PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066704

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066704

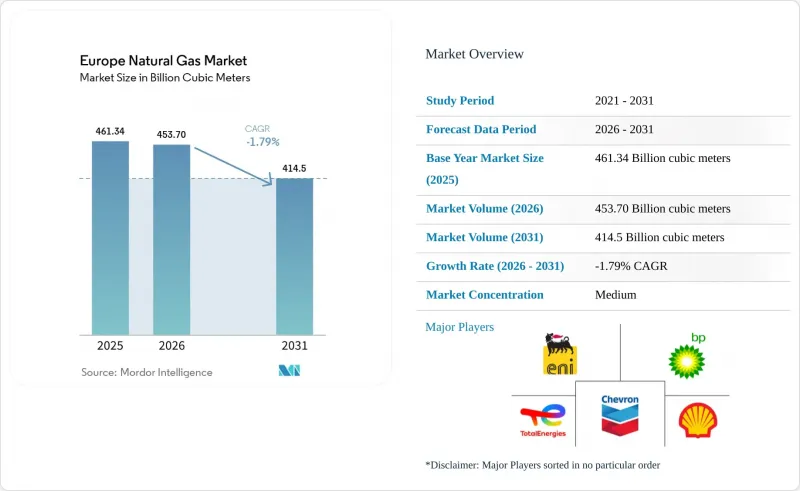

Europe Natural Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe natural gas market size is projected to contract from 461.34 Billion cubic meters in 2025 and 453.70 Billion cubic meters in 2026 to 414.5 Billion cubic meters by 2031, registering a CAGR of -1.79% between 2026 to 2031.

This report is Segmented by Type (Compressed Natural Gas, Piped Natural Gas, and Liquefied Natural Gas), Source (Domestic Production - Onshore, Domestic Production - Offshore, and LNG Imports), End-Use Sector (Fertilizer Production, City Gas Distribution, Transportation, Petrochemical Feedstock, and Others), and Geography (Germany, France, Italy, Spain, Netherlands, Norway, Poland, and Rest of Europe).

Europe Natural Gas Market Trends and Insights

Coal-to-Gas Switching in Power & District Heating Fleets

Municipal operators in Germany and Poland continue migrating from aging coal boilers to gas-fired combined heat and power units as carbon-allowance prices climbed to EUR 83.79 per tonne CO2 in December 2025 and are heading toward EUR 149 by 2030. Mid-sized cities favor incremental gas conversions because district-heating grids often lack capacity for large-scale heat pumps. The opportunity window, however, is narrowing as Title Transfer Facility (TTF) prices occasionally exceed coal-switching thresholds, reducing baseload gas economics. While gas-fired electricity output slipped 6% in 2024, near-term compliance deadlines under the Energy Efficiency Directive still support residual switching in heating. As grid upgrades and renewables proliferate, district-heating gas demand is expected to plateau after 2029, reinforcing the European natural gas market's structural decline even as short-term gains persist.

Expansion of European LNG Regasification Capacity

Europe's regasification capacity jumped 32% between 2022 and 2025 to roughly 270 BCM per year, propelled by rapid FSRU deployments in Germany and expansions in Poland and the Netherlands. Germany alone commissioned 44.8 BCM of import capacity across Wilhelmshaven, Brunsbuttel, Lubmin, and Stade within 24 months. Poland's Gdansk FSRU and Swinoujscie upgrade now provide 14.4 BCM combined, giving Warsaw surplus volumes for regional exports. Lithuania's Klaipeda terminal underscores the rise of small-scale reloads, posting 1,834 truck loadings in 2025. Forecast additions could lift capacity to 405 BCM by 2030, implying significant over-build if demand trends hold, so asset owners increasingly seek long-term offtake partners to mitigate utilization risk.

Geopolitical Supply Disruptions After Russia-Ukraine War

Russian pipeline flows plunged from about 40% of EU supply in 2021 to 13% in 2025 as sanctions and the transit-agreement expiry forced diversification. The European Commission now seeks a full Russian-gas ban by the end of 2027, funneling demand to LNG spot markets and Norwegian pipelines. Norway supplied 31% of EU needs in 2025, yet flat output limits future upside. Inventory dipped to 40% in February 2025, below the 50% regulatory minimum, sparking price spikes and industrial curtailments. Utilities remain hesitant to sign 20-year LNG deals at elevated prices, prolonging supply-risk premiums and deterring new liquefaction investments.

Other drivers and restraints analyzed in the detailed report include:

- Policy Support for Gas as a Transition Fuel Under Fit-for-55

- Growth of Small-Scale LNG Bunkering Infrastructure in Baltic & North Seas

- EU 2040 Decarbonization Target Accelerating Electrification

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Piped natural gas retained 70.7% of the Europe natural gas market share in 2025, reflecting decades of network build-out that offers low tariffs of EUR 2-4 per MWh. Pipeline volumes, however, decline as legacy Russian contracts expire and residential electrification widens, shrinking the European natural gas market size allocated to PNG. LNG, although costlier at EUR 6-8 per MWh delivered, is forecast to expand 3.5% annually through 2031 thanks to new FSRUs and flexible spot-purchase options.

LNG's adaptability makes it the favored marginal source for utilities balancing volatile renewables. Small-scale LNG also supports trucking and marine bunkering, reinforcing downstream growth. Compressed natural gas remains niche, with 786 refueling stations mainly in Italy, France, and Germany. Competing drivetrain technologies restrict CNG's headroom, and total demand is set to plateau late in the decade. Overall, LNG's expansion partially cushions pipeline-volume erosion, slowing, but not reversing, the European natural gas market's aggregate decline.

List of Companies Covered in this Report:

- Shell plc

- BP plc

- TotalEnergies SE

- Equinor ASA

- Eni SpA

- Exxon Mobil Corp.

- Chevron Corp.

- ConocoPhillips

- Engie SA

- EDF SA

- Gazprom PJSC

- OMV AG

- Repsol SA

- PGNiG (PKN Orlen)

- Naturgy Energy Group SA

- VNG AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Coal-to-gas switching in power & district-heating fleets

- 4.2.2 Expansion of European LNG regasification capacity

- 4.2.3 Policy support for gas as a transition fuel under Fit-for-55

- 4.2.4 Growth of small-scale LNG bunkering infrastructure in Baltic & North Seas

- 4.2.5 Hydrogen-ready pipeline retrofits lowering stranded-asset risk

- 4.3 Market Restraints

- 4.3.1 Geopolitical supply disruptions after Russia-Ukraine war

- 4.3.2 EU 2040 decarbonisation target accelerating electrification

- 4.3.3 Mandatory biomethane blending quotas reducing fossil-gas demand

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Compressed Natural Gas (CNG)

- 5.1.2 Piped Natural Gas (PNG)

- 5.1.3 Liquefied Natural Gas (LNG)

- 5.2 By Source

- 5.2.1 Domestic Production - Onshore

- 5.2.2 Domestic Production - Offshore

- 5.2.3 LNG Imports

- 5.3 By End-Use Sector

- 5.3.1 Fertilizer Production

- 5.3.2 City Gas Distribution

- 5.3.3 Transportation

- 5.3.4 Petrochemical Feedstock

- 5.3.5 Others [Industrial Manufacturing, Agriculture (Tea Plantation), IC for Pipeline System, LPG Shrinkage, Sponge Iron/Steel]

- 5.4 By Geography

- 5.4.1 Germany

- 5.4.2 France

- 5.4.3 Italy

- 5.4.4 Spain

- 5.4.5 Netherlands

- 5.4.6 Norway

- 5.4.7 Poland

- 5.4.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Shell plc

- 6.4.2 BP plc

- 6.4.3 TotalEnergies SE

- 6.4.4 Equinor ASA

- 6.4.5 Eni SpA

- 6.4.6 Exxon Mobil Corp.

- 6.4.7 Chevron Corp.

- 6.4.8 ConocoPhillips

- 6.4.9 Engie SA

- 6.4.10 EDF SA

- 6.4.11 Gazprom PJSC

- 6.4.12 OMV AG

- 6.4.13 Repsol SA

- 6.4.14 PGNiG (PKN Orlen)

- 6.4.15 Naturgy Energy Group SA

- 6.4.16 VNG AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment