PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066617

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066617

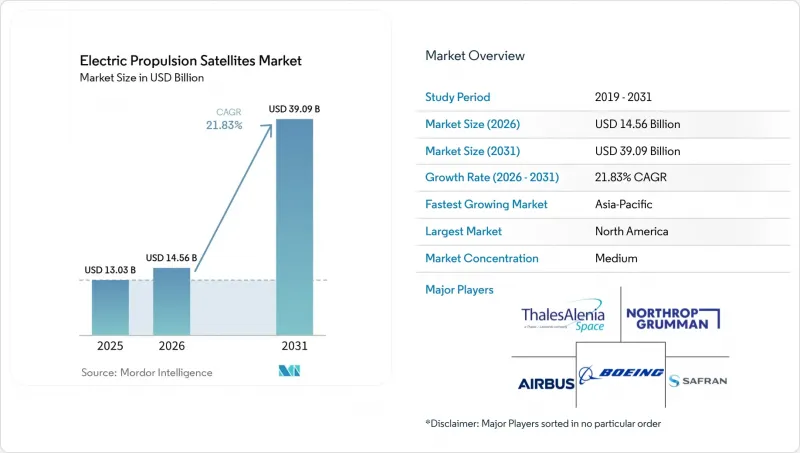

Electric Propulsion Satellites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the electric propulsion satellites market size was valued at USD 13.03 billion in 2025 and is projected to grow from USD 14.56 billion in 2026 to USD 39.09 billion by 2031, at a CAGR of 21.83% during 2026 to 2031.

This report is Segmented by Propulsion Technology (Hall-Effect Thrusters, Gridded Ion Thrusters, and More), Satellite Mass (Small, Medium, and Large), Application (Communication, Earth Observation and Remote Sensing, and More), End User (Commercial and Government and Defense), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Electric Propulsion Satellites Market Trends and Insights

Rapid Growth of LEO Broadband Mega-constellations

The rapid expansion of low Earth orbit (LEO) broadband mega-constellations is a significant driver for the electric propulsion satellites market. Large constellation operators increasingly rely on efficient propulsion technologies to support high-volume satellite deployment and long-term fleet management. SpaceX and Amazon have both moved their constellations into a deployment phase where propulsion demand is tied to repeat launch cadence and fleet replenishment rather than one-time spacecraft procurement. The primary demand driver is the simultaneous deployment of multiple competing broadband constellations, each requiring hundreds of satellites equipped with electric propulsion systems. Electric propulsion systems facilitate orbit raising, station keeping, collision avoidance, and controlled end-of-life disposal while reducing spacecraft mass and enhancing payload efficiency. As operators expand global broadband networks through multi-satellite architectures, the focus is shifting from limited satellite production to industrial-scale deployment models. This shift is driving increased adoption of electric propulsion solutions due to their operational efficiency, lower launch costs, and suitability for constellation-based missions.

Launch Cost Savings via Lighter All-electric Satellites

The electric propulsion satellites market is also benefiting from all-electric and hybrid-electric spacecraft designs that reduce the propellant mass needed on board and free more of the satellite for payload and mission hardware. The HEMPT-NG project noted that all electric satellites can save up to 80% of propellant mass compared to chemical alternatives, strengthening the business case for electric systems beyond simple launch price comparisons. SpaceX's reporting on a lighter V2 Mini configuration shows how iterative mass reduction can directly improve spacecraft packing per launch, which further reinforces the value of electric architecture at scale. Hence, buyers increasingly treat propulsion choice as a core financial decision in the electric propulsion satellites market rather than merely an engineering trade-off.

Space-debris Driven Licensing Hurdles

Stringent debris compliance rules are constraining the electric propulsion satellites market, as operators must now demonstrate disposal capability and propulsion reliability earlier in the licensing process. The FCC's five-year post-mission disposal rule for new LEO satellite licenses became effective in September 2024, which turned propulsion from a performance enhancer into a compliance-relevant subsystem for many missions. In the electric propulsion satellites market, that rule tends to favor established suppliers, because qualification campaigns, endurance testing, and insurer review are expensive and time-consuming for new entrants with limited flight heritage. Smaller operators and newer thruster developers therefore face a harder path to commercial acceptance, even when their technology offers real cost or mass advantages. The electric propulsion satellites market still benefits in the long run because compliance increases the need for onboard propulsion, but the near-term effect is a more selective procurement environment. Standards such as ISO 24113 and ISO 26872 reinforce this direction by raising the minimum expectation for debris mitigation performance and spacecraft operations discipline.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for High-throughput Data Services

- Government Deep-space Exploration Initiatives

- High Development Cost of EP Subsystems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hall-effect thrusters led this segment with 48.20% of revenue in 2025, which kept them at the center of the electric propulsion satellites market across commercial and government programs. Their position reflects a long record in GEO communications, scientific missions, and large-scale constellation use, where buyers value a balance of thrust density, specific impulse, and manageable production scale. In the electric propulsion satellites market, that combination keeps Hall systems attractive for satellite classes that need practical maneuvering capability without moving into the highest-complexity range. Gridded ion thrusters still play an important role in missions where very high specific impulse and mission endurance justify the added subsystem complexity. HEMPT is the fastest-growing propulsion type in this segment, with the electric propulsion satellites market for HEMPT projected to expand at a 22.71% CAGR through 2031. Thales and the European Commission have both highlighted HEMPT's core advantages, especially erosion-free plasma confinement and the ability to operate with xenon, krypton, and argon without redesign, which directly addresses lifetime and supply concerns. In the electric propulsion satellites industry, multi-propellant flexibility matters because customers want fewer design changes when they shift fuel strategy across mission sets.

Medium-weight satellites (500 kg to less than 2,000 kg) accounted for 52.45% of revenue in 2025, making them the largest mass class in the electric propulsion satellites market, reflecting the continued relevance of GEO communications buses and medium LEO platforms, both of which still generate meaningful propulsion demand because they combine long operating lives with more capable mission profiles. In the electric propulsion satellites market, medium-class platforms also benefit from the widest pool of qualified propulsion options, especially Hall systems that already support orbit raising, station keeping, and life extension.

Small satellites are the fastest-growing mass class, with the electric propulsion satellites market for this category projected to grow at a 22.83% CAGR from 2026 to 2031. The main driver is the continued spread of broadband, earth observation, and defense-related constellations, where fleet counts are rising quickly, and propulsion systems must meet strict mass, power, and volume limits. In the electric propulsion satellites market, this changes supplier requirements because many heritage systems were designed for larger buses and do not translate cleanly into compact platforms.

Geography Analysis

North America held 53.77% of the global electric propulsion satellites market in 2025, making it the leading regional center for both demand and propulsion subsystem production. The region benefits from the concentration of major constellation operators, a dense base of spacecraft manufacturers, and steady procurement from NASA, the Space Development Agency, and the US Space Force. The US remains the core national market in the region because Starlink deployment alone creates significant recurring demand for in-house propulsion capability, fleet replenishment, and related power-processing hardware. The electric propulsion satellites market in North America is also shaped by stronger domestic supply preferences, especially where government procurement prioritizes local manufacturing and documented heritage. Safran's Colorado production move shows how suppliers are responding to that demand by building US manufacturing capacity closer to end customers in the small satellite segment.

Europe remained the second-largest region in the electric propulsion satellites market, supported by a long-standing industrial base across propulsion, satellite manufacturing, and public research funding. The region's position is reinforced by companies such as Thales Alenia Space, Safran, OHB, and ArianeGroup, as well as European Commission-backed programs that continue to support next-generation propulsion work. CORDIS-backed projects such as HEMPT-NG and related development programs have helped keep Europe competitive in propellant-flexible, lifetime-oriented electric propulsion designs. South America is still a small contributor to the electric propulsion satellites market. Still, its long-term position is improving as lower launch costs and broader connectivity needs make smaller satellite programs more practical.

Asia-Pacific is the fastest-growing region, with the electric propulsion satellites market in this geography expected to expand at a 24.63% CAGR through 2031. China is a major driver because state-directed commercial constellations and domestic propulsion development are advancing in tandem, providing local thruster suppliers a path from research to repeat deployment. India is also strengthening regional momentum through ISRO's propulsion capabilities and a broader domestic push for space manufacturing. Japan adds another important dimension to the electric propulsion satellites market through ETS-9, where JAXA has highlighted the role of long-life Hall thruster capability in building domestic commercial relevance. The Middle East and Africa remain an emerging geography in the electric propulsion satellites market, with demand likely to come mainly from satellite procurement by established primes rather than from local propulsion manufacturing in the near term.

- Airbus SE

- Thales Alenia Space

- The Boeing Company

- Northrop Grumman Corporation

- Lockheed Martin Corporation

- L3Harris Technologies, Inc.

- Maxar Technologies (Vantor Holdings Inc.)

- OHB SE

- Blue Canyon Technologies LLC (RTX Corporation)

- Safran SA

- ArianeGroup SAS

- Busek Co. Inc.

- Sitael S.p.A

- Orbion Space Technology

- Rocket Lab USA, Inc.

- Enpulsion GmbH

- UAB Kongsberg NanoAvionics (Kongsberg Gruppen ASA)

- York Space Systems Inc.

- DFH Satellite Co. Ltd.

- Space Exploration Technologies Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid growth of LEO broadband mega-constellations

- 4.2.2 Rising demand for high-throughput data services

- 4.2.3 Launch cost savings via lighter all-electric satellites

- 4.2.4 Government deep-space exploration initiatives

- 4.2.5 Adoption of iodine and krypton propellants

- 4.2.6 Electric propulsion-enabled on-orbit servicing and debris removal

- 4.3 Market Restraints

- 4.3.1 Space-debris driven licensing hurdles

- 4.3.2 Xenon supply constraints and price volatility

- 4.3.3 High development cost of electric propulsion subsystems

- 4.3.4 Insurance qualification hurdles for new electric propulsion technology

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Propulsion Technology

- 5.1.1 Hall-Effect Thrusters

- 5.1.2 Gridded Ion Thrusters

- 5.1.3 High-Efficiency Multi-Stage Plasma Thrusters (HEMPT)

- 5.1.4 Pulsed Plasma Thrusters (PPT)

- 5.1.5 Others

- 5.2 By Satellite Mass

- 5.2.1 Small (Less than 500 kg)

- 5.2.2 Medium (500 kg to Less than 2,000 kg)

- 5.2.3 Large (More than 2,000 kg)

- 5.3 By Application

- 5.3.1 Communication

- 5.3.2 Earth Observation and Remote Sensing

- 5.3.3 Navigation and PNT

- 5.3.4 Science and Exploration

- 5.3.5 Technology Demonstration

- 5.4 By End User

- 5.4.1 Commercial

- 5.4.2 Government and Defense

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Italy

- 5.5.2.5 Russia

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, and Recent Developments)

- 6.4.1 Airbus SE

- 6.4.2 Thales Alenia Space

- 6.4.3 The Boeing Company

- 6.4.4 Northrop Grumman Corporation

- 6.4.5 Lockheed Martin Corporation

- 6.4.6 L3Harris Technologies, Inc.

- 6.4.7 Maxar Technologies (Vantor Holdings Inc.)

- 6.4.8 OHB SE

- 6.4.9 Blue Canyon Technologies LLC (RTX Corporation)

- 6.4.10 Safran SA

- 6.4.11 ArianeGroup SAS

- 6.4.12 Busek Co. Inc.

- 6.4.13 Sitael S.p.A

- 6.4.14 Orbion Space Technology

- 6.4.15 Rocket Lab USA, Inc.

- 6.4.16 Enpulsion GmbH

- 6.4.17 UAB Kongsberg NanoAvionics (Kongsberg Gruppen ASA)

- 6.4.18 York Space Systems Inc.

- 6.4.19 DFH Satellite Co. Ltd.

- 6.4.20 Space Exploration Technologies Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment