PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072446

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072446

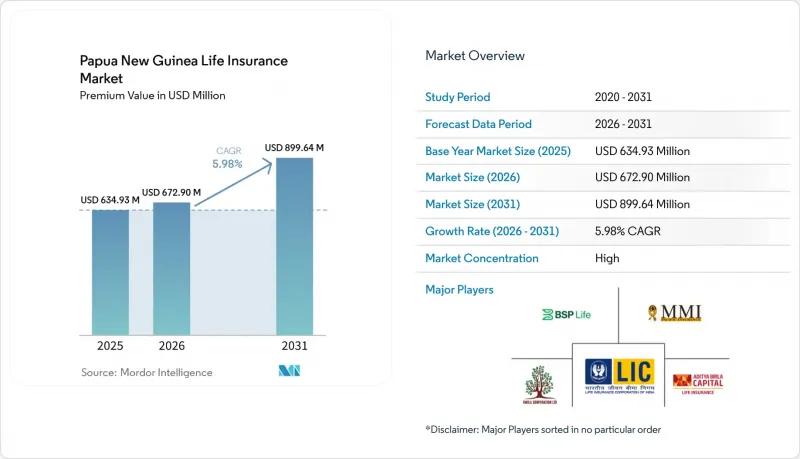

Papua New Guinea Life Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the papua new guinea life insurance market size in terms of premium value is expected to grow from USD 634.93 million in 2025 to USD 672.90 million in 2026 and is forecast to reach USD 899.64 million by 2031 at 5.98% CAGR over 2026-2031.

This report is Segmented by Product Type (Term Life Insurance, Whole Life Insurance, Endowment Insurance, and More), Distribution Channel (Agents, Brokers, Banks, and More), Premium Type (Regular Premium, Single Premium), Customer Age Group (0-24 Years, 25-44 Years, 45-64 Years, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Papua New Guinea Life Insurance Market Trends and Insights

Mandatory Employer-Superannuation Contributions Spur Group-Life Uptake

Nasfund managed PGK 8.92 billion (USD 2.4 billion) in member funds across more than 724,680 accounts in 2025, and compulsory payroll deductions automatically bundle death and disability coverage that lifts group penetration. Predictable premium flows reduce underwriting costs, enabling lower group rates and broader coverage for mining, government, and banking workers. Prudential rules enforced by the Bank of Papua New Guinea safeguard reserves, which sustain insurer appetite for long-duration liabilities. Integrating insurance into workplace benefits offsets low retail awareness, particularly for high-risk industries that confront income-protection gaps. Employers exceeding minimum contribution thresholds further enlarge the overall Papua New Guinea life insurance market as voluntary top-ups translate into higher sum-assured levels.

Mobile & Agent-Led Micro-Insurance Expansion

BIMA reached 282,289 customers by partnering with Digicel to allow premium deductions from airtime, overcoming branch scarcity and language barriers. Agent networks explain simple K2.70 monthly covers in local dialects, unlocking sales among cocoa farmers, market vendors, and seasonal laborers. The Digizen digital ID pilot with 2,500 rural enrollees simplifies KYC and instant policy issuance. Scalable commissions keep agents active in remote posts, while mobile penetration of 42% provides a ready platform for policy alerts and claims filing. Regulatory sandboxes let carriers test parametric models that pay via mobile wallets, a format suited to low-ticket risks and disaster compensation.

Low Financial Literacy & Limited Awareness of Insurance

Surveys cite "don't know what insurance is" as the leading barrier, and traditional wantok systems reduce perceived need for formal cover. Traditional wantok systems, which emphasize communal support, further reduce the need for formal insurance coverage in the eyes of many. The absence of insurance-related topics in school curricula prevents knowledge about insurance from being passed down to younger generations. With over 600 islands, media campaigns struggle to reach all areas, limiting efforts to raise awareness. Additionally, only 36% of women use digital financial services, which widens the gap between genders in accessing financial tools. Community workshops conducted in Tok Pisin have shown positive results in educating people, but the high costs of scaling these workshops to cover 800 different languages make widespread implementation challenging.

Other drivers and restraints analyzed in the detailed report include:

- Growing Urban Middle Class and Formal Employment

- Strengthening Prudential & Solvency Supervision by BPNG

- Geographic Dispersion and Poor Infrastructure Drive Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Unit-linked contracts captured 37.85% of Papua New Guinea's life insurance market share in 2025 as resource-sector bonuses funneled into wealth-building vehicles. The segment benefits from transparent fund values and the prospect of capital appreciation tied to LNG and mining equities. Annuity business is projected to compound at 6.87% through 2031, favored by aging workers seeking guaranteed post-retirement income in the absence of state pensions. Whole-life remains relevant for conservative savers wanting definite death benefits, while term assurance attracts young families needing affordable mortgage risk cover. Endowment plans support education savings as private school enrollment rises. Hybrid covers that bundle outpatient health benefits broaden protection scope and help carriers defend margins in a competitive field.

Steady growth within unit-linked accounts underscores rising financial sophistication among urban professionals, and it boosts asset-management revenues for carriers with in-house fund arms. The annuity line, though still niche in absolute volume, gains momentum as superannuation members approaching 55 convert lump-sum withdrawals into life-contingent streams. Endowments and other blended products remain important for diversifying insurer balance sheets and catering to parents wary of tuition inflation. Collectively, the product mix shows a shift from pure protection to solutions combining protection and savings, a trend that sustains the broader Papua New Guinea life insurance market.

Agents generated 44.15% of premiums in 2025 because relationship-based selling aligns with communal culture and local-language needs. They guide paperwork, facilitate claims, and meet customers in markets or villages, cementing trust. Telco-hosted platforms, however, are set to grow 7.72% annually through 2031 as Digicel Financial Services cross-sells life covers through 1.1 million mobile money accounts. Banks, notably BSP, leverage branch footprints and payroll relationships to push bundled covers during loan origination. Brokers handle corporate risk portfolios, and direct digital sales remain low due to limited literacy, but offer potential for straight-through processing of micro policies.

The channel landscape will diversify as open-API frameworks allow insurers to plug products into ride-hailing or agri-e-commerce apps, widening reach without duplicative infrastructure. Yet, high agent productivity and cultural proximity suggest that face-to-face will keep primacy for complex products. The evolving mix underpins resilient premium inflows for carriers while enhancing consumer choice, sustaining overall expansion of the Papua New Guinea life insurance market.

Complete Report Scope:

- By Product Type (Value)

- Term Life Insurance

- Whole Life Insurance

- Endowment Insurance

- Unit-Linked / Investment-Linked

- Annuity Insurance

- Other Types

- By Distribution Channel (Value)

- Agents

- Brokers

- Banks

- Direct to Consumer

- Online Marketplaces

- By Premium Type (Value)

- Regular Premium

- Single Premium

- By Customer Age Group (Value)

- 0-24 Years

- 25-44 Years

- 45-64 Years

- 65 Years & Above

List of Companies Covered in this Report:

- BSP Life (PNG) Ltd

- Capital Life Insurance Co Ltd

- Life Insurance Corporation (PNG) Ltd

- Pacific MMI Insurance Ltd

- Kwila Insurance Corp Ltd

- Workers Mutual Insurance (PNG) Ltd

- Capital Insurance Group Ltd

- BIMA (Milvik PNG)

- Digicel Financial Services PNG

- MiBank

- Bank South Pacific Financial Group Ltd

- Kina Securities Ltd (Kina Bank)

- ANZ Bank PNG

- Westpac PNG

- AON Risk Services PNG

- Marsh PNG

- Asian Insurance Brokers Ltd

- Bougainville Insurance Brokers Ltd

- Pacific Reinsurance Company

- Swiss Re (Pacific)

- Munich Re (Pacific)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory employer-superannuation contributions spur group-life uptake

- 4.2.2 Mobile & agent-led micro-insurance expansion

- 4.2.3 Growing urban middle class and formal employment

- 4.2.4 Strengthening prudential & solvency supervision by BPNG

- 4.2.5 Climate-risk financing pilots bundling life & catastrophe cover

- 4.2.6 Remittance-linked life-savings products for PNG diaspora

- 4.3 Market Restraints

- 4.3.1 Low financial literacy & limited awareness of insurance

- 4.3.2 Geographic dispersion and poor infrastructure drive costs

- 4.3.3 High communicable-disease mortality pushes premiums up

- 4.3.4 Punitive taxation of non-resident insurers curbs reinsurance appetite

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type (Value)

- 5.1.1 Term Life Insurance

- 5.1.2 Whole Life Insurance

- 5.1.3 Endowment Insurance

- 5.1.4 Unit-Linked / Investment-Linked

- 5.1.5 Annuity Insurance

- 5.1.6 Other Types

- 5.2 By Distribution Channel (Value)

- 5.2.1 Agents

- 5.2.2 Brokers

- 5.2.3 Banks

- 5.2.4 Direct to Consumer

- 5.2.5 Online Marketplaces

- 5.3 By Premium Type (Value)

- 5.3.1 Regular Premium

- 5.3.2 Single Premium

- 5.4 By Customer Age Group (Value)

- 5.4.1 0-24 Years

- 5.4.2 25-44 Years

- 5.4.3 45-64 Years

- 5.4.4 65 Years & Above

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 BSP Life (PNG) Ltd

- 6.4.2 Capital Life Insurance Co Ltd

- 6.4.3 Life Insurance Corporation (PNG) Ltd

- 6.4.4 Pacific MMI Insurance Ltd

- 6.4.5 Kwila Insurance Corp Ltd

- 6.4.6 Workers Mutual Insurance (PNG) Ltd

- 6.4.7 Capital Insurance Group Ltd

- 6.4.8 BIMA (Milvik PNG)

- 6.4.9 Digicel Financial Services PNG

- 6.4.10 MiBank

- 6.4.11 Bank South Pacific Financial Group Ltd

- 6.4.12 Kina Securities Ltd (Kina Bank)

- 6.4.13 ANZ Bank PNG

- 6.4.14 Westpac PNG

- 6.4.15 AON Risk Services PNG

- 6.4.16 Marsh PNG

- 6.4.17 Asian Insurance Brokers Ltd

- 6.4.18 Bougainville Insurance Brokers Ltd

- 6.4.19 Pacific Reinsurance Company

- 6.4.20 Swiss Re (Pacific)

- 6.4.21 Munich Re (Pacific)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment