PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066648

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066648

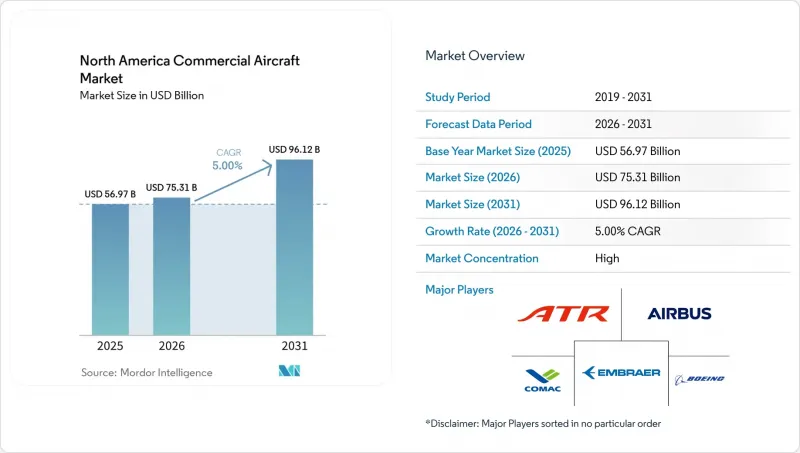

North America Commercial Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america commercial aircraft market size is expected to grow from USD 56.97 billion in 2025 to USD 75.31 billion in 2026 and is forecasted to reach USD 96.12 billion by 2031 at a 5.00% CAGR over 2026-2031.

This report is Segmented by Aircraft Type (Narrowbody, Widebody, and Regional Jets), Application (Passenger and Freighter), Propulsion Type (Turbofan and Turboprop), Component (Airframe Structures, Aero-Engines, Avionics and Flight Control, Cabin Interior and IFEC, and More), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Commercial Aircraft Market Trends and Insights

Fleet Replacement Cycle Accelerates Due to Aging Fleet and Efficiency Mandates

Airlines in North America are prioritizing newer-generation aircraft to reduce fuel burn and maintenance exposure as utilization normalizes and sustainability targets tighten. The replacement imperative is reinforced by extended delivery schedules that keep older fleets in service longer, which in turn sustain a parallel focus on reliability and cabin upgrades. At the same time, operators secure future slots for next-generation narrowbodies and selective widebodies. The Federal Aviation Administration (FAA) projects US mainline fleets to expand from 4,829 jets in 2024 to 6,854 by 2045, an average of 96 aircraft per year, reflecting both replacement and moderate growth that reshapes fleet age profiles over the long term. Carriers are locking in delivery positions well into the next decade, which turns procurement timing into a competitive lever in slot-constrained airports and high-demand leisure corridors. These orders are closely tied to operating economics, as new single-aisle platforms can materially lower unit costs relative to retiring families, supporting network flexibility and margin resilience in slower demand phases. The combined shift maintains pressure on supplier capacity, which underscores the importance of airspace modernization and certification throughput to convert orders into delivered lift over the forecast window.

Upgauging and Single-Aisle Dominance in Networks Driven by LCC Growth

Single-aisle aircraft continue to anchor network planning, as they combine favorable seat-mile costs with the gate compatibility carriers need at secondary airports. The trend extends beyond low-cost operators as legacy airlines standardize on higher-density narrowbody configurations for transcontinental and select transatlantic services, reinforcing the center of gravity in the North American commercial aircraft market. OEM production plans reflect this trajectory, as the A320 Family ramp targets higher monthly output in the late decade, while program backlogs anchor multi-year schedule visibility for airlines and lessors. Upgauging helps offset labor and airport constraints because larger single-aisle variants allow carriers to add seats without increasing movements at heavily utilized hubs. This strategy also supports route experimentation in long-thin markets, where new-generation narrowbodies can fly farther at improved economics, sustaining fleet commonality while broadening network reach. As a result, the narrowbody franchise remains the primary growth vector in the North America commercial aircraft market across the forecast period.

Engine Reliability and Inspection Cycles Disrupt Capacity and Deliveries

Inspection findings and mandated shop visits on selected engine families have tightened available lift and lengthened maintenance turn times across portions of the fleet. Airlines are mitigating through lease extensions and sub-fleet swaps, but that requires coordination with airport slots and crew availability, which limits how quickly grounded capacity can be offset. Lessors are also recalibrating terms as parked assets and late deliveries alter supply, which keeps lease rates firm relative to pre-pandemic baselines. Over the forecast period, faster parts flow and greater MRO throughput can reduce disruption. Still, in the short term, the North America commercial aircraft market faces localized groundings and operational buffers.

Other drivers and restraints analyzed in the detailed report include:

- US Passenger Traffic at Record Highs Sustaining Aircraft Demand

- North America Leads Global Freighter Fleet and New Widebody Freighter Deliveries

- Aerospace Supply-Chain Constraints Affecting Castings, Forgings, and Titanium Availability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Narrowbodies captured 79.73% of the North America commercial aircraft market share in 2025 and are forecast to post a 6.14% CAGR through 2031. Backlogs and production ramps for single-aisle aircraft indicate multi-year delivery visibility, supporting fleet commonality and network upgauging. Operators prioritize single-aisle aircraft for new capacity due to gate compatibility and turnaround advantages, while accommodating seasonality and peak demand. Elevated backlogs and tight production slots sustain residual values for in-service units, further driving procurement toward narrowbody aircraft.

Widebodies remain essential for long-haul networks and premium cabin revenue, though their growth rate is slower than that of narrowbodies. Cargo variants and conversions help stabilize utilization as older freighter lines retire. Regional jets continue to serve short-haul routes, but pilot scope and unit costs lead many operators to favor larger narrowbodies or modern turboprops. The procurement environment remains slot-driven, favoring carriers and lessors with early multi-year delivery agreements. This dynamic keeps the market focused on single-aisle programs while leveraging widebodies and regionals where economically viable.

Passenger operations held a 94.78% share in 2025 and are projected to grow at a 5.76% CAGR through 2031, ensuring that most of the North America commercial aircraft market remains tied to single-aisle fleet plans and premium-economy monetization. Traffic data show a tilt toward international leisure within seasonal peaks, which preserves widebody relevance while reinforcing the primacy of high-capacity narrowbodies on domestic and transborder routes. Airlines are allocating more cabin space to products that raise yield without significant weight penalties, which supports investments in connectivity and interiors at delivery to lock in lifetime ancillary revenue options.

Freighter applications continue to carry strategic weight that exceeds their revenue share suggests. The region's express and e-commerce ecosystems rely on dedicated aircraft to maintain next-day and two-day service standards, which underpins long-term forecasts for new-build freighters and conversions across the Americas. Airbus market materials also highlight new entrants in the widebody cargo space that will reach service later in the decade, complementing the conversion pipeline. Confirmed deliveries of B777-300ERSF units to North American operators signal deeper conversion capacity that can support payload-intensive missions during the production transition. Even amid mixed international cargo trends in 2025, the structural role of freighters helps balance seasonal swings in passenger flying, thereby steadying overall fleet utilization in the North America commercial aircraft market.

List of Companies Covered in this Report:

- Aircraft OEMs

- Systems Manufacturers and Integrators

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Fleet replacement cycle accelerates (aging fleet, efficiency mandates)

- 4.2.2 Upgauging and single-aisle dominance in networks and LCC growth

- 4.2.3 US passenger traffic at record highs sustaining aircraft demand

- 4.2.4 North America leads global freighter fleet and new widebody freighters

- 4.2.5 US SAF tax credits catalyze decarbonization investments

- 4.2.6 FAA NextGen capacity/efficiency gains support aircraft utilization

- 4.3 Market Restraints

- 4.3.1 Engine reliability/inspection cycles disrupt capacity and deliveries

- 4.3.2 Aerospace supply-chain constraints (castings/forgings/titanium)

- 4.3.3 Pilot and AMT pipeline constraints at regionals raise costs

- 4.3.4 Scope-clause ceilings limit new sub-100-seat jets adoption

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Aircraft Type

- 5.1.1 Narrowbody

- 5.1.2 Widebody

- 5.1.3 Regional Jets

- 5.2 By Application

- 5.2.1 Passenger

- 5.2.2 Freighter

- 5.3 By Propulsion Type

- 5.3.1 Turbofan

- 5.3.2 Turboprop

- 5.4 By Component

- 5.4.1 Airframe Structures

- 5.4.2 Aero-Engines

- 5.4.3 Avionics and Flight Control

- 5.4.4 Cabin Interior and IFEC

- 5.4.5 Other Components

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share Analysis

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Aircraft OEMs

- 6.3.1.1 Airbus SE

- 6.3.1.2 The Boeing Company

- 6.3.1.3 Embraer S.A.

- 6.3.1.4 Avions de Transport Regional GIE (ATR)

- 6.3.1.5 Commercial Aircraft Corporation of China, Ltd. (COMAC)

- 6.3.1.6 De Havilland Aircraft of Canada Limited

- 6.3.1.7 United Aircraft Corporation

- 6.3.1.8 Mitsubishi Heavy Industries, Ltd.

- 6.3.2 Systems Manufacturers and Integrators

- 6.3.2.1 Safran S.A.

- 6.3.2.2 Honeywell International Inc.

- 6.3.2.3 Rolls-Royce Holdings plc

- 6.3.2.4 General Electric Company

- 6.3.2.5 RTX Corporation

- 6.3.2.6 MTU Aero Engines AG

- 6.3.2.7 BAE Systems plc

- 6.3.2.8 Teledyne Technologies Incorporated

- 6.3.2.9 Thales Group

- 6.3.1 Aircraft OEMs

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment