PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066735

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066735

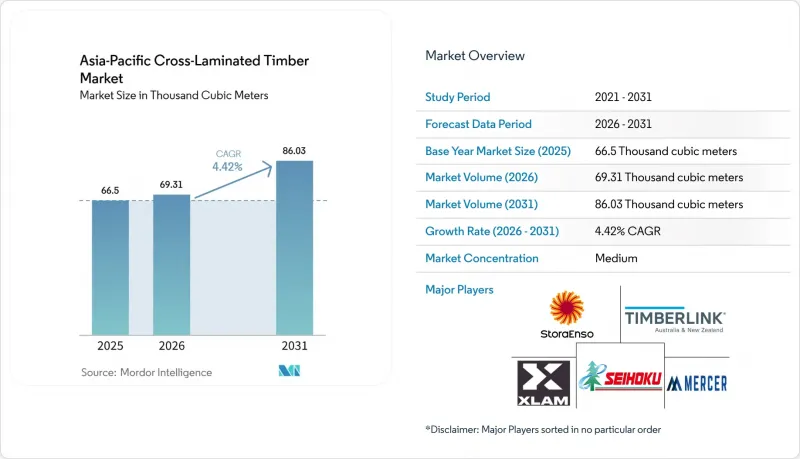

Asia-Pacific Cross-Laminated Timber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific cross-Laminated timber market size is expected to increase from 66.5 Thousand cubic meters in 2025 to 69.31 Thousand cubic meters in 2026 and reach 86.03 Thousand cubic meters by 2031, growing at a CAGR of 4.42% over 2026-2031.

This report is Segmented by Type (Adhesive Bonded and Mechanically Fastened), Application (Residential and Non-Residential), and Geography (China, India, Japan, South Korea, Australia and Zealand, and the Rest of Asia-Pacific). The Market Size and Forecasts are Provided in Terms of Volume (Cubic Meters).

Asia-Pacific Cross-Laminated Timber Market Trends and Insights

Rapid Urban Mid-Rise Construction Boom in China and India

China and India together contribute more than 60% of annual mid-rise residential starts, and fresh policy signals are directing a measurable fraction toward modern wood structures. Jiangsu's January 2026 directive obliges public projects above 5,000 m2 to evaluate CLT, adding 8,000-12,000 m3 of yearly demand inside the province. India's first mass-timber residence in Goa and IIT Roorkee's INR 120 million (USD 1.38 million) training center are creating local design capacity and anchoring supply chains. Builders value CLT's 20-25% weight advantage because it limits deep foundations in land-scarce metros where plots command premium prices. With engineering talent graduating from new programs by 2028, most incremental volume is expected to appear from 2027 onward.

Green-Building Incentives Across Japan, South Korea, Australia

CASBEE, G-SEED, and Green Star certifications now award extra points for low-embodied-carbon materials validated by Environmental Product Declarations. Japan's 2024 guidelines grant up to 10% floor-area-ratio bonuses for domestic CLT, which Mitsui Fudosan used to add an additional storey to its 2025 Nihonbashi project. South Korea mandates Green 2 for all public buildings, effectively making Environmental Product Declaration (EPD) documentation a market-entry requirement for suppliers. Australia's Clean Energy Finance Corporation has set aside AUD 300 million in low-interest loans for net-zero mass-timber projects, underwriting 42,000 m3 of panels by Q1 2026. These incentives disproportionately support adhesive-bonded CLT today but are likely to persist well beyond 2031 and continue lifting specification rates.

Moisture-Induced Delamination and Mold Risk in Tropical Climates

Sustained humidity above 75% pushes lamella moisture beyond adhesive tolerance, and field surveys in Malaysia and northern Australia documented delamination in 8-12% of unprotected panels within two years. Mold appeared within one year on 26% of 34 tracked projects across Indonesia, Malaysia, and Thailand, forcing remedial costs that neutralize CLT's price advantage. Silane-modified polyurethane solves the chemistry but is still 30-40% more expensive and remains uncertified for structural use. Until codes mandate vapor control layers or adhesives improve, tropical humidity will remain a drag on adoption.

Other drivers and restraints analyzed in the detailed report include:

- Prefabricated Mass-Timber Modular Demand Post-COVID Logistics Shift

- Hybrid Timber-Steel High-Rise Approvals Unlocking New Volume

- Shortage of CLT-Skilled Labor and Inspection Expertise

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Adhesive-bonded panels command 68.12% share because continuous glue lines deliver higher shear capacity, critical for tall-building cores. Binderholz's Burgbernheim Plant II now produces lot-size-one CLT panels up to 18 m long, underlining economies of scale that keep bonded systems price-competitive. The Asia-Pacific cross-laminated timber market size for adhesive panels should retain leadership in seismic and long-span applications, yet mechanically fastened formats are on track to reach a higher market share by 2031 as circular-economy standards tighten.

Mechanically fastened laminated timber is forecast to expand at 7.31% CAGR to 2031, outperforming the wider Asia-Pacific cross-laminated timber market. Demand accelerates because Japanese and South Korean rating systems grant extra credits for reversible construction methods that allow post-use disassembly. A University of British Columbia test in 2024 showed five-ply mechanically fastened CLT reached 92% of the bending strength of bonded panels, narrowing performance gaps for residential floors. Builders in Tokyo and Seoul have already substituted mechanically fastened CLT in low-stress diaphragms to secure sustainability bonuses.

List of Companies Covered in this Report:

- AGROP NOVA a.s.

- B&K Structures

- Binderholz GmbH

- Eugen Decker Holzindustrie KG

- HASSLACHER Holding GmbH

- HESS Timber GmbH

- Holmen AB

- KLH Massivholz GmbH

- Mayr-Melnhof Holz Holding AG

- Meiken Lamwood Corp.

- Mercer International Inc.

- Pfeifer Group

- Schilliger Holz AG

- SEIHOKU Corporation

- SIPEUROPE s.r.o.

- SmartLam NA

- Sterling Structural

- Stora Enso

- Structurlam Mass Timber

- Timberlink Australia & New Zealand

- XLam Australia Pty Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urban mid-rise construction boom in China and India

- 4.2.2 Green-building incentives across Japan, South Korea, Australia

- 4.2.3 Prefabricated mass-timber modular demand post-COVID logistics shift

- 4.2.4 Hybrid timber-steel high-rise approvals unlocking new volume

- 4.2.5 Indigenous bamboo-reinforced CLT RandD in China and South-East Asia

- 4.3 Market Restraints

- 4.3.1 Moisture-induced delamination and mold risk in tropical climates

- 4.3.2 Shortage of CLT-skilled labor and inspection expertise

- 4.3.3 Building-code fragmentation slowing project approvals

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products and Services

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Adhesive Bonded

- 5.1.2 Mechanically Fastened

- 5.2 By Application

- 5.2.1 Residential

- 5.2.2 Non-Residential

- 5.2.2.1 Commercial

- 5.2.2.2 Industrial / Institutional

- 5.2.2.3 Other Applications

- 5.3 By Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Australia and New Zealand

- 5.3.6 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AGROP NOVA a.s.

- 6.4.2 B&K Structures

- 6.4.3 Binderholz GmbH

- 6.4.4 Eugen Decker Holzindustrie KG

- 6.4.5 HASSLACHER Holding GmbH

- 6.4.6 HESS Timber GmbH

- 6.4.7 Holmen AB

- 6.4.8 KLH Massivholz GmbH

- 6.4.9 Mayr-Melnhof Holz Holding AG

- 6.4.10 Meiken Lamwood Corp.

- 6.4.11 Mercer International Inc.

- 6.4.12 Pfeifer Group

- 6.4.13 Schilliger Holz AG

- 6.4.14 SEIHOKU Corporation

- 6.4.15 SIPEUROPE s.r.o.

- 6.4.16 SmartLam NA

- 6.4.17 Sterling Structural

- 6.4.18 Stora Enso

- 6.4.19 Structurlam Mass Timber

- 6.4.20 Timberlink Australia & New Zealand

- 6.4.21 XLam Australia Pty Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment