PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066719

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066719

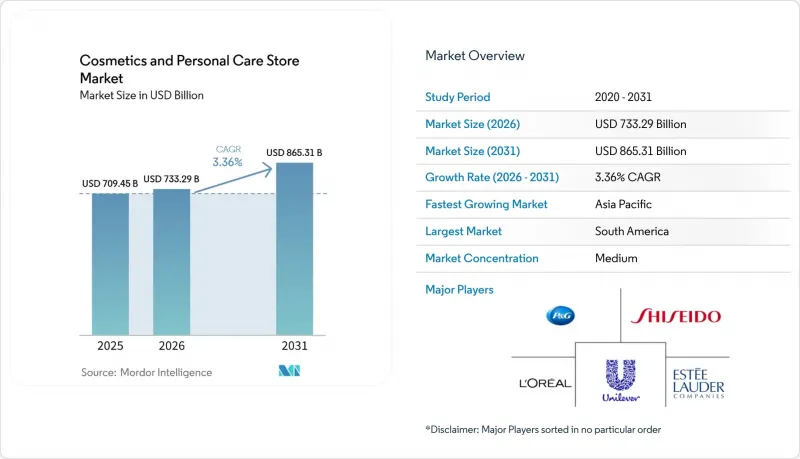

Cosmetics And Personal Care Store - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the cosmetics and personal care store market size is expected to grow from USD 709.45 billion in 2025 to USD 733.29 billion in 2026 and is forecast to reach USD 865.31 billion by 2031 at 3.36% CAGR over 2026-2031.

This report is Segmented by Product Type (Decorative, Skincare, Haircare, Perfume, Oral-Care, Bath & Shower), Distribution Channel (Specialist Retail Stores, and Other), Store Format (Flagship Beauty Stores, and Other), and Geography (North America, South America, Europe, Asia-Pacific, Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD), Based On Availability.

Global Cosmetics And Personal Care Store Market Trends and Insights

Rising Disposable Income in Emerging Markets

Middle-class expansion in Asia-Pacific and South America translates to higher per-capita spending on prestige beauty, with Watsons allocating USD 250 million to refurbish 6,000 regional outlets to experiential formats. L'Oreal treats Brazil as an "open-air laboratory," using rapid test-and-learn rollouts to localize products and formats quickly. International brands capitalize on relatively streamlined approval cycles and supportive foreign-investment policies, enabling quicker shelf placement than in mature Western markets. Premiumization is further encouraged by social-media narratives that frame beauty as a marker of self-expression and success. Domestic retailers respond by layering concierge-style services and in-store diagnostics to boost conversion. Currency stabilization in several key markets improves imported product affordability, reinforcing demand for luxury SKUs. Overall, rising purchasing power remains a pivotal tailwind for the cosmetics and personal care store market revenue growth.

Growing Demand for Natural/Organic Cosmetics

Regulators and consumers alike scrutinize ingredient safety, driving retailers to expand clean-beauty assortments and initiate refill or recycling programs. Sephora has broadened its in-store refill stations, while The Body Shop extended its global refill initiative to more than 720 locations in 2024. Transparency mandates under MoCRA and the EU Green Deal raise the bar for documentation, nudging formulators toward plant-derived actives and biodegradable packaging. Specialty retailers position curated organic lines and third-party certifications as differentiators against mass competitors. Price premiums remain resilient because shoppers equate verified natural claims with health benefits and environmental responsibility. These dynamics foster margin-accretive product mixes for retailers able to secure stable, ethically sourced supply chains.

High Dependence on Discretionary Spending Cycles

Beauty remains a non-essential category, so economic slowdowns quickly translate into traffic declines and lower average tickets. Bath & Body Works and other mid-tier chains reported softer footfall during inflationary spikes in 2024, prompting heavier promotion calendars. Ulta registered a 1.2% comp-store drop in Q2 2024, forcing management to trim full-year guidance despite later rebounds. North and South American markets exhibit heightened sensitivity because consumer-confidence indices closely correlate with beauty expenditures. Retailers shelter margins by ramping up own-label ranges, offering bundle deals, and leveraging loyalty points to encourage repeat visits. Credit-card delinquency upticks in some regions signal potential further tightening of discretionary spending. The constraint underscores the importance of diversified geographic footprints and balanced channel mixes for retailers seeking steady cosmetics and personal care store market growth.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Specialty Beauty Retail Chains

- Omnichannel Retail Integration in Beauty Sector

- Rising Competition from Direct-to-Consumer E-Commerce

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Skincare held 31.88% of the cosmetics and personal care store market share in 2025 on the strength of science-backed formulations and AI-enabled skin analyses that personalize regimens. Multinationals employ large R&D teams to launch serums, essences, and targeted dermo cosmetic lines that command premium pricing. Younger consumers gravitate toward preventative skin health, sustaining demand for SPF and barrier-repair products. Regulatory scrutiny surrounding ingredients such as parabens and PFAS encourages reformulation and cleaner label positioning in both mass and prestige tiers. Haircare, however, leads future growth at a 8.87% CAGR as scalp-health products and bond-repair treatments ride the "skinification" wave. Clinics and salons integrate diagnostic devices that migrate into retail, translating professional protocols into at-home regimens that lift average unit prices. Retailers dedicate expanded shelf space to trichology-inspired lines, diversifying the cosmetics and personal care store market size across categories.

Skincare's maturity constrains incremental volume gains, so brands focus on adjacent sub-segments such as skin-microbiome boosters and blue-light protection sprays. In contrast, haircare benefits from under-penetration of premium price points in emerging markets, signaling ample runway for value-per-capita growth. Cross-category bundles pairing facial serums with scalp tonics encourage multi-item baskets and deepen loyalty-program engagement. Ingredient transparency regulations elevate switching costs by making consumers more discerning, thereby reinforcing brand equity for compliant players. At the same time, indie labels use plant-based actives to resonate with clean-beauty enthusiasts, nudging incumbents to accelerate green chemistry roadmaps. Collectively, product-mix shifts and premiumization efforts sustain cosmetics and personal care store market size expansion across both established and nascent categories.

Geography Analysis

Asia-Pacific retained 37.40% of the cosmetics and personal care store market share in 2025, supported by Watsons' USD 250 million overhaul of 6,000 stores across 15 markets and Mecca's regional expansion. Rising disposable income, social-commerce influence, and government policies encouraging foreign direct investment sustain demand for both mass and prestige offerings. Flagship and concept-store counts proliferate in tier-one and tier-two cities where consumer appetite for experiential shopping is strongest. Regulatory frameworks remain supportive, with streamlined licensing in markets such as Thailand and Indonesia accelerating rollout timelines. South America tops the growth chart at a 8.89% CAGR, underpinned by Brazil's fragrance boom and L'Oreal's "open-air laboratory" strategy that tests localized SKUs before global release. Mexico attracts attention after Ulta partnered with Grupo Axo to build a multi-store network, broadening prestige accessibility. Economic reforms and expanding middle-class cohorts boost premium-segment volume, albeit currency fluctuations pose earnings-translation risks. Local champions like Natura leverage hybrid offline-online ecosystems to fend off international competition.

North America and Europe collectively exceed 30% of the cosmetics and personal care store market size, but display maturity. The Ulta-Sephora rivalry intensifies as both chains advance omnichannel investments and expand loyalty memberships past 40 million each. Europe grapples with cost pressures stemming from proposed EU ban extensions on PFAS and expanded safety-testing obligations, raising barriers for indie entrants. Nevertheless, refurbished department-store halls and AI-powered diagnostics refresh consumer interest. The Middle East & Africa and Oceania emerge as frontier opportunities. Printemps plans a New York flagship as a springboard for Gulf expansions, while brands such as La Mer invest in Southeast Asian flagships to capture luxury tourism flows. Diverse regulatory regimes require agile compliance capabilities, yet lower saturation levels create white-space potential. Collectively, geographic diversification mitigates macro volatility and unlocks incremental cosmetics personal care store market growth.

- L'Oreal Group

- Estee Lauder Companies

- Procter & Gamble

- Unilever

- Shiseido

- Coty Inc.

- LVMH Moet Hennessy Louis Vuitton

- Johnson & Johnson

- Beiersdorf AG

- Amorepacific Corp.

- Revlon Inc.

- Kao Corporation

- Natura &Co

- Mary Kay

- Oriflame

- Kylie Cosmetics

- Glossier

- The Hut Group (THG Beauty)

- Sephora (Retailer)

- Ulta Beauty (Retailer)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising disposable income in emerging markets

- 4.2.2 Growing demand for natural/organic cosmetics

- 4.2.3 Proliferation of specialty beauty retail chains

- 4.2.4 Omnichannel retail integration in beauty sector

- 4.2.5 Experiential in-store tech (AR mirrors, diagnostics)

- 4.2.6 Subscription-based refill & zero-waste stations

- 4.3 Market Restraints

- 4.3.1 High dependence on discretionary spending cycles

- 4.3.2 Stringent cosmetic safety & labeling regulations

- 4.3.3 Rising competition from direct-to-consumer e-commerce

- 4.3.4 Land-use restrictions limiting new brick-and-mortar sites

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Decorative

- 5.1.2 Skincare

- 5.1.3 Haircare

- 5.1.4 Perfume

- 5.1.5 Oral-Care

- 5.1.6 Bath & Shower

- 5.2 By Distribution Channel

- 5.2.1 Specialist Retail Stores

- 5.2.2 Supermarket / Hypermarket

- 5.2.3 Convenience Stores

- 5.2.4 Pharmacies / Drug Stores

- 5.3 By Store Format

- 5.3.1 Flagship Beauty Stores

- 5.3.2 Department Store Beauty Halls

- 5.3.3 Pop-Up / Kiosk Stores

- 5.3.4 Omni-channel Concept Stores

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East & Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East & Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 L'Oreal Group

- 6.4.2 Estee Lauder Companies

- 6.4.3 Procter & Gamble

- 6.4.4 Unilever

- 6.4.5 Shiseido

- 6.4.6 Coty Inc.

- 6.4.7 LVMH Moet Hennessy Louis Vuitton

- 6.4.8 Johnson & Johnson

- 6.4.9 Beiersdorf AG

- 6.4.10 Amorepacific Corp.

- 6.4.11 Revlon Inc.

- 6.4.12 Kao Corporation

- 6.4.13 Natura &Co

- 6.4.14 Mary Kay

- 6.4.15 Oriflame

- 6.4.16 Kylie Cosmetics

- 6.4.17 Glossier

- 6.4.18 The Hut Group (THG Beauty)

- 6.4.19 Sephora (Retailer)

- 6.4.20 Ulta Beauty (Retailer)

7 Market Opportunities & Future Outlook

- 7.1 Premium zero-waste refill store concepts

- 7.2 AI-driven personalized in-store regimen mapping