PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066639

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066639

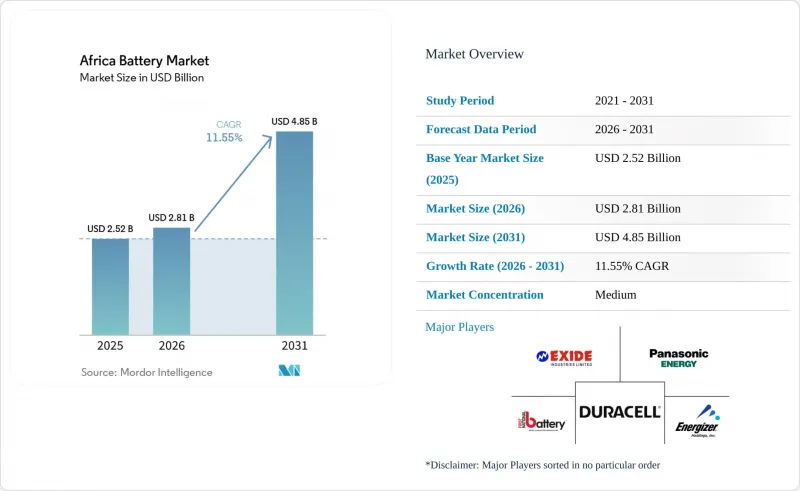

Africa Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the africa battery market size was valued at USD 2.52 billion in 2025 and is estimated to grow from USD 2.81 billion in 2026 to reach USD 4.85 billion by 2031, at a CAGR of 11.55% during the forecast period (2026-2031).

This report is Segmented by Battery Type (Primary Batteries and Secondary Batteries), Technology (Lead-Acid, Li-Ion, Nickel-Metal Hydride, Nickel-Cadmium, Sodium-Sulfur, Solid-State, Flow Battery, and Emerging Chemistries), Application (Automotive, Industrial, Portable, Power Tools, SLI, and Other Applications), and Geography (South Africa, Egypt, Kenya, Nigeria, Morocco, Ethiopia, and Rest of Africa).

Africa Battery Market Trends and Insights

Declining Lithium-Ion Prices

Global pack prices slipped to USD 115 per kWh in 2024 and to USD 94 per kWh in China, finally undercutting diesel gensets for African telecom towers and microgrids. Operators such as MTN and Airtel retrofit sites with lithium-ion systems that last up to 10 years, trimming the total cost of ownership by about 30% and slashing maintenance trips. South African and Egyptian utilities now pair multi-hour storage with solar farms, exemplified by the 540 MW Kenhardt project that integrates 1,140 MWh of batteries to meet evening peaks. Chinese cathode and anode plants opening in Morocco further compress supply-chain costs, creating a virtuous circle of affordability.

Surge in Off-Grid Solar + BESS Deployments

Off-grid solar-plus-storage microgrids are proliferating where extending grids remains uneconomic. Ethiopia targets 35% off-grid electrification by 2030 using solar arrays with 4-8 hour battery reserves. Egypt, Botswana, and Zambia adopted similar models, securing debt from multilateral banks that now view storage cash flows as bankable. Telecom and agricultural cold-chain operators gain uptime improvements that justify higher upfront spend, advancing rural energy access and economic activity.

Raw-Material Supply Bottlenecks

The DRC's 30% processing rule idled cobalt shipments, adding 4-6 week delays and 12% to Asian buyers' landed costs. Zimbabwe's rail capacity caps lithium exports, doubling freight versus Australian peers, while South African manganese miners truck ore because of rail unreliability. Artisanal cobalt, roughly 20% of global supply, now sits in compliance limbo under the EU due diligence law, exposing buyers to legal and reputational risk.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Local Battery Manufacturing

- Rapid Electrification of Two-/Three-Wheelers

- Counterfeit / Low-Quality Battery Influx

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Secondary batteries delivered 86.5% of 2025 revenues, and their 12.1% CAGR is set to reinforce that dominance. Automotive and industrial clients value rechargeability's lower lifetime cost, while lithium-ion replaces lead-acid in high-cycle roles. Primary cells cling to a 13.5% share mainly in low-drain devices. The Africa battery market size for secondary chemistries is projected to eclipse USD 4 billion by 2031, with lithium-ion securing most gains.

The Africa battery market share of primary cells will keep shrinking as extended producer responsibility fees rise in Kenya and South Africa. Lead recyclers such as First National Battery recover 96% of materials, yet lithium-ion recycling remains scarce, signaling an investment opportunity. Gotion's Moroccan plant will shorten delivery times and hedge currency swings, further tilting buyers toward rechargeables.

List of Companies Covered in this Report:

- CATL

- BYD Co. Ltd.

- Panasonic Energy

- Duracell Inc.

- Energizer Holdings Inc.

- Exide Industries Ltd.

- First National Battery (Metair)

- Solar MD

- Uganda Batteries Ltd.

- Chloride Exide Kenya Ltd.

- Luminous Power Technologies

- Murata Manufacturing Co. Ltd.

- East Penn Manufacturing

- EnerSys

- GS Yuasa Corp.

- Gotion High-Tech

- BSL Battery

- Felicity Solar

- Orbit Batteries

- Saft (TotalEnergies)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining lithium-ion prices

- 4.2.2 Surge in off-grid solar + BESS deployments

- 4.2.3 Government incentives for local battery manufacturing

- 4.2.4 Rapid electrification of two-/three-wheelers

- 4.2.5 Telecom-tower retrofit cycle

- 4.2.6 Chinese-backed lithium-processing build-out

- 4.3 Market Restraints

- 4.3.1 Raw-material supply bottlenecks

- 4.3.2 Patchy grid & charging infrastructure

- 4.3.3 Counterfeit/low-quality battery influx

- 4.3.4 Policy fragmentation & weak enforcement

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Battery Type

- 5.1.1 Primary Batteries

- 5.1.2 Secondary Batteries

- 5.2 By Technology

- 5.2.1 Lead-acid

- 5.2.2 Li-ion

- 5.2.3 Nickel-metal hydride

- 5.2.4 Nickel-cadmium

- 5.2.5 Sodium-sulfur

- 5.2.6 Solid-state

- 5.2.7 Flow Battery

- 5.2.8 Emerging chemistries

- 5.3 By Application

- 5.3.1 Automotive (HEV, PHEV, and EV)

- 5.3.2 Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.)

- 5.3.3 Portable (Consumer Electronics, etc.)

- 5.3.4 Power Tools

- 5.3.5 SLI

- 5.3.6 Other Applications

- 5.4 By Geography

- 5.4.1 South Africa

- 5.4.2 Egypt

- 5.4.3 Kenya

- 5.4.4 Nigeria

- 5.4.5 Morocco

- 5.4.6 Ethiopia

- 5.4.7 Rest of Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 CATL

- 6.4.2 BYD Co. Ltd.

- 6.4.3 Panasonic Energy

- 6.4.4 Duracell Inc.

- 6.4.5 Energizer Holdings Inc.

- 6.4.6 Exide Industries Ltd.

- 6.4.7 First National Battery (Metair)

- 6.4.8 Solar MD

- 6.4.9 Uganda Batteries Ltd.

- 6.4.10 Chloride Exide Kenya Ltd.

- 6.4.11 Luminous Power Technologies

- 6.4.12 Murata Manufacturing Co. Ltd.

- 6.4.13 East Penn Manufacturing

- 6.4.14 EnerSys

- 6.4.15 GS Yuasa Corp.

- 6.4.16 Gotion High-Tech

- 6.4.17 BSL Battery

- 6.4.18 Felicity Solar

- 6.4.19 Orbit Batteries

- 6.4.20 Saft (TotalEnergies)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment