PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066599

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066599

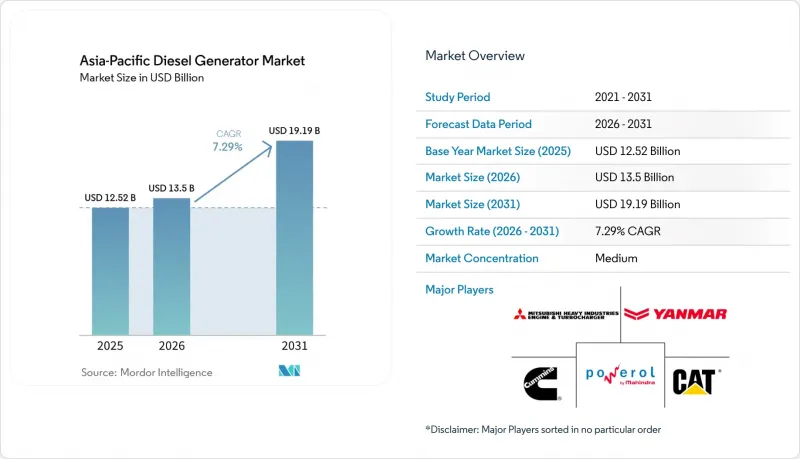

Asia-Pacific Diesel Generator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific diesel generator market size is projected to expand from USD 12.52 billion in 2025 and USD 13.5 billion in 2026 to USD 19.19 billion by 2031, registering a CAGR of 7.29% between 2026 to 2031.

This report is Segmented by Capacity (Below 75 KVA, 75 To 350 KVA, 375 To 750 KVA, 750 To 2, 000 KVA, and Above 2, 000 KVA), Application (Stand-by/Backup Power, Prime/Continuous Power, and Peak-shaving/Load Management), End-User (Residential, Commercial, and Industrial), and Geography (China, India, Japan, South Korea, ASEAN Countries, Australia and New Zealand, and Rest of Asia-Pacific).

Asia-Pacific Diesel Generator Market Trends and Insights

Rapid Industrialization & Urbanization

India's Production-Linked Incentive outlays of USD 30 billion across 14 sectors by 2025 deepened power-demand spikes in Tamil Nadu and Uttar Pradesh, where summer deficits touched 15%. Similar strains emerged in Vietnam's Bac Ninh and Hai Phong electronics belts after USD 20 billion of FDI arrived in 2024, yet transmission upgrades trail demand by up to three years. Buyers, therefore, budget for 750-2,000 kVA prime-rated sets, moving gensets from facilities overhead to core capex and extending replacement cycles to ten years. Fuel efficiency and Stage IV compliance have become board-level KPIs because continuous duty now dominates procurement briefs.

Data-Center Build-Out Boom

A 19,371 MW IT-load pipeline across Asia-Pacific in 2025 requires 1.2-1.5X redundancies, translating into 23,000-29,000 MW of diesel backup demand if all projects proceed. Adani's pledged 5 GW AI campus in India alone implies 7,500 MW in gensets by 2035. Data-sovereignty statutes, such as Indonesia's in-country hosting rule, accelerate localized build-outs in weak-grid markets, ensuring multi-megawatt gensets stay relevant even as renewable penetration rises.

Stricter Emission Regulations Favoring Gas & Renewables

China's National VI and India's CPCB Stage IV add 15-20% to diesel genset capex, eroding the cost gap versus gas turbines and solar-plus-storage hybrids. Singapore's carbon tax of SGD 25 per ton in 2024 rises to as high as SGD 80 by 2030, accelerating shifts to low-carbon backup.

Other drivers and restraints analyzed in the detailed report include:

- Grid-Reliability Gaps & Outage Frequency

- Hybrid Micro-Grids on Island Tourism Hubs

- Volatile Diesel Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 375-750 kVA class captured 45.1% of the Asia-Pacific diesel generator market share in 2025. Telecom towers, mid-rise offices, and light factories prize its footprint and price. However, above-2,000 kVA units are forecast to post an 8.7% CAGR, making them the fastest contributor to the Asia-Pacific diesel generator market size growth. Hyperscalers parallel 2-3 MW blocks to reach 20 MW arrays, while Indonesian and Australian mines deploy multi-MW islands for off-grid hauling operations.

Below-75 kVA sets face solar-plus-battery substitution in urban homes, yet remain essential in remote clinics. The 75-375 kVA band benefits from India's 5G rollout; 200,000 new macro towers in 2024-2025, each specified 30-50 kVA backup. ISO 8528 certification is now non-negotiable above 500 kVA as buyers demand transient load handling and harmonic control.

List of Companies Covered in this Report:

- Caterpillar Inc.

- Cummins Inc.

- Mitsubishi Heavy Industries Engine & Turbocharger Ltd.

- Yanmar Holdings Co. Ltd.

- Mahindra Powerol Ltd.

- Generac Power Systems

- Doosan Corporation

- Kohler Co.

- Kirloskar Oil Engines Ltd.

- Perkins Engines Company Ltd.

- Atlas Copco AB

- Himoinsa (SA de CV)

- Rolls-Royce Power Systems (MTU)

- Honda Motor Co. Ltd.

- Aksa Power Generation

- Weichai Power Co. Ltd.

- Aggreko plc

- Briggs & Stratton LLC

- Wartsila Corporation

- SG Generator Pvt Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid industrialisation & urbanisation

- 4.2.2 Data-centre build-out boom

- 4.2.3 Grid-reliability gaps & outage frequency

- 4.2.4 Hybrid micro-grids on island tourism hubs

- 4.2.5 Emission-norm driven replacement cycle (CPCB IV+)

- 4.2.6 Predictive-maintenance digital twins lowering TCO

- 4.3 Market Restraints

- 4.3.1 Stricter emission regulations favouring gas & RE

- 4.3.2 Volatile diesel prices

- 4.3.3 Corporate renewable PPAs cutting genset run-time

- 4.3.4 Shortage of Tier-4 skilled technicians

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Capacity (kVA)

- 5.1.1 Below 75 kVA

- 5.1.2 75 to 375 kVA

- 5.1.3 375 to 750 kVA

- 5.1.4 750 to 2,000 kVA

- 5.1.5 Above 2,000 kVA

- 5.2 By Application

- 5.2.1 Stand-by/Backup Power

- 5.2.2 Prime/Continuous Power

- 5.2.3 Peak-shaving/Load Management

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 ASEAN Countries

- 5.4.6 Australia and New Zealand

- 5.4.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Caterpillar Inc.

- 6.4.2 Cummins Inc.

- 6.4.3 Mitsubishi Heavy Industries Engine & Turbocharger Ltd.

- 6.4.4 Yanmar Holdings Co. Ltd.

- 6.4.5 Mahindra Powerol Ltd.

- 6.4.6 Generac Power Systems

- 6.4.7 Doosan Corporation

- 6.4.8 Kohler Co.

- 6.4.9 Kirloskar Oil Engines Ltd.

- 6.4.10 Perkins Engines Company Ltd.

- 6.4.11 Atlas Copco AB

- 6.4.12 Himoinsa (SA de CV)

- 6.4.13 Rolls-Royce Power Systems (MTU)

- 6.4.14 Honda Motor Co. Ltd.

- 6.4.15 Aksa Power Generation

- 6.4.16 Weichai Power Co. Ltd.

- 6.4.17 Aggreko plc

- 6.4.18 Briggs & Stratton LLC

- 6.4.19 Wartsila Corporation

- 6.4.20 SG Generator Pvt Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment