PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073454

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073454

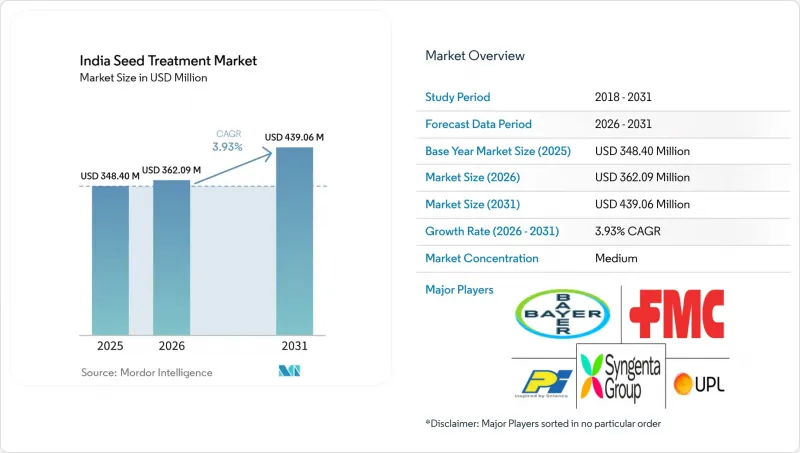

India Seed Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, india seed treatment market size in 2026 is estimated at USD 362.09 million, growing from 2025 value of USD 348.4 million with 2031 projections showing USD 439.06 million, growing at 3.93% CAGR over 2026-2031.

This report is Segmented by Function (Fungicide, Insecticide, and Nematicide), Crop Type (Commercial Crops, Fruits and Vegetables, Grains and Cereals, Pulses and Oilseeds, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume(Metric Tons).

India Seed Treatment Market Trends and Insights

Biological seed treatment adoption

Biological seed treatments are reshaping the India seed treatment market by offering sustained plant health benefits that extend beyond short-term pest knockdown. Fast-tracked registration processes now clear well-characterized microbial strains in 12-18 months, half the earlier period, cutting compliance costs . Farmers favor Bacillus- and Trichoderma-based products for cotton, soybean, and vegetables because they enhance root vigor, nutrient uptake, and drought resilience. Export-oriented growers appreciate these residue-free treatments in meeting the stringent maximum residue limits enforced by the European Union. Federal subsidies covering 50% of certified biological input costs in Karnataka and Maharashtra further accelerate adoption. As a result, the India seed treatment market is rapidly shifting from purely chemical options toward integrated biological portfolios that align with sustainable agriculture goals.

Increasing precision agriculture adoption

Precision agriculture technologies are revolutionizing seed treatment application methods, enabling variable-rate treatments based on field-specific pest pressure and soil conditions. The integration of drone-based scouting and GPS-guided planting equipment allows farmers to optimize treatment rates, reducing input costs while maintaining efficacy levels. This technological convergence particularly benefits large-scale commercial crop producers in Punjab, Haryana, and western Maharashtra, where mechanized farming operations can leverage precision application systems effectively. The trend accelerates as equipment costs decline and technical support infrastructure expands through government-backed agricultural technology centers. Precision application also addresses regulatory concerns about chemical residues by ensuring optimal dosing that minimizes environmental impact while maximizing crop protection benefits.

Raw Material Price Volatility from Imports

Import dependency for technical-grade active ingredients creates significant cost pressures that constrain market expansion and limit farmer adoption of premium seed treatments. India imports approximately 70% of technical-grade pesticide ingredients, with China supplying over 60% of these materials, creating vulnerability to supply chain disruptions and price fluctuations. The 2024 disruptions in Chinese manufacturing due to environmental regulations resulted in 25-40% price increases for key active ingredients, including imidacloprid and thiamethoxam, forcing domestic formulators to either absorb costs or pass increases to farmers. This volatility particularly impacts smaller domestic companies lacking financial buffers to manage input cost fluctuations, potentially leading to market consolidation favoring larger players with stronger balance sheets. Currency fluctuations add another layer of complexity, with rupee depreciation against the Chinese yuan directly impacting import costs for seed treatment manufacturers.

Other drivers and restraints analyzed in the detailed report include:

- Government Support for Sustainable Formulations

- Export demand for residue-compliant produce

- Regulatory Approval Complexities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Insecticides command an overwhelming 89.60% market share in 2025, reflecting India's persistent battle against crop-damaging pests and the critical importance of early-stage plant protection in determining final yields. The segment's 3.99% CAGR through 2031 indicates sustained growth driven by expanding acreage under commercial crops and increasing pest pressure from climate variability. This dominance stems from the immediate and visible impact of insecticidal seed treatments in preventing seedling mortality from soil-dwelling pests like termites, wireworms, and cutworms that can devastate crop establishment across diverse agro-climatic zones. Neonicotinoid-based treatments, particularly imidacloprid and thiamethoxam formulations, maintain preference among farmers for their systemic action and extended protection periods, despite regulatory scrutiny in international markets.

Fungicides represent a smaller but strategically important segment, addressing seed and soil-borne diseases that cause significant yield losses in high-moisture environments and intensive cropping systems. The segment benefits from increasing awareness of fungal resistance management and the need for preventive disease control strategies that reduce subsequent foliar applications. Nematicides occupy a niche position, primarily used in high-value crops like vegetables and commercial crops where nematode damage justifies premium treatment costs. The Indian Council of Agricultural Research's emphasis on integrated pest management creates opportunities for combination treatments that address multiple pest categories simultaneously, potentially reshaping traditional functional segmentation.

Complete Report Scope:

- Function

- Fungicides

- Insecticides

- Nematicide

- Crop Type

- Commercial Crops

- Fruits & Vegetables

- Grains & Cereals

- Pulses & Oilseeds

- Turf & Ornamental

List of Companies Covered in this Report:

- ADAMA Agricultural Solutions Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- Crystal Crop Protection Ltd

- FMC Corporation

- PI Industries

- Rallis India Ltd

- Syngenta Group

- UPL Limited

- Dhanuka Agritech Ltd

- Sumitomo Chemical India Ltd

- Nagarjuna Agrichem Ltd

- Bharat Rasayan Ltd

- Meghmani Organics Ltd

- NACL Industries Ltd

- Sharda Cropchem Ltd

- Gharda Chemicals Ltd

- Tagros Chemicals India Pvt Ltd

- Willowood Chemicals Pvt Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 India

- 4.4 Value Chain & Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Biological seed treatment adoption

- 4.5.2 Precision agriculture integration

- 4.5.3 Government support for sustainable inputs

- 4.5.4 Export demand for residue-compliant produce

- 4.5.5 Seed-coating technology innovation

- 4.5.6 Integrated pest management programs

- 4.6 Market Restraints

- 4.6.1 Raw material price volatility from imports

- 4.6.2 Regulatory approval complexities

- 4.6.3 Fragmented distribution networks in eastern states

- 4.6.4 Currency fluctuations raising import costs

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Function

- 5.1.1 Fungicides

- 5.1.2 Insecticides

- 5.1.3 Nematicide

- 5.2 Crop Type

- 5.2.1 Commercial Crops

- 5.2.2 Fruits & Vegetables

- 5.2.3 Grains & Cereals

- 5.2.4 Pulses & Oilseeds

- 5.2.5 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 ADAMA Agricultural Solutions Ltd

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Crystal Crop Protection Ltd

- 6.4.6 FMC Corporation

- 6.4.7 PI Industries

- 6.4.8 Rallis India Ltd

- 6.4.9 Syngenta Group

- 6.4.10 UPL Limited

- 6.4.11 Dhanuka Agritech Ltd

- 6.4.12 Sumitomo Chemical India Ltd

- 6.4.13 Nagarjuna Agrichem Ltd

- 6.4.14 Bharat Rasayan Ltd

- 6.4.15 Meghmani Organics Ltd

- 6.4.16 NACL Industries Ltd

- 6.4.17 Sharda Cropchem Ltd

- 6.4.18 Gharda Chemicals Ltd

- 6.4.19 Tagros Chemicals India Pvt Ltd

- 6.4.20 Willowood Chemicals Pvt Ltd

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS