PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066722

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066722

North America Home Energy Management System (HEMS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

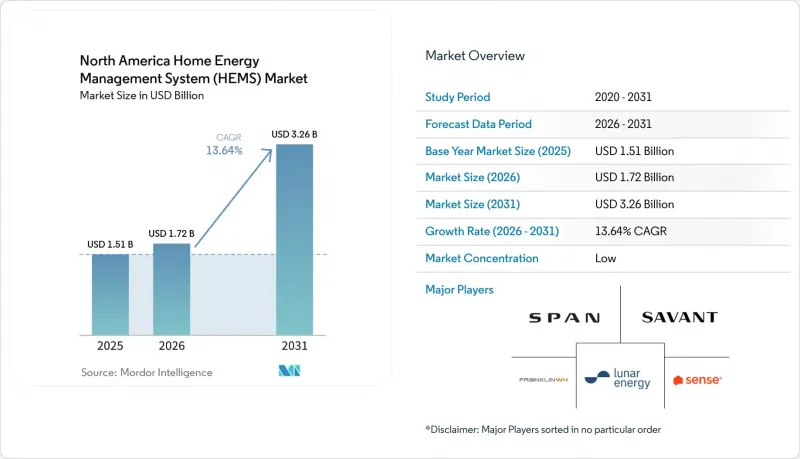

According to Mordor Intelligence, the north america home energy management system (HEMS) market size is expected to grow from USD 1.51 billion in 2025 to USD 1.72 billion in 2026 and is forecast to reach USD 3.26 billion by 2031 at 13.64% CAGR over 2026-2031.

This report is Segmented by Component (Hardware (Smart Meters, Smart Thermostats, Energy Storage Systems, and More), Software, Services), Communication Technology (ZigBee, Wi-Fi, Z-Wave, and More), End-User (Residential, Commercial), Deployment Mode (Cloud-Hosted Platforms, On-Premises / Local Gateway), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America Home Energy Management System (HEMS) Market Trends and Insights

Smart Meter and AMI Saturation Supporting Real-Time Control

Smart meter saturation is pushing household energy management away from simple usage visibility and toward real-time device control. In the North America home energy management system (HEMS) market, this matters because AMI data gives platforms a constant stream of household consumption signals that can support automated scheduling, load disaggregation, and tariff response. As utilities move from billing-focused infrastructure to grid-edge intelligence, the value of software that can interpret meter data and translate it into appliance-level decisions rises with it. This shift also lowers the friction of adoption because some households can receive better energy insight without adding a full set of new sensing hardware inside the home. The North America home energy management system market benefits from that lower entry barrier because it expands the addressable base for platform vendors and utility-led programs. It also strengthens the case for partnerships between utilities, software developers, and device providers that can turn existing grid infrastructure into a practical household orchestration layer.

Solar-Plus-Storage and Home Electrification Adoption

Solar-plus-storage adoption is one of the clearest demand anchors for the North America home energy management system market because households with multiple energy assets need active coordination rather than passive monitoring. The US residential storage segment grew 51% year over year in 2025, and cumulative deployments since 2019 exceeded 50GW and 144GWh, which materially expanded the installed base that can be paired with household energy control software. The same report indicates the United States is expected to deploy 500GWh of storage from 2026 to 2031, which keeps creating new integration points for home energy platforms over the forecast period. In practical terms, each new battery system raises the value of software that can optimize charging, backup priority, self-consumption, and time-based load shifting inside the home. This is why the North America home energy management system (HEMS) market is moving closer to full-stack orchestration, where thermostats, smart panels, storage systems, and connected loads operate as one coordinated energy system. The adoption of electric appliances and home electrification upgrades further deepens this need because household power flows become more complex as more flexible loads enter the home.

High Upfront System and Installation Costs

High upfront system cost remains the clearest barrier to mass adoption in the North America home energy management system market. A fully integrated residential setup that includes a smart panel, battery storage, thermostat, software, and EV charging can require USD 15,000 to USD 35,000 before rebates, which keeps many middle-income households on the sidelines. Installation also adds cost because circuit-level control and electrical reconfiguration often require trained electricians and platform-specific commissioning. This cost issue is more severe in multi-family settings and in markets where rebate rollout is slower or utility support is limited. It also affects product mix because households may choose a thermostat or a solar-only setup first, then delay the rest of the energy stack until financing or rebates improve. Until service-based financing and lower-cost deployment models scale more broadly, the North America HEMS market will continue to face slower conversion from consumer interest to completed installations.

Other drivers and restraints analyzed in the detailed report include:

- Utility Time-Of-Use and Dynamic Pricing Expansion

- IRA-Linked Whole-Home Rebate Stacking Improving HEMS Payback

- Cybersecurity and Household Data Privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware held 64.56% of the North America home energy management system market share in 2025, which reflects the still heavy role of physical equipment in total system spending. Smart thermostats remain the most common first step because they offer a visible path to energy savings and can connect later to a broader household control stack. The North America home energy management system market also continues to rely on smart electrical panels, energy storage systems, smart plugs, and in-home displays to create the physical control and sensing layer required for coordinated energy management. Rising US residential electricity prices in 2025 reinforced the need for hardware-led demand control, especially for households looking to manage peak usage more actively. SPAN strengthened that hardware case in February 2025 when it launched the SPAN Panel MAIN 40+MID and SPAN Panel MLO 48 with 25-50% more breaker spaces, while also positioning the products around avoiding 400-ampere service upgrade costs in all-electric homes.

Software is the fastest-growing component in the North America home energy management system (HEMS) market, with a 14.89% CAGR expected from 2026 to 2031. That expansion reflects the move toward AI-based load forecasting, tariff optimization, battery dispatch logic, and recurring platform subscriptions rather than one-time device revenue. The North America home energy management system market size for software is gaining support from the rising installed base of residential storage, which creates a larger pool of homes that need real-time orchestration across generation, storage, and flexible loads. Enphase reinforced this direction in February 2026 when it introduced Power Control software for IQ9 and IQ8 microinverter-based small commercial systems, showing how software can improve economics on top of an existing hardware base. Services are also expanding because multi-vendor integration, commissioning, monitoring, and managed participation in utility programs require specialized support as the installed asset base becomes more complex.

Wi-Fi accounted for 38.76% of revenue in 2025 and remained the largest communication layer in the North America home energy management system market because it fits naturally into existing home broadband networks. It supports cloud-connected dashboards, remote configuration, software updates, and high-bandwidth data exchange without requiring a separate communication backbone in most homes. ZigBee continues to matter in utility-linked and meter-adjacent environments because low-power mesh communication still suits large distributed device deployments. Bluetooth maintains relevance for short-range setup and control, especially in simpler outlet-level or portable device configurations. HomePlug still serves certain retrofit cases where wiring conditions or building materials reduce the reliability of wireless links inside older homes.

Z-Wave is the fastest-growing communication protocol, with a 14.21% CAGR projected for 2026 to 2031, and it benefits from strong performance in battery-powered, multi-sensor environments. The Connectivity Standards Alliance released Matter 1.5 in November 2025, and the update added an Electrical Energy Tariff device type along with broader support that helps devices share pricing and energy data more consistently across protocols. That matters for the North America home energy management system market because interoperability reduces the risk that any one household must choose a single closed communication stack. It also allows a practical coexistence model where Wi-Fi handles high-bandwidth cloud tasks while Z-Wave supports low-power sensing and control at the edge. Matter 1.5.1, released in March 2026, further improved cross-platform device behavior and reinforced the push toward smoother multi-device compatibility.

List of Companies Covered in this Report:

- SPAN.io, Inc.

- Savant Systems, Inc.

- FranklinWH Energy Storage Inc.

- Lunar Energy, Inc.

- Sense Labs, Inc.

- Emporia Corp

- Lumin Systems, Inc.

- ecobee Inc.

- sonnen GmbH

- Resideo Technologies, Inc.

- Itron, Inc.

- Generac Holdings, Inc.

- ChargePoint Holdings, Inc.

- Sigenergy Technology Co., Ltd.

- EcoFlow Technology Inc.

- Anker Innovations Technology Co., Ltd.

- Enphase Energy, Inc.

- SolarEdge Technologies, Inc.

- AutoGrid, Inc.

- OhmConnect, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smart Meter and AMI Saturation Supporting Real-Time Control

- 4.2.2 Utility Time-of-Use and Dynamic Pricing Expansion

- 4.2.3 Solar-Plus-Storage and Home Electrification Adoption

- 4.2.4 Insurance and Resiliency Demand for Backup-Oriented Energy Orchestration

- 4.2.5 IRA-Linked Whole-Home Rebate Stacking Improving HEMS Payback

- 4.2.6 Matter 1.5 and Utility Signal Standardization Lowering Integration Friction

- 4.3 Market Restraints

- 4.3.1 High Upfront System and Installation Costs

- 4.3.2 Cybersecurity and Household Data Privacy Concerns

- 4.3.3 Installer Commissioning Complexity Across Multi-Vendor Home Energy Assets

- 4.3.4 Tariff and Program Volatility Weakening Consumer ROI Confidence

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Smart Meters

- 5.1.1.2 Smart Thermostats

- 5.1.1.3 Energy Storage Systems

- 5.1.1.4 Smart Plugs and Outlets

- 5.1.1.5 In-Home Displays (IHDs)

- 5.1.1.6 Other Hardwares

- 5.1.2 Software

- 5.1.3 Services

- 5.1.1 Hardware

- 5.2 By Communication Technology

- 5.2.1 ZigBee

- 5.2.2 Wi-Fi

- 5.2.3 Z-Wave

- 5.2.4 Bluetooth

- 5.2.5 HomePlug

- 5.2.6 Other Communication Technologies

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.1.1 Single-Family Homes

- 5.3.1.2 Multi-Family Housing

- 5.3.2 Commercial

- 5.3.2.1 Small Office / Home Office

- 5.3.2.2 Retail and Hospitality

- 5.3.1 Residential

- 5.4 By Deployment Mode

- 5.4.1 Cloud-Hosted Platforms

- 5.4.2 On-Premises / Local Gateway

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SPAN.io, Inc.

- 6.4.2 Savant Systems, Inc.

- 6.4.3 FranklinWH Energy Storage Inc.

- 6.4.4 Lunar Energy, Inc.

- 6.4.5 Sense Labs, Inc.

- 6.4.6 Emporia Corp

- 6.4.7 Lumin Systems, Inc.

- 6.4.8 ecobee Inc.

- 6.4.9 sonnen GmbH

- 6.4.10 Resideo Technologies, Inc.

- 6.4.11 Itron, Inc.

- 6.4.12 Generac Holdings, Inc.

- 6.4.13 ChargePoint Holdings, Inc.

- 6.4.14 Sigenergy Technology Co., Ltd.

- 6.4.15 EcoFlow Technology Inc.

- 6.4.16 Anker Innovations Technology Co., Ltd.

- 6.4.17 Enphase Energy, Inc.

- 6.4.18 SolarEdge Technologies, Inc.

- 6.4.19 AutoGrid, Inc.

- 6.4.20 OhmConnect, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment