PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066770

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066770

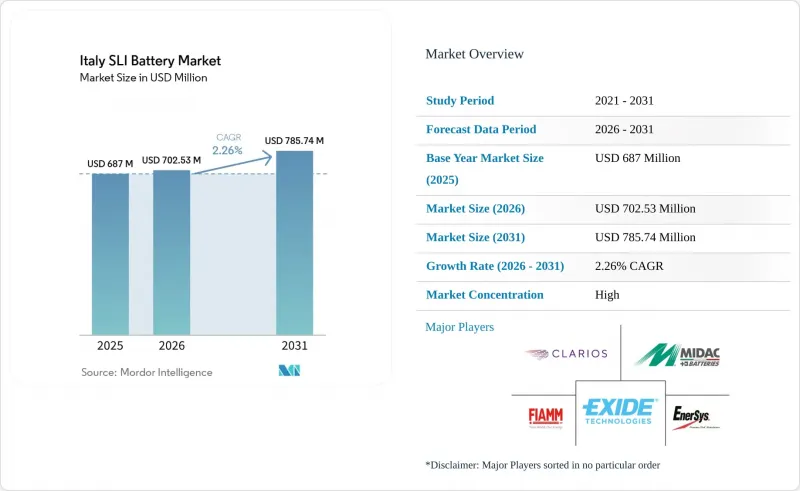

Italy SLI Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the italy sLI battery market size is expected to grow from USD 687 million in 2025 to USD 702.53 million in 2026 and is forecast to reach USD 785.74 million by 2031 at 2.26% CAGR over 2026-2031.

This report is Segmented by Battery Type (Flooded, Enhanced Flooded, Absorbent Glass Mat, and Gel Cell VRLA), Battery Voltage (Up To 12V, 12V, 48V, and Above 60V), Application (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Two-/Three-Wheelers, Agricultural and Off-Highway Vehicles, Industrial Motive Power, and Stand-by/Backup).

Italy SLI Battery Market Trends and Insights

Growing vehicle-parc & replacement demand

Italy's 41 million-unit parc, averaging 13 years in age, generates a deep pool of batteries nearing end-of-life. Slow fleet turnover, new registrations equal only 3-4% of total parc, means flooded batteries installed before 2015 are now cycling through second or third replacements. The stability of this demand segment shields the Italy SLI battery market from abrupt volume declines even as EV adoption lags Northern Europe. Winter cold-cranking failures rise sharply in batteries older than five years, prompting retailers to promote diagnostic checks and seasonal discounts.

Rising AGM/EFB adoption in start-stop cars

Start-stop systems topped 68% penetration in Europe by 2024, and Italian OEMs mandate AGM or EFB fitment on new micro-hybrid platforms. As these vehicles age, aftermarket replacements are set to accelerate, favoring AGM chemistry that tolerates deep cycling. Exide's dual-terminal AGM B24 series widened fitment coverage by up to 1 million units, underscoring the priority manufacturers place on versatility. Distributors must therefore invest in AGM stocking, new racking, and staff training to capture the revenue upswing.

Li-ion 12 V auxiliaries gaining share

EUROBAT projects a 50/50 split between lead-acid and lithium-ion in 12 V auxiliary batteries by 2030 as ADAS and infotainment loads soar. Lithium-ion offers faster recharge and lighter weight, but lead-acid holds a 60-70% cost edge and better cold-cranking at sub-zero temperatures. Italian manufacturers are racing to introduce Thin-Plate Pure Lead and carbon-enhanced variants to hold ground in this critical niche.

Other drivers and restraints analyzed in the detailed report include:

- Micro-hybrid retrofit boom in urban fleets

- EU circular-economy push for lead recycling

- Shrinking ICE production under 2030 targets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

AGM already serves the majority of start-stop cars and is forecast to expand at a 6.31% CAGR, compared with the Italy SLI battery market's overall 2.26% growth. Flooded batteries still dominate replacement sales for vehicles built before 2015, but their share will erode as the AGM replacement wave matures. EFB provides a mid-price option for fleet operators who need higher cycle life than flooded units can provide, yet balk at full-AGM pricing.

The Italy SLI battery market size for AGM units is projected to rise from USD 227 million in 2025 to nearly USD 327.7 million by 2031 as start-stop penetration deepens. Exide's M3-rated AGM B24 launch shows how manufacturers are broadening terminal options to trim SKU counts for distributors. Meanwhile, flooded designs will persist in cost-pressured Southern regions but decline nationally as consumer education on AGM benefits increases.

List of Companies Covered in this Report:

- FIAMM Energy Technology S.p.A.

- Clarios (Johnson Controls)

- Exide Technologies

- Midac SpA

- Sunlight Group

- EnerSys

- GS Yuasa Corporation

- Banner GmbH

- C&D Technologies Inc.

- Leoch International Tech. Ltd.

- Accumulatori Ariete S.R.L.

- Trojan Battery Company

- NorthStar Battery

- Bosch (Battery Division)

- Varta AG

- Yuasa Battery (Europe) Ltd.

- East Penn Mfg. (Deka)

- TAB Batteries

- Moll Batterien GmbH

- VoltA Batteries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing vehicle-parc & replacement demand

- 4.2.2 Rising AGM/EFB adoption in start-stop cars

- 4.2.3 Micro-hybrid retrofit boom in urban fleets

- 4.2.4 EU circular-economy push for lead recycling

- 4.2.5 Carbon-footprint labelling favours local supply

- 4.2.6 Expansion of automotive aftermarket e-commerce

- 4.3 Market Restraints

- 4.3.1 Li-ion 12 V auxiliaries gaining share

- 4.3.2 Shrinking ICE production under 2030 targets

- 4.3.3 Battery-passport compliance cost for SMEs

- 4.3.4 Lead-scrap price volatility & export curbs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Battery Type

- 5.1.1 Flooded (Conventional)

- 5.1.2 Enhanced Flooded (EFB)

- 5.1.3 Absorbent Glass Mat (AGM)

- 5.1.4 Gel Cell VRLA

- 5.2 By Battery Voltage

- 5.2.1 Up to 12 V

- 5.2.2 12 V

- 5.2.3 48 V

- 5.2.4 Above 60 V

- 5.3 By Application

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.3.4 Two-/Three-Wheelers

- 5.3.5 Agricultural and Off-Highway Vehicles

- 5.3.6 Industrial Motive Power (Forklifts, Material-Handling)

- 5.3.7 Stand-by/Backup (Telecom, UPS)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 FIAMM Energy Technology S.p.A.

- 6.4.2 Clarios (Johnson Controls)

- 6.4.3 Exide Technologies

- 6.4.4 Midac SpA

- 6.4.5 Sunlight Group

- 6.4.6 EnerSys

- 6.4.7 GS Yuasa Corporation

- 6.4.8 Banner GmbH

- 6.4.9 C&D Technologies Inc.

- 6.4.10 Leoch International Tech. Ltd.

- 6.4.11 Accumulatori Ariete S.R.L.

- 6.4.12 Trojan Battery Company

- 6.4.13 NorthStar Battery

- 6.4.14 Bosch (Battery Division)

- 6.4.15 Varta AG

- 6.4.16 Yuasa Battery (Europe) Ltd.

- 6.4.17 East Penn Mfg. (Deka)

- 6.4.18 TAB Batteries

- 6.4.19 Moll Batterien GmbH

- 6.4.20 VoltA Batteries

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment