PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959591

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959591

Industrial Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

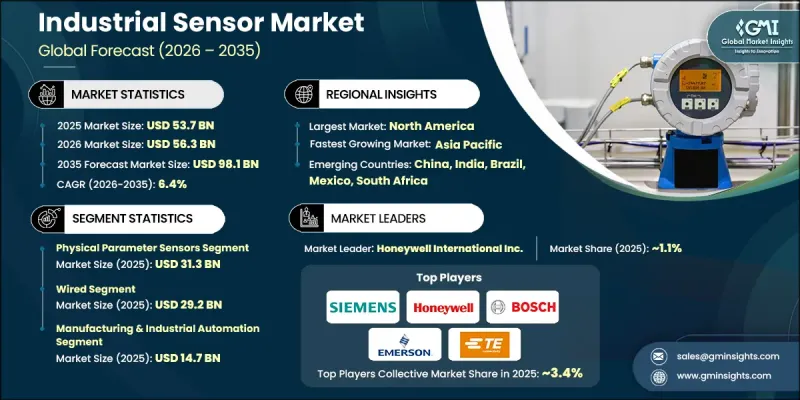

The Global Industrial Sensor Market was valued at USD 53.7 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 98.1 billion by 2035.

Industrial sensors have become integral to modern manufacturing, energy, aerospace, and logistics operations, enabling precise monitoring and control of machinery, processes, and environmental conditions. As industrial environments grow more complex and automated, the need for real-time data and situational awareness has intensified. These sensors allow organizations to track equipment performance, ensure safety compliance, and maintain process efficiency. Increasing production volumes, coupled with rising adoption of smart manufacturing, industrial IoT, and predictive maintenance solutions, are further boosting demand. Companies now rely on sensor technology not only for operational reliability but also for process optimization, early fault detection, and seamless integration with analytics platforms. The push for higher precision, efficiency, and sustainability continues to drive innovation and deployment across global industrial sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $53.7 Billion |

| Forecast Value | $98.1 Billion |

| CAGR | 6.4% |

The physical parameter sensors segment generated USD 31.3 billion in 2025. Physical parameter sensors dominate due to their ability to provide high-precision measurements of force, torque, pressure, vibration, and temperature. These sensors are crucial for preventing downtime, maintaining operational efficiency, and enabling predictive maintenance in industrial machinery and production lines. Their durability in harsh conditions and compatibility with automation systems make them indispensable across manufacturing, energy, and aerospace applications.

The wired segment held USD 29.2 billion in 2025. Wired sensors remain popular due to their reliable data transmission, robustness, and resistance to interference. Industrial facilities, processing plants, and energy operations prefer wired solutions for continuous monitoring, where uninterrupted and accurate data flow is critical. Their compatibility with existing automation infrastructure ensures consistent performance in challenging environments.

North America Industrial Sensor Market accounted for 35.2% share in 2025. Growth in this region is fueled by investments in smart manufacturing, connected factories, and industrial automation solutions. Companies are increasingly implementing IoT, AI, and advanced analytics to optimize processes, reduce downtime, and improve safety. Regulatory compliance, energy efficiency, and sustainability initiatives are also driving the adoption of high-precision and application-specific sensors, strengthening North America's leadership in the industrial sensor market.

Prominent players in the Global Industrial Sensor Market include ABB Ltd., Allegro MicroSystems, Inc., Balluff GmbH, Banner Engineering, Bosch Group, Endress+Hauser Group Services AG, Emerson Electric Co., Honeywell International Inc., ifm electronic gmbh, Keyence Corporation, LEM Holding, Melexis, OMRON Corporation, Panasonic Industry, Pepperl+Fuchs SE, Rockwell Automation, Inc., SICK AG, Sensatec GmbH, Sensata Technologies, Schneider Electric SE, Siemens AG, STMicroelectronics, TE Connectivity, Texas Instruments, and Turck Group. Key strategies adopted by industrial sensor companies to strengthen market presence include expanding R&D to develop high-precision and application-specific sensors, integrating AI and IoT capabilities for predictive maintenance and process optimization, and forming partnerships with industrial automation and manufacturing solution providers. Companies focus on enhancing reliability, durability, and performance under harsh operating conditions, while also improving energy efficiency and reducing costs. Geographic expansion, targeting emerging industrial markets, and compliance with regional standards help increase global reach. Businesses are leveraging direct sales, distribution networks, and digital platforms to improve customer engagement, ensure quick deployment, and provide value-added services. Product innovation, service support, and sustainable manufacturing practices further solidify market position and long-term competitiveness.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Sensor type trends

- 2.2.2 Technology trends

- 2.2.3 Connectivity trends

- 2.2.4 End Use industry trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing Adoption of Industrial Automation and Smart Manufacturing

- 3.2.1.2 Integration of IoT and Industrial Internet of Things (IIoT) Technologies

- 3.2.1.3 Rising Demand for Predictive Maintenance and Real-Time Monitoring

- 3.2.1.4 Expansion in Renewable Energy and Advanced Power Generation Systems

- 3.2.1.5 Stringent Regulatory Compliance and Safety Standards

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Initial Investment and Integration Complexity

- 3.2.2.2 Data Security and Reliability Concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of Smart Factories and Industry 4.0 Initiatives

- 3.2.3.2 Expansion in Renewable Energy and Advanced Power Systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Sensor Type, 2022 - 2035 (USD Billion)

- 5.1 Key trends

- 5.2 Physical Parameter Sensors

- 5.2.1 Temperature Sensors

- 5.2.2 Pressure Sensors

- 5.2.3 Flow Sensors

- 5.2.4 Level Sensors

- 5.2.5 Position & Motion Sensors

- 5.3 Proximity Sensors

- 5.3.1 Inductive & Capacitive Proximity

- 5.3.2 Optical / Photoelectric Sensors

- 5.4 Environmental Monitoring Sensors

- 5.4.1 Humidity & Moisture Sensors

- 5.4.2 Vibration & Condition Sensors

- 5.4.3 Gas & Chemical Sensors

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 MEMS (Micro-Electro-Mechanical Systems)

- 6.3 Optical/Photonic

- 6.4 Electrochemical

- 6.5 Mechanical

- 6.6 Electromagnetic

- 6.7 Ultrasonic/Acoustic

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By Connectivity, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 Wired

- 7.3 Wireless

Chapter 8 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Chemicals & Petrochemicals

- 8.3 Energy & Power

- 8.4 Food & Beverage

- 8.5 Manufacturing & Industrial Automation

- 8.6 Metals & Mining

- 8.7 Oil & Gas

- 8.8 Pharmaceuticals

- 8.9 Automotive & Transportation

- 8.10 Water & Wastewater Treatment

- 8.11 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ABB Ltd.

- 10.2 Allegro MicroSystems, Inc.

- 10.3 Balluff GmbH

- 10.4 Banner Engineering

- 10.5 Bosch Group

- 10.6 Endress+Hauser Group Services AG

- 10.7 Emerson Electric Co.

- 10.8 Honeywell International Inc.

- 10.9 ifm electronic gmbh

- 10.10 Keyence Corporation

- 10.11 LEM Holding

- 10.12 Melexis

- 10.13 OMRON Corporation

- 10.14 Panasonic Industry

- 10.15 Pepperl+Fuchs SE

- 10.16 Rockwell Automation, Inc.

- 10.17 SICK AG

- 10.18 Sensatec GmbH

- 10.19 Sensata Technologies

- 10.20 Schneider Electric SE

- 10.21 Siemens AG

- 10.22 STMicroelectronics

- 10.23 TE Connectivity

- 10.24 Texas Instruments

- 10.25 Turck Group