PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066634

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066634

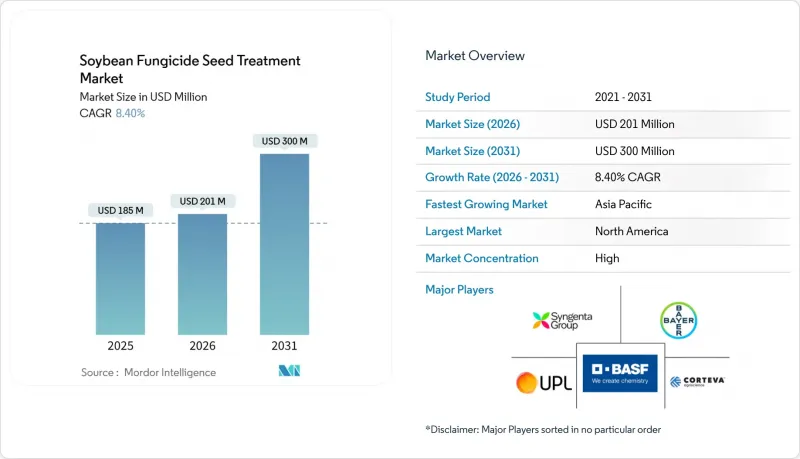

Soybean Fungicide Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the soybean fungicide seed treatment market was valued at USD 185 million in 2025 and is projected to grow from USD 201 million in 2026 to USD 300 million by 2031, registering a CAGR of 8.4% from 2026 to 2031.

This report is Segmented by Type (Chemicals and Non-Chemical/Biological), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Soybean Fungicide Seed Treatment Market Trends and Insights

Increasing Incidence of Fungicide-Resistant Phytophthora sojae Strains

Field surveys have identified multiple Phytophthora sojae pathotypes capable of overcoming long-standing Rps genes, reducing genetic resistance, and driving growers toward multi-mode seed treatments. Variability is accelerating the adoption of stacked chemistries that combine phenylamides with ethaboxam and biological antagonists. Additionally, South American researchers have reported azoxystrobin-resistant Colletotrichum truncatum, highlighting the need for new active ingredients. Pathogen populations are evolving more rapidly than the introduction of new active ingredients to the market, prompting growers to adopt seed treatments with multiple modes of action.

Growing Demand for High-Quality Crop Yields

Exporters are facing stricter regulations on mycotoxins and protein variability, making seed treatment an essential quality assurance measure. For instance, Chinese importers often reject shipments containing deoxynivalenol levels exceeding 1 part per million, a risk mitigated by managing Fusarium infections during germination. In Argentina, producers aiming for premium contracts with European crushers have standardized seed treatment practices across multiplication plots. According to seed companies, most of the foundation seed lots are now treated to ensure varietal purity.

Adverse Effects of Chemical Fungicides on Soil Microbiota

The application of chemical fungicide seed treatments in soybean cultivation is facing growing limitations due to their negative impact on beneficial soil microbiota, particularly nitrogen-fixing Rhizobium species. These fungicides can interfere with root nodulation, thereby reducing the efficiency of biological nitrogen fixation. According to a study published in Bioscience, soybean seeds treated with fungicides exhibited a 36% decrease in root nodules, adversely affecting plant-microbe symbiosis and nutrient absorption . This reduction can constrain yields in low-fertility soils, leading to increased regulatory scrutiny and driving the adoption of microbiome-friendly or biological seed treatment alternatives.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidies for Seed-Treatment Adoption

- Expansion of Cold-Plasma Coating Technologies

- Stringent Regulations on Agrochemicals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chemical formulations accounted for the largest market share, at 68%, for the soybean fungicide seed treatment market in 2025. Meanwhile, the biological market size is projected to grow at the fastest CAGR of 9.3% from 2026 to 2031. Triazole and phenylamide combinations continue to be widely used for managing Phytophthora and Rhizoctonia due to their extensive field history, cost-effectiveness per hectare, and broad regulatory approvals, making them a staple across commodity crops. However, resistance concerns in Brazil and the United States are driving the adoption of rotation and stacking practices, encouraging growers to opt for premium multi-active blends.

Biological seed treatments include living microbes such as Bacillus and Trichoderma, along with fermentation-derived metabolites. Examples like Corteva Agriscience's Pseudomonas-based Lumisena and Syngenta's Bacillus-based Saltro highlight the growing adoption of high-performance biofungicides. Advances in encapsulation technologies, such as alginate matrices, have improved shelf life and on-seed viability. If efficacy continues to improve, biological seed treatments could achieve a comparable market share by 2031, shifting competition toward companies with extensive microbial libraries and large-scale fermentation capabilities.

Geography Analysis

North America accounted for the largest market share of 34% for soybean fungicide seed treatment revenue in 2025, driven by widespread coating practices across the Corn Belt and Prairie provinces. Growth through 2031 is projected to be moderate due to saturated acreage. However, premiumization trends are evident as processors adopt atmospheric-pressure cold-plasma units, which enhance germination and reduce synthetic inputs. Additionally, subsidies linked to climate-smart agriculture are facilitating the transition to biological and precision-applied stacks, helping to sustain revenue even as planted hectares stabilize.

The Asia-Pacific market size is projected to grow at the fastest CAGR of 9.8% from 2026 to 2031, as growers address challenges such as Asian soybean rust, Phytophthora root rot, and Diaporthe stem canker. India and China are at earlier stages of adoption, with lower penetration rates. However, government initiatives providing subsidized treated seeds to smallholders are helping to close the gap. In Brazil, where approximately three-quarters of soybean seeds are already coated, rising disease pressure in regions like Mato Grosso and Parana supports continued volume growth, alongside a shift toward multi-active or biological products.

Europe and the Middle East and Africa are projected to experience slower growth, due to smaller soybean acreage and stricter residue regulations under the Farm to Fork strategy, which is phasing out several triazoles. In Europe, organic and integrated pest management producers in countries such as Germany, France, and Italy are early adopters of microbial coatings from BASF SE agricultural solutions and Novozymes, though overall volumes remain limited. In Africa, irrigation-dependent regions in Egypt and South Africa rely on seed treatments to mitigate high pathogen pressure, while Turkey is emerging as a formulation hub serving neighboring markets.

- Syngenta Group Co., Ltd.

- Bayer AG

- BASF SE

- Corteva, Inc.

- UPL Limited

- Sumitomo Chemical Company, Limited

- FMC Corporation

- Nufarm Limited

- Novozymes A/S

- Pro Farm Group Inc.

- Valent U.S.A. LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing incidence of fungicide-resistant Phytophthora sojae strains

- 4.2.2 Growing demand for high-quality crop yields

- 4.2.3 Government subsidies for seed-treatment adoption

- 4.2.4 Expansion of cold-plasma coating technologies

- 4.2.5 Adoption of drone-enabled seed pelleting

- 4.2.6 Integration of RNA-based fungicides into seed-treatment stacks

- 4.3 Market Restraints

- 4.3.1 Adverse effects of chemical fungicides on soil microbiota

- 4.3.2 Stringent regulations on agrochemicals

- 4.3.3 Supply-chain volatility for key triazole actives

- 4.3.4 Farmer perception of phytotoxicity in low-organic-matter soils

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Force Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 Type

- 5.1.1 Chemical

- 5.1.2 Non-Chemical/Biological

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of North America

- 5.2.2 South America

- 5.2.2.1 Brazil

- 5.2.2.2 Argentina

- 5.2.2.3 Rest of South America

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Spain

- 5.2.3.5 Italy

- 5.2.3.6 Russia

- 5.2.3.7 Rest of Europe

- 5.2.4 Asia-Pacific

- 5.2.4.1 China

- 5.2.4.2 Japan

- 5.2.4.3 India

- 5.2.4.4 Thailand

- 5.2.4.5 Vietnam

- 5.2.4.6 Australia

- 5.2.4.7 Rest of Asia-Pacific

- 5.2.5 Middle East

- 5.2.5.1 Turkey

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 Rest of Middle East

- 5.2.6 Africa

- 5.2.6.1 South Africa

- 5.2.6.2 Egypt

- 5.2.6.3 Rest of Africa

- 5.2.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Syngenta Group Co., Ltd.

- 6.4.2 Bayer AG

- 6.4.3 BASF SE

- 6.4.4 Corteva, Inc.

- 6.4.5 UPL Limited

- 6.4.6 Sumitomo Chemical Company, Limited

- 6.4.7 FMC Corporation

- 6.4.8 Nufarm Limited

- 6.4.9 Novozymes A/S

- 6.4.10 Pro Farm Group Inc.

- 6.4.11 Valent U.S.A. LLC

7 Market Opportunities and Future Outlook