PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066765

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066765

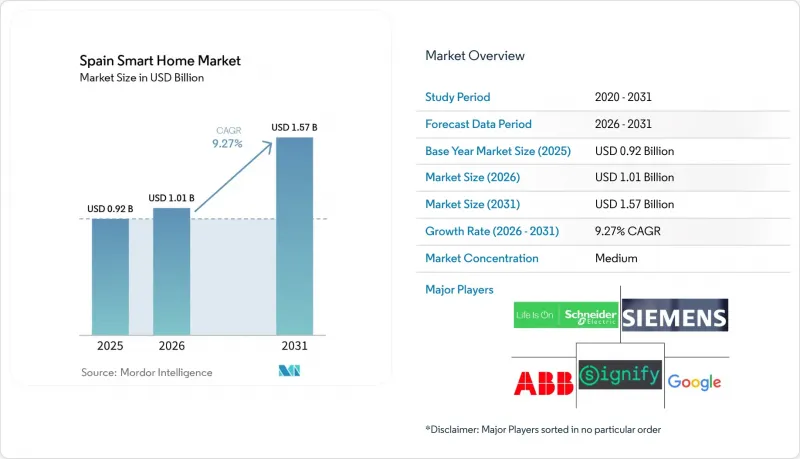

Spain Smart Home - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, spain smart home market size in 2026 is estimated at USD 1.01 billion, growing from 2025 value of USD 0.92 billion with 2031 projections showing USD 1.57 billion, growing at 9.27% CAGR over 2026-2031.

This report is Segmented by Product (Comfort and Lighting, Control and Connectivity, and More), Connectivity Technology (Wi-Fi, Bluetooth, and More), Installation Type (New Construction, Retrofit/Existing Homes), Sales Channel (E-Commerce, Electrical Wholesalers, and More), End-User Profile (Single-Family Houses, Multi-Dwelling Units), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Spain Smart Home Market Trends and Insights

Government-backed Energy-efficiency Subsidies for Residential Retrofits

Incentives such as the PREE 5000 program and income-tax deductions covering up to 60% of qualifying costs narrow payback periods for connected energy-management systems, converting latent interest into active demand. The ERESEE 2030 target of 1.2 million dwelling upgrades ensures a persistent pipeline, while staged renovation roadmaps common in Spanish households translate into recurring opportunities for device add-ons.

Rapid FTTH and 5G Rollout Boosting Device Reliability

With 93% population coverage in fiber, Spain leads Europe in very-high-capacity network reach, delivering low-latency performance critical for cloud-dependent voice assistants and security cameras. Digital Spain 2026 allocates additional 5G funding to rural provinces, enabling Spain smart home market growth beyond metropolitan hubs.

Persistent Data-privacy Scepticism Among Spanish Consumers

Despite GDPR safeguards, 30% of Spanish Internet users report technical concerns when interacting with connected services, reinforcing caution toward always-listening devices Eurostat. Manufacturers pursuing the Spain smart home market must offer transparent data handling and local processing options to ease trust barriers.

Other drivers and restraints analyzed in the detailed report include:

- Growth in single-person and elderly households

- Matter-enabled interoperability

- High Upfront Device Costs vs Average Household Income

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Comfort and Lighting solutions contributed 37.92% of Spain smart home market share in 2025, reflecting widespread acceptance of smart LEDs, thermostats, and shading controls that align with daily lifestyle patterns. Smart Appliances hold the strongest upside, expanding at 10.18% CAGR as energy-label rules tighten and dynamic tariffs reward intelligent scheduling. Home Entertainment adoption rides on ubiquitous broadband, though growth moderates with saturation in larger cities. Security systems sustain steady uptake, especially in holiday rentals seeking remote monitoring assurance. Integrated Energy Management platforms link rooftop PV, heat pumps, and household loads, positioning the Spain smart home market for grid-interactive services that complement the national solar boom. Spanish firms such as Fermax tailor intercom-linked lighting packages for multi-dwelling units, underscoring local design preferences shaped by Mediterranean building traditions.

Innovations in appliance-embedded Wi-Fi chips and cost-effective single-board controllers expand entry-level options, lowering barriers for first-time buyers. Voice assistant tie-ins with refrigerators and washing machines amplify convenience, while regulator-mandated eco-modes foster adoption among cost-sensitive households. The Spain smart home market size for appliances could represent a fifth of all connected-device revenue by 2030 if EU eco-design proposals progress, introducing time-of-use optimization as a default feature. Insurance firms piloting premium discounts for leak-sensing dishwashers illustrate new monetization pathways. Manufacturers that integrate over-the-air updates and Matter compliance from launch are best placed to capture cross-brand households seeking future-proof investments.

Wi-Fi remains the backbone, hosting 45.88% of installed nodes in 2025, yet Thread/Matter-ready chip shipments are posting 11.62% CAGR as brands race to offer frictionless pairing and lower standby power. Bluetooth Low Energy underpins wearables and portable sensors, while Zigbee and Z-Wave sustain modest use in legacy hubs. The Spain smart home market values devices capable of switching intelligently between protocols, hence chipset makers bundle Wi-Fi, BLE, and 802.15.4 radios on a single die. Edge-AI processors that run local intent recognition reduce cloud traffic, answering privacy worries. Telecom providers bundle multi-protocol routers with new fiber contracts, cementing their gatekeeper role and nudging households toward unified ecosystems.

Matter's gradual reach into appliances, HVAC, and security cameras simplifies purchase decisions and cuts return rates at retail. Retailers report drop-in support calls once customers migrate to single-app environments. Furthermore, utility-managed demand-response pilots exploit Thread border routers embedded in smart speakers to deliver rapid load-shed signals without extra hardware. The Spain smart home market continues to reward vendors that maintain over-the-air upgradability, positioning products for regulatory changes around cybersecurity labeling proposed by the EU.

List of Companies Covered in this Report:

- Schneider Electric SE

- ABB Ltd

- Siemens AG

- Signify Holding

- Google LLC

- GE Lighting (a Savant Co.)

- EVVR ApS

- Fibaro Group SA

- Samsung Electronics Co. Ltd

- LG Electronics

- Amazon.com Inc.

- Apple Inc.

- Bosch Smart Home GmbH

- Somfy SA

- Fermax Electronica S.A.U.

- Wallbox N.V.

- Legrand SA/Netatmo

- Nice SpA

- Philips Hue

- Huawei Technologies Co. Ltd (HiLink)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-backed energy-efficiency subsidies for residential retrofits

- 4.2.2 Rapid FTTH and 5G rollout boosting device reliability

- 4.2.3 Surge in single-person and elderly households demanding assisted-living automation

- 4.2.4 Matter standard enabling cross-brand interoperability

- 4.2.5 Rising electricity prices intensifying energy-management adoption

- 4.2.6 PropTech and smart-rental platforms driving turnkey smart apartments

- 4.3 Market Restraints

- 4.3.1 Persistent data-privacy scepticism among Spanish consumers

- 4.3.2 High upfront device costs vs average household income

- 4.3.3 Fragmented after-sales service network outside tier-1 cities

- 4.3.4 Lack of VAT incentives for smart-home devices vs solar PV

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Intensity of Competitive Rivalry

- 4.6.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Product

- 5.1.1 Comfort and Lighting

- 5.1.2 Control and Connectivity

- 5.1.3 Energy Management

- 5.1.4 Home Entertainment

- 5.1.5 Security

- 5.1.6 Smart Appliances

- 5.2 By Connectivity Technology

- 5.2.1 Wi-Fi

- 5.2.2 Bluetooth

- 5.2.3 Zigbee

- 5.2.4 Z-Wave

- 5.2.5 Thread/Matter-ready ICs

- 5.3 By Installation Type

- 5.3.1 New Construction

- 5.3.2 Retrofit/Existing Homes

- 5.4 By Sales Channel

- 5.4.1 E-commerce

- 5.4.2 Consumer Electronics Retailers

- 5.4.3 Electrical Wholesalers

- 5.4.4 Professional Installers/Integrators

- 5.5 By End-user Profile

- 5.5.1 Single-family Houses

- 5.5.2 Multi-dwelling Units (MDUs)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 ABB Ltd

- 6.4.3 Siemens AG

- 6.4.4 Signify Holding

- 6.4.5 Google LLC

- 6.4.6 GE Lighting (a Savant Co.)

- 6.4.7 EVVR ApS

- 6.4.8 Fibaro Group SA

- 6.4.9 Samsung Electronics Co. Ltd

- 6.4.10 LG Electronics

- 6.4.11 Amazon.com Inc.

- 6.4.12 Apple Inc.

- 6.4.13 Bosch Smart Home GmbH

- 6.4.14 Somfy SA

- 6.4.15 Fermax Electronica S.A.U.

- 6.4.16 Wallbox N.V.

- 6.4.17 Legrand SA/Netatmo

- 6.4.18 Nice SpA

- 6.4.19 Philips Hue

- 6.4.20 Huawei Technologies Co. Ltd (HiLink)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment