PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066733

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066733

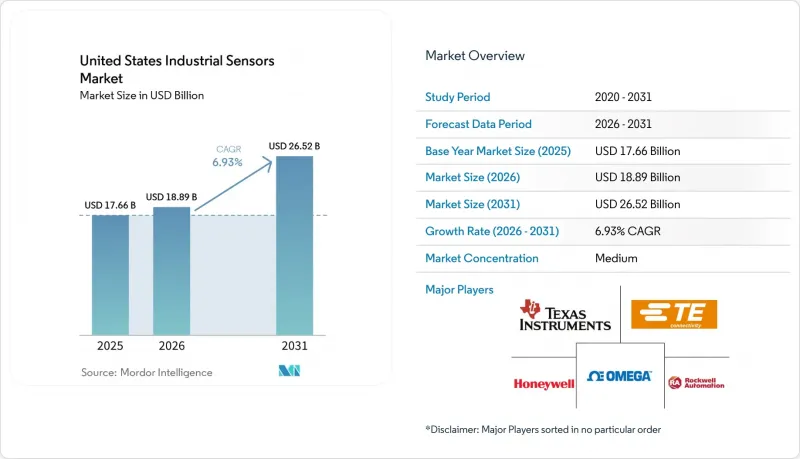

United States Industrial Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states industrial sensors market size was valued at USD 17.66 billion in 2025 and is estimated to grow from USD 18.89 billion in 2026 to USD 26.52 billion by 2031, growing at a CAGR of 6.93% from 2026 to 2031.

This report is Segmented by Connectivity (Wired Solutions, and Wireless Solutions), Sensor Type (Pressure Sensors, Flow Sensors, Temperature Sensors, Level Sensors, and More), and End-User Industry (Oil and Gas, Chemicals and Petrochemicals, Water and Wastewater, Food and Beverage, Power Generation, Automotive, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Industrial Sensors Market Trends and Insights

Surge in IIoT Adoption Across Discrete and Process Industries

Manufacturers are embedding sensors at every production node to enable real-time analytics that minimize unplanned downtime and scrap rates. Private 5G deployments demonstrate sub-10 millisecond latency for vibration, temperature, and vision sensors, validating wireless performance on automotive assembly and CNC machining lines. Food processors have reduced cabling work by 60% using LoRaWAN gateways to backhaul data from hygienic temperature and flow sensors. Edge gateways now run time-sensitive networking in concert with OPC UA, allowing closed-loop control that was previously limited to wired systems. As a result, the United States industrial sensors market is witnessing denser sensor grids and higher attach rates in both brownfield and greenfield facilities.

Rising Capital Expenditure on Clean-Energy Infrastructure

The Department of Energy's Speed to Power initiative halves interconnection timelines, spurring demand for differential pressure sensors in wind-turbine pitch systems and current sensors inside grid-tied inverters. A USD 44 million federal outlay in 2025 targeted advanced metering and substation automation, both of which rely on temperature and partial-discharge sensors. Offshore wind developers specify intrinsically safe pressure and flow devices rated for Class I Division 1 environments under NFPA 70 Article 500.Battery storage projects, which added 15 GW in 2025, mandate thermal-runaway detection to meet UL 9540A standards. Clean-energy growth, therefore, tilts the United States industrial sensors market toward gas, current, and vibration sensing technologies that support asset availability and regulatory compliance.

Persistent Chip-Supply Volatility for Specialty MEMS Dies

Lead times for automotive-grade piezoresistive pressure dies and capacitive accelerometers extended beyond 26 weeks in late 2024, delaying retrofit programs. Infineon's XENSIV and Bosch Sensortec's BMI families faced the steepest allocation constraints. Domestic foundries funded by the CHIPS Act are ramping up production but are not expected to match Asian manufacturing capacity until at least 2028, keeping supply risks elevated. Dual sourcing and redesigns around SOI and piezoelectric alternatives increase non-recurring engineering costs, tempering near-term growth of the United States industrial sensors market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of the United States Semiconductor Fabs Driving Sensor Demand

- Acceleration of Predictive-Maintenance Programs Post-2025

- Cybersecurity Risks Inhibiting Wireless Sensor Roll-Outs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wired solutions captured 73.82% of the United States industrial sensors market share in 2025 due to decades-long investment in 4-20 mA and HART loops. They remain indispensable for sub-5 millisecond shutdown tasks mandated by NFPA 85 and API 670. However, wireless nodes are forecast to grow at an 8.45% CAGR through 2031 on the back of private 5G, LoRaWAN, and Ethernet-APL adoption. Greenfield semiconductor fabs deploy thousands of IO-Link temperature sensors over wireless backhaul to preserve cleanroom flexibility, while Ethernet-APL supports intrinsic-safety compliance in hydrocarbon zones. The USAindustrial sensors market is converging toward hybrid architectures in which wired loops handle safety functions and wireless layers add diagnostics.

Private cellular pilots at automotive plants show that reducing cable pulls can lower installation budgets by 40%, creating a compelling case for wireless deployment in discrete manufacturing. Conversely, brownfield chemical sites often retain wired retrofits because spectrum licenses and gateway hardware dilute the wireless value proposition. Vendors such as Emerson and Honeywell now offer unified asset-management suites that aggregate both wired and wireless data streams, demonstrating how hybrid connectivity will underpin the next growth phase of the US industrial sensors market.

List of Companies Covered in this Report:

- ABB Ltd

- Analog Devices, Inc.

- Banner Engineering Corp.

- Bosch Sensortec GmbH

- Endress+Hauser AG

- Emerson Electric Co.

- Honeywell International Inc.

- IFM Efector, Inc.

- Infineon Technologies AG

- Keyence Corporation of America

- Omega Engineering Inc.

- Omron Corporation

- Pepperl+Fuchs, Inc.

- Rockwell Automation, Inc.

- Sensata Technologies, Inc.

- Sick AG

- TE Connectivity Ltd.

- Texas Instruments Incorporated

- The Krohne Group

- Vega Grieshaber KG

- Yokogawa Electric Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in IIoT Adoption Across Discrete and Process Industries

- 4.2.2 Rising Capital Expenditure on Clean-Energy Infrastructure

- 4.2.3 Expansion of the United States Semiconductor Fabs Driving Sensor Demand in Advanced Manufacturing

- 4.2.4 Acceleration of Predictive-Maintenance Programs Post-2025

- 4.2.5 Federal Incentives for Reshoring Critical Industries

- 4.2.6 Growth of Hydrogen Economy Requiring Novel Pressure and Gas Sensors

- 4.3 Market Restraints

- 4.3.1 Persistent Chip-Supply Volatility for Specialty MEMS Dies

- 4.3.2 Cyber-Security Risks Inhibiting Wireless Sensor Roll-Outs

- 4.3.3 High Total Cost of Ownership for Intrinsically Safe Sensors in Explosive Zones

- 4.3.4 Standards Fragmentation Across Industrial Communications Protocols

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Connectivity

- 5.1.1 Wired Solutions

- 5.1.2 Wireless Solutions

- 5.2 By Sensor Type

- 5.2.1 Pressure Sensors

- 5.2.2 Flow Sensors

- 5.2.3 Temperature Sensors

- 5.2.4 Level Sensors

- 5.2.5 Gas Sensors

- 5.2.6 Proximity and Photoelectric Sensors

- 5.2.7 Vibration Sensors

- 5.2.8 Other Types of Sensors

- 5.3 By End-User Industry

- 5.3.1 Oil and Gas

- 5.3.2 Chemicals and Petrochemicals

- 5.3.3 Water and Wastewater

- 5.3.4 Food and Beverage

- 5.3.5 Power Generation

- 5.3.6 Automotive

- 5.3.7 Pharmaceutical and Life Sciences

- 5.3.8 Aerospace and Defense

- 5.3.9 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Analog Devices, Inc.

- 6.4.3 Banner Engineering Corp.

- 6.4.4 Bosch Sensortec GmbH

- 6.4.5 Endress+Hauser AG

- 6.4.6 Emerson Electric Co.

- 6.4.7 Honeywell International Inc.

- 6.4.8 IFM Efector, Inc.

- 6.4.9 Infineon Technologies AG

- 6.4.10 Keyence Corporation of America

- 6.4.11 Omega Engineering Inc.

- 6.4.12 Omron Corporation

- 6.4.13 Pepperl+Fuchs, Inc.

- 6.4.14 Rockwell Automation, Inc.

- 6.4.15 Sensata Technologies, Inc.

- 6.4.16 Sick AG

- 6.4.17 TE Connectivity Ltd.

- 6.4.18 Texas Instruments Incorporated

- 6.4.19 The Krohne Group

- 6.4.20 Vega Grieshaber KG

- 6.4.21 Yokogawa Electric Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment