PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066600

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066600

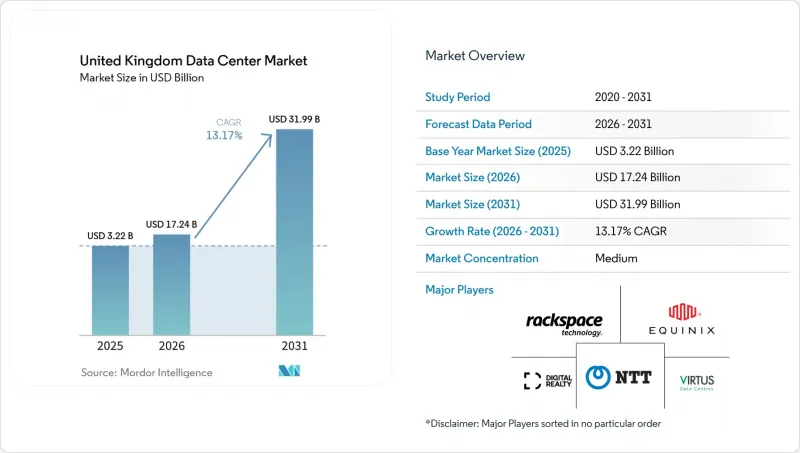

United Kingdom Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united kingdom data center market size was valued at USD 15.23 billion in 2025 and estimated to grow from USD 17.24 billion in 2026 to reach USD 31.99 billion by 2031, at a CAGR of 13.17% during the forecast period (2026-2031).

This report is Segmented by Data Center Size (Small, Medium, Large, Mega, and Massive), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-built, Enterprise/Edge, and Colocation), End User (BFSI, IT and ITES, E-Commerce, Government, Manufacturing, Media and Entertainment, and More), and Hotspot. The Market Forecasts are Provided in Terms of IT Load Capacity (MW).

United Kingdom Data Center Market Trends and Insights

Surge in hyperscale cloud and AI compute demand

Hyperscale operators drive a structural uplift in rack power density as AI training workloads migrate into purpose-built campuses. Amazon's GBP 8 billion (USD 10.73 billion) program through 2028, Microsoft's multi-region estate expansion, and Google's liquid-cooled cluster roll-outs collectively add more than 1 GW of near-term capacity. Facility blueprints now specify 100-150 kW racks, direct-to-chip liquid loops, and on-site gas turbines to bypass multi-year grid queues The United Kingdom data center market therefore absorbs deep-tech capital inflows, job creation, and supply-chain localization across switchgear, chillers, and modular power plants.

Growth of 5G and edge computing across the United Kingdom

Nationwide 5G coverage stimulates distributed processing needs that small and medium edge nodes satisfy within a 10 ms latency envelope. Vodafone's Manchester Edge Lab and BT's Wavelength alliance furnish reference architectures that operators replicate across urban corridors. Enterprises deploying private 5G in logistics and manufacturing now co-locate micro-data rooms inside campuses, spurring a sub-10 MW segment of the United Kingdom data center market serving IoT analytics and AR-enabled maintenance

Power-grid connection delays in London availability zones

National Grid warns that London data center demand could reach 6 GW by 2035, yet capacity expansions lag, adding multi-year delays to already committed builds. Developers therefore weigh behind-the-meter gas turbines and battery energy-storage systems while scoping northern sites with spare transmission headroom

Other drivers and restraints analyzed in the detailed report include:

- Rising adoption of hybrid IT among BFSI and enterprise segments

- Government incentives for digital infrastructure and the National Planning Framework

- Escalating construction and energy costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Massive facilities dominated with 37.05% United Kingdom data center market share in 2025 on the back of multi-tenant colocation halls catering to cloud regions and large enterprises. The segment maintains scale advantages through established fiber routes, mature operations teams, and embedded cross-connect ecosystems. However, mega-campus projects exceeding 250 MW are projected to capture the highest 31.45% CAGR to 2031 as AI workloads necessitate contiguous plots and on-site substations capable of delivering 400 kV feeds. The United Kingdom data center market size for mega campuses is forecast to surpass 6,140 MW by 2031, reflecting strategic pivots by investors seeking long-duration contracts with hyperscale tenants.

Mega-campus design typologies now feature modular power rooms, liquid-cooling manifolds, and roof-mounted dry-coolers that displace water-intensive towers. These projects benefit from economies of scale in equipment procurement and power-purchase agreements, often negotiating 15-year renewable PPAs that stabilize operating costs. In contrast, small and medium data centers align with edge applications and regulatory niches that demand geographic proximity to users, capturing resilient albeit slower-growing demand pockets within the broader United Kingdom data center market.

Tier 3 accounted for 77.92% United Kingdom data center market share in 2025, underpinning the core colocation offer of concurrent maintainability at a cost-effective redundancy level. Nevertheless, hyperscale AI training, high-frequency trading, and regulated workloads elevate the business case for Tier 4. The United Kingdom data center market size attributable to Tier 4 is set to expand from 892 MW in 2026 to 3,474 MW by 2031, reflecting a 31.25% CAGR.

Tier 4 adoption hinges on fully independent dual power paths, fault-tolerant cooling, and 99.995% uptime SLAs that minimize downtime costs measured in millions per hour for AI model retraining or financial order-book slippage. Operators proactively retrofit Tier 3 halls with additional UPS strings and looped chilled-water rings to bridge the redundancy gap while preserving sunk capex. London's regulatory recognition of data centers as Critical National Infrastructure accelerates this trend, as mission-critical tenants demand the highest assurance levels for cybersecurity and operational resilience.

List of Companies Covered in this Report:

- Digital Realty Trust Inc.

- Equinix, Inc.

- VIRTUS Data Centres Ltd (ST Telemedia Global Data Centres)

- IBM Corporation

- Ark Data Centres

- Vantage Data Centers Management Company, LLC

- NTT Corporation

- CyrusOne LLC

- Redcentric Data Centres

- Rackspace Technology Inc.

- Green Mountain AS

- Global Switch Holdings Limited

- Amazon Web Services, Inc.

- Telehouse International Corporation of Europe Ltd

- Oracle Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition - Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in hyperscale cloud and AI compute demand

- 4.2.2 Growth of 5G and edge computing across the United Kingdom

- 4.2.3 Rising adoption of hybrid IT among BFSI and enterprise segments

- 4.2.4 Government incentives for digital infrastructure and the National Planning Framework

- 4.2.5 Proliferation of new submarine-cable landings on the United Kingdom east coast

- 4.2.6 Repurposing of legacy industrial estates into AI-ready campuses in northern England

- 4.3 Market Restraints

- 4.3.1 Power-grid connection delays in London availability zones

- 4.3.2 Escalating construction and energy costs

- 4.3.3 Stringent sustainability and carbon-reduction regulations

- 4.3.4 Skilled-labour shortage for liquid-cooling and high-density operations outside London

- 4.4 Market Outlook

- 4.4.1 IT Load Capacity

- 4.4.2 Raised Floor Space

- 4.4.3 Colocation Revenue

- 4.4.4 Installed Racks

- 4.4.5 Rack Space Utilization

- 4.4.6 Submarine Cable

- 4.5 Key Industry Trends

- 4.5.1 Smartphone Users

- 4.5.2 Data Traffic Per Smartphone

- 4.5.3 Mobile Data Speed

- 4.5.4 Broadband Data Speed

- 4.5.5 Fiber Connectivity Network

- 4.5.6 Regulatory Framework

- 4.5.6.1 Greater London

- 4.5.6.2 Rest of United Kingdom

- 4.6 Value Chain and Distribution Channel Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (MEGAWATT)

- 5.1 By Data Center Size

- 5.1.1 Small

- 5.1.2 Medium

- 5.1.3 Large

- 5.1.4 Mega

- 5.1.5 Massive

- 5.2 By Tier Type

- 5.2.1 Tier 1 and 2

- 5.2.2 Tier 3

- 5.2.3 Tier 4

- 5.3 By Data Center Type

- 5.3.1 Hyperscale / Self-built

- 5.3.2 Enterprise / Edge

- 5.3.3 Colocation

- 5.3.3.1 Non-Utilized

- 5.3.3.2 Utilized

- 5.3.3.2.1 Retail Colocation

- 5.3.3.2.2 Wholesale Colocation

- 5.4 By End User

- 5.4.1 BFSI

- 5.4.2 IT and ITES

- 5.4.3 E-Commerce

- 5.4.4 Government

- 5.4.5 Manufacturing

- 5.4.6 Media and Entertainment

- 5.4.7 Telecom

- 5.4.8 Other End Users

- 5.5 By Hotspot

- 5.5.1 Greater London

- 5.5.2 Rest of United Kingdom

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Digital Realty Trust Inc.

- 6.4.2 Equinix, Inc.

- 6.4.3 VIRTUS Data Centres Ltd (ST Telemedia Global Data Centres)

- 6.4.4 IBM Corporation

- 6.4.5 Ark Data Centres

- 6.4.6 Vantage Data Centers Management Company, LLC

- 6.4.7 NTT Corporation

- 6.4.8 CyrusOne LLC

- 6.4.9 Redcentric Data Centres

- 6.4.10 Rackspace Technology Inc.

- 6.4.11 Green Mountain AS

- 6.4.12 Global Switch Holdings Limited

- 6.4.13 Amazon Web Services, Inc.

- 6.4.14 Telehouse International Corporation of Europe Ltd

- 6.4.15 Oracle Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment