PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066637

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066637

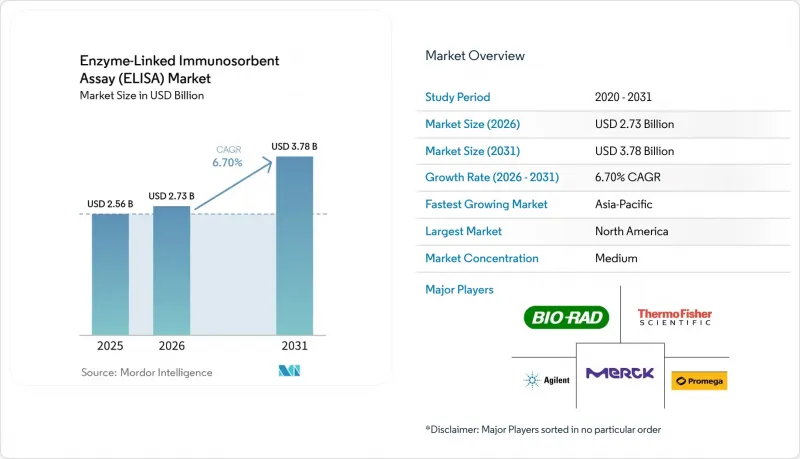

Enzyme-Linked Immunosorbent Assay (ELISA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the enzyme-Linked immunosorbent assay (ELISA) market size was valued at USD 2.56 billion in 2025 and is estimated to grow from USD 2.73 billion in 2026 to reach USD 3.78 billion by 2031, at a CAGR of 6.70% during the forecast period (2026-2031).

This report is Segmented by Product Type (Kits & Reagents, Instruments, Software & Services), Assay Technique (Sandwich, Direct, Indirect, Competitive), Application (Diagnostics, Drug Development & Quality Control, Research Use), End User (Hospitals & Clinics, and More), and Geography (North America, Europe, and More ). The Market Forecasts are Provided in Terms of Value (USD).

Global Enzyme-Linked Immunosorbent Assay (ELISA) Market Trends and Insights

Growing prevalence of chronic & infectious diseases

Rising incidences of diabetes, cardiovascular disorders, and persistent viral infections are pushing healthcare providers to embed ELISA into routine population-health programs. National screening agendas in India and China are scaling up biomarker testing volume, with ELISA favored for its validated protocols and low per-test cost, especially when budgets constrain the uptake of newer chemiluminescent systems. Hospital networks in the Middle East are integrating ELISA panels for hepatitis and HIV monitoring within universal-testing rollouts, lifting reagent consumption. Multilateral donors are also financing ELISA-based tuberculosis surveillance in sub-Saharan Africa, enlarging the installed base. The combined effect is a stable sample-volume pipeline that cushions market revenue against cyclical R&D spending patterns.

High-throughput automated ELISA workstations

Automation addresses the chronic shortage of qualified technicians and reduces error rates linked to manual pipetting. Leading platforms now process up to 960 wells per hour with integrated barcode tracking and AI-led result validation, cutting turnaround time by more than 30% for large reference labs. Cost-benefit analyses in US hospital chains show a two-year payback when daily test load exceeds 1,500 samples. European laboratories are layering middleware that feeds results directly into electronic medical records, improving clinical decision efficiency. Asian contract research organizations are adopting lease models that bundle instrumentation, software, and reagents, lowering upfront capital barriers and accelerating penetration.

Cross-reactivity & false positives

Overlap in epitope binding can trigger misleading results, especially when analyte concentration is low or sample matrices are heterogeneous. Clinical laboratories now mandate confirmatory testing for critical biomarkers, adding process steps that inflate operating costs. Regulators responded with tighter validation guidance in 2024, raising the bar for commercial kit launch approvals. Manufacturers counter with high-affinity recombinant antibody pairs and refined blocking buffers, yet performance variability persists among lower-priced kits, complicating procurement decisions for price-sensitive hospitals. The resultant skepticism nudges some institutions toward chemiluminescent formats with broader dynamic range.

Other drivers and restraints analyzed in the detailed report include:

- Companion diagnostics demand in immuno-oncology

- Multiplex ELISA panels for immunotherapy monitoring

- Shift to multiplex bead & CLIA platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Kits & reagents generated 46.95% of the ELISA market in 2025, powered by their recurring-revenue profile and broad menu coverage. Instruments, although representing a smaller installed-base value, are forecast to outpace consumables at a 7.05% CAGR as laboratories pursue automation. The ELISA market size for high-capacity analyzers is expected to reach USD 1.69 billion by 2031, reflecting bundled software and service contracts that lift average selling prices. Vendors now embed cloud analytics for remote calibration and predictive maintenance, shrinking downtime to enhance lab productivity.

Large hospital networks pursue multi-plate robotics that unify microplate washing, incubation, and optical detection, trimming technician hours by up to 40%. Subscription models offer predictable cash flow for suppliers and smoother capital budgeting for customers. Emerging Asian labs, where capital budgets remain constrained, are adopting staged-upgrade pathways: entry-level semi-automated readers today, scalable to full robotics upon volume escalation. Reagent manufacturers collaborate with instrument partners to pre-validate kit compatibility, ensuring plug-and-play deployment and shortening verification cycles.

Sandwich assays still anchor 35.65% of 2025 revenue, preferred for large protein detection owing to dual-antibody specificity. Competitive ELISA, however, expands at 7.28% CAGR as pharmaceutical clients require low-molecular-weight drug quantification during pharmacokinetic studies. Direct ELISA finds traction in rapid toxin screens, while indirect formats remain standard for serological surveillance of emerging pathogens.

Technique selection increasingly hinges on regulatory precedent. Competitive formats enjoy entrenched FDA-cleared protocols for therapeutic drug monitoring, smoothing submission dossiers for new generics. Academic research groups appreciate the technique's tolerance for small antigen targets, fueling catalog diversification among mid-tier kit suppliers. Detection chemistries also evolve: colorimetric substrates give way to amplified fluorescence, extending detection limits and pulling ELISA closer to CLIA performance without overhaul of legacy plate readers.

Geography Analysis

North America generated 41.85% of 2025 revenue and retains leadership through 2031, supported by elevated per-capita healthcare spending and the concentration of top IVD manufacturers. Clinical laboratories readily adopt next-generation instruments, and payors reimburse specialized assays, sustaining premium pricing. Government initiatives to fortify pandemic readiness cement ELISA as a backbone technology within national stockpiles.

Asia-Pacific advances at an 8.12% CAGR, the highest regional pace. China's "Healthy China 2030" blueprint funds hospital immunology labs in secondary cities, lifting capital equipment imports. India's Ayushman Bharat scheme broadens insurance coverage, unlocking rural diagnostic demand met by decentralized ELISA-on-chip devices distributed via primary health centers. Japan and South Korea emphasize automation upgrades, leveraging domestic robotics expertise to raise throughput while offsetting technician shortages; Australia maintains stable demand through public-private pathology partnerships that prioritize assay standardization.

Europe demonstrates balanced growth under the new IVDR that requires higher clinical-evidence thresholds. Germany's manufacturing prowess secures supply chain resilience for regional kit production. The United Kingdom channels Life Sciences Vision funding into oncology biomarker research, inflating competitive ELISA kit usage. Southern European nations roll out EU-supported modernization grants, updating public hospital labs with automated workstations. South America and Middle East & Africa contribute incremental gains as economic headwinds stabilize; multinational NGOs deploy ELISA for surveillance of vector-borne diseases, expanding the installed base that vendors can later monetize with consumables.

- Thermo Fisher Scientific

- Danaher Corp. (Beckman Coulter)

- Roche

- Merck

- Bio-Rad Laboratories

- PerkinElmer

- Bio-Techne Corp. (R&D Systems)

- Abcam

- Agilent Technologies

- Enzo Biochem

- Beckton Dickinson

- Siemens Healthineers

- QuidelOrtho Corp.

- Mindray

- RayBiotech Life, Inc.

- Eurofins

- OriGene Technologies

- Creative Diagnostics

- Promega

- Elabscience Biotechnology Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing prevalence of chronic & infectious diseases

- 4.2.2 Rapid penetration of high-throughput automated ELISA workstations

- 4.2.3 Rising demand for companion diagnostics in immuno-oncology

- 4.2.4 Multiplex ELISA panels for immunotherapy monitoring (under-reported)

- 4.2.5 Cost-efficient recombinant/plant-derived antibodies for ELISA kits (under-reported)

- 4.2.6 Decentralised POC ELISA-on-chip formats for rural settings (under-reported)

- 4.3 Market Restraints

- 4.3.1 Cross-reactivity & false-positive concerns

- 4.3.2 Growing adoption of next-gen multiplex bead & CLIA platforms

- 4.3.3 Sustainability pressure on single-use micro-plates & plastics (under-reported)

- 4.3.4 Shortage of skilled immunoassay technicians in emerging markets (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Threat of Substitutes

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type (Value)

- 5.1.1 Kits & Reagents

- 5.1.2 Instruments

- 5.1.3 Software & Services

- 5.2 By Assay Technique (Value)

- 5.2.1 Sandwich ELISA

- 5.2.2 Direct ELISA

- 5.2.3 Indirect ELISA

- 5.2.4 Competitive ELISA

- 5.3 By Application (Value)

- 5.3.1 Diagnostics

- 5.3.1.1 Infectious Diseases

- 5.3.1.2 Cancer

- 5.3.1.3 Auto-immune Diseases

- 5.3.1.4 Hormone & Fertility

- 5.3.1.5 Food Allergy

- 5.3.2 Drug Development & Quality Control

- 5.3.3 Research Use

- 5.3.1 Diagnostics

- 5.4 By End User (Value)

- 5.4.1 Hospitals & Clinics

- 5.4.2 Diagnostic Laboratories

- 5.4.3 Pharmaceutical & Biotechnology Companies

- 5.4.4 Contract Research Organisations

- 5.4.5 Academic & Research Institutes

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Thermo Fisher Scientific Inc.

- 6.3.2 Danaher Corp. (Beckman Coulter)

- 6.3.3 F. Hoffmann-La Roche Ltd.

- 6.3.4 Merck KGaA

- 6.3.5 Bio-Rad Laboratories Inc.

- 6.3.6 PerkinElmer Inc.

- 6.3.7 Bio-Techne Corp. (R&D Systems)

- 6.3.8 Abcam plc

- 6.3.9 Agilent Technologies Inc.

- 6.3.10 Enzo Life Sciences Inc.

- 6.3.11 Becton, Dickinson and Company

- 6.3.12 Siemens Healthineers AG

- 6.3.13 QuidelOrtho Corp.

- 6.3.14 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.15 RayBiotech Life, Inc.

- 6.3.16 Eurofins Scientific SE

- 6.3.17 OriGene Technologies Inc.

- 6.3.18 Creative Diagnostics

- 6.3.19 Promega Corporation

- 6.3.20 Elabscience Biotechnology Co. Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment