PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066703

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066703

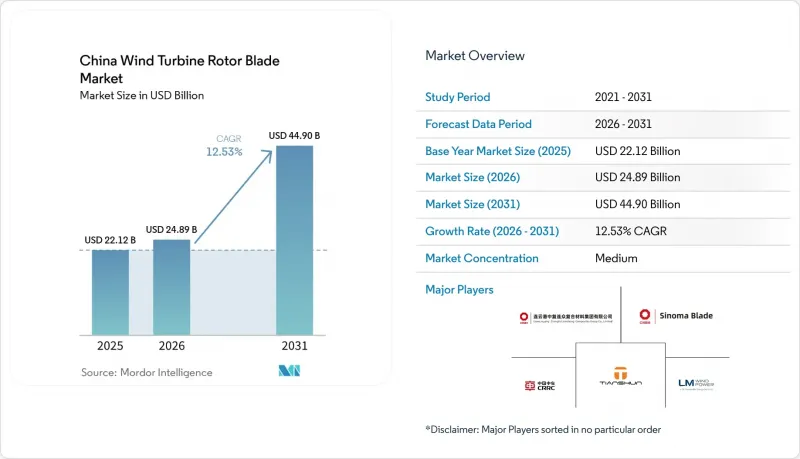

China Wind Turbine Rotor Blade - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the china wind turbine rotor blade market size was valued at USD 22.12 billion in 2025 and estimated to grow from USD 24.89 billion in 2026 to reach USD 44.9 billion by 2031, at a CAGR of 12.53% during the forecast period (2026-2031).

This report is Segmented by Location of Deployment (Onshore and Offshore), Blade Material (Carbon Fiber, Glass Fiber, Hybrid Composites, and Other Blade Materials), Blade Length (Below 45 M, 46 To 60 M, 61 To 75 M, and Above 75 M), and Manufacturing Process (Hand Lay-Up, Vacuum Infusion, Pre-Preg, and Others). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

China Wind Turbine Rotor Blade Market Trends and Insights

Ambitious 2030 Wind-Power Capacity Targets

China plans to hit 400 GW of cumulative wind by 2030, with 140 GW slated for 2025 alone. This policy certainty drives the long-term procurement of ever-larger rotors, 58.6% of which now exceed 180 m in diameter. Grid-parity objectives force OEMs to optimize blade aerodynamics for diverse inland and coastal conditions. Consistent government backing sustains capital inflows into new blade factories, sparking technology upgrades that keep the Chinese wind turbine rotor blade market on a steep growth curve.

Cost Decline in > 80 m Carbon-Glass Hybrid Blades

Hybrid composites reduce blade weight by 38% and costs by 14% compared to glass-only designs, while maintaining stiffness. Automated fiber placement and thermoplastic processing now enable serial manufacture, anchoring China's leadership in blades exceeding 80 m in length for offshore use. Local suppliers of polyurethane resin systems are strengthening hybrid adoption, pushing the China wind turbine rotor blade market toward lightweight, high-performance solutions suited for 16 MW-class turbines.

Volatile Epoxy & PET Foam Prices Squeezing Margins

Shift from scarce balsa to PET foam magnifies exposure to petrochemical swings; resin spikes already compress OEM margins by up to 3 percentage points. Currency shifts and import tariffs complicate budgeting, compelling supply-chain diversification and trials of bioplastics, also known as bio-resins. Price pass-through is limited amid cut-throat turbine bidding, keeping profitability pressure high across the Chinese wind turbine rotor blade market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Offshore Wind Build-Out Along Coastal Provinces

- Accelerating Replacement of 2010-Era Onshore Turbines

- Grid Curtailment Risk in Northern China Wind Bases

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Onshore blades contribute 92.12% of 2025 installations and are projected to log a 13.05% CAGR to 2031, driven by large-scale repowering that rapidly expands the China wind turbine rotor blade market size for this segment. Fleet owners in Inner Mongolia and Xinjiang swap out sub-2 MW units for modern 5 MW designs that increase site yields by more than 70%

Latest province-level auctions include strict LCOE caps, prompting OEMs to opt for longer rotors to maximize megawatt-hours within fixed tariffs. Enhanced aerodynamics and hybrid materials keep nacelle mass in check, ensuring logistics feasibility across rugged inland transport routes. The result is a virtuous cycle of capacity factor gains and declining costs that entrenches onshore leadership in the Chinese wind turbine rotor blade market.

Offshore arrays, though smaller today, represent the fastest-growing slice, adding more than 10 GW annually after 2025. Jiangsu's deep-sea sites pioneered 240-m rotor trials in 2025, signalling future procurement of extra-long, splash-zone-resistant blades. Floating foundations under test in Fujian could unlock Southern deep-water zones, expanding geographical diversity and boosting the overall China wind turbine rotor blade market.

Carbon fiber's 50.72% share stems from its stiffness-to-weight edge, especially for > 10 MW offshore machines. Yet, hybrids will see a 13.28% CAGR to 2031 and could overtake carbon by volume before 2032, reshaping the China wind turbine rotor blade market share landscape.

Producers blend carbon unis with glass fabrics, lowering cost while retaining critical bending stiffness. Thermoplastic resins make large-part recycling feasible, aligning with China's 2030 circular-economy standards. Hybrids thus bridge the cost and sustainability gap, widening the addressable demand and anchoring market expansion.

List of Companies Covered in this Report:

- Lianyungang Zhongfu Lianzhong Composites Group Co. Ltd

- Sinoma Wind Power Blade Co. Ltd

- Zhuzhou Times New Material Technology Co. Ltd

- Tianshun Wind Energy (Suzhou) Co. Ltd

- LM Wind Power (GE Renewable Energy)

- TPI Composites Inc. (China)

- Nordex SE (Jiangsu Facility)

- Vestas Wind Systems A/S (Tianjin)

- Siemens Gamesa Renewable Energy (Tianjin)

- Goldwind Science & Technology Co. Ltd

- Dongfang Electric Wind Blade Co. Ltd

- Shanghai Aeolon Wind Energy Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ambitious 2030 wind-power capacity targets

- 4.2.2 Cost decline in >80 m carbon-glass hybrid blades

- 4.2.3 Rapid offshore wind build-out along coastal provinces

- 4.2.4 Accelerating replacement of 2010-era onshore turbines

- 4.2.5 Commercialisation of pultrusion-based automated blade lines

- 4.2.6 Digital-twin enabled life-extension & warranty models

- 4.3 Market Restraints

- 4.3.1 Volatile epoxy & PET foam prices squeezing margins

- 4.3.2 Grid curtailment risk in Northern China wind bases

- 4.3.3 Stricter land-use & ecological approvals for new projects

- 4.3.4 Shortage of skilled composites technicians

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 By Blade Material

- 5.2.1 Glass Fiber

- 5.2.2 Carbon Fiber

- 5.2.3 Hybrid Composites

- 5.2.4 Others

- 5.3 By Blade Length

- 5.3.1 Below 45 m

- 5.3.2 46 to 60 m

- 5.3.3 61 to 75 m

- 5.3.4 Above 75 m

- 5.4 By Manufacturing Process

- 5.4.1 Hand Lay-Up

- 5.4.2 Vacuum Infusion

- 5.4.3 Pre-Preg

- 5.4.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Lianyungang Zhongfu Lianzhong Composites Group Co. Ltd

- 6.4.2 Sinoma Wind Power Blade Co. Ltd

- 6.4.3 Zhuzhou Times New Material Technology Co. Ltd

- 6.4.4 Tianshun Wind Energy (Suzhou) Co. Ltd

- 6.4.5 LM Wind Power (GE Renewable Energy)

- 6.4.6 TPI Composites Inc. (China)

- 6.4.7 Nordex SE (Jiangsu Facility)

- 6.4.8 Vestas Wind Systems A/S (Tianjin)

- 6.4.9 Siemens Gamesa Renewable Energy (Tianjin)

- 6.4.10 Goldwind Science & Technology Co. Ltd

- 6.4.11 Dongfang Electric Wind Blade Co. Ltd

- 6.4.12 Shanghai Aeolon Wind Energy Technology

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment