1 Volatile cotton and freight costs pressure pricing and margins

- 4.3.2 Fragmented retail landscape and private labels intensify price competition

- 4.3.3 Water scarcity limits local dyeing/finishing scalability

- 4.3.4 Giga-project execution risks can delay hospitality-driven orders

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Bed Linen

- 5.1.2 Bath Linen

- 5.1.3 Kitchen Linen

- 5.1.4 Upholstery

- 5.1.5 Others (Carpets & Area Rugs)

- 5.2 By Material

- 5.2.1 Cotton

- 5.2.2 Linen

- 5.2.3 Synthetic Fibres

- 5.2.4 Other Materials (Wool, Hemp, Silk, Jute, Bamboo)

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.4 By Distribution Channel

- 5.4.1 Offline

- 5.4.2 Mass Merchandisers (Hypermarkets/Supermarkets)

- 5.4.3 Home Centers

- 5.4.4 Specialty Stores

- 5.4.5 Other Offline Channels

- 5.4.6 Online

- 5.5 By Region

- 5.5.1 Saudi Arabia

- 5.5.2 UAE

- 5.5.3 Qatar

- 5.5.4 Kuwait

- 5.5.5 Oman

- 5.5.6 Bahrain

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Al Abdullatif Industrial Investment Co.

- 6.4.2 Al Sorayai / Naseej International Trading

- 6.4.3 Omar Kassem Alesayi Group

- 6.4.4 Satex

- 6.4.5 Standard Carpets Ind. LLC

- 6.4.6 Abu Dhabi National Carpet Factory - ADNC

- 6.4.7 WestPoint Home

- 6.4.8 Oriental Weavers Group

- 6.4.9 Welspun Living Ltd

- 6.4.10 Trident Limited

- 6.4.11 Indo Count Industries Ltd

- 6.4.12 D'Decor Home Fabrics

- 6.4.13 Zorlu Tekstil

- 6.4.14 Menderes Tekstil

- 6.4.15 Merinos HalI

- 6.4.16 Nishat Mills Ltd

- 6.4.17 Gul Ahmed Textile Mills Ltd

- 6.4.18 Sunvim Group

- 6.4.19 Luolai Lifestyle Technology

- 6.4.20 Beaulieu International Group

7 Market Opportunities & Future Outlook

- 7.1 SASO/GSO-compliant, low-water, quick-dry institutional linens for GCC laundries

- 7.2 Omnichannel private-label programs for Home Centers and hypermarkets with near-shore sourcing