PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072448

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072448

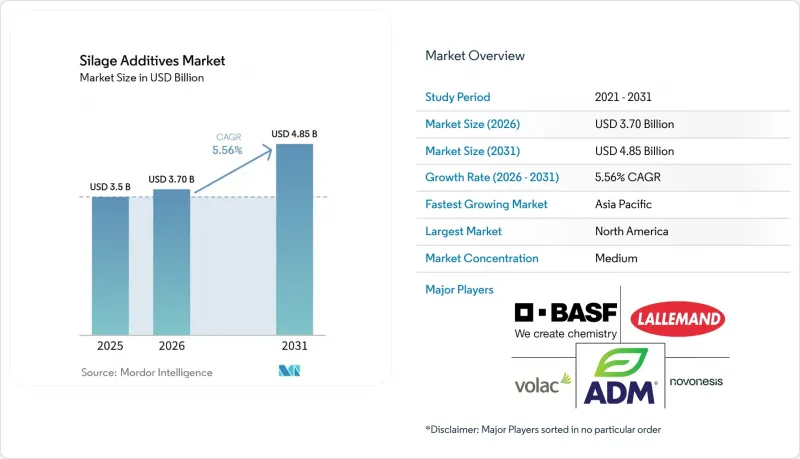

Silage Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the silage additives market size was valued at USD 3.5 billion in 2025 and estimated to grow from USD 3.7 billion in 2026 to reach USD 4.85 billion by 2031, at a CAGR of 5.56% during the forecast period (2026-2031).

This report is Segmented by Additive Type (Inoculants, Organic Acids and Salts, Enzymes, Adsorbents, Preservatives, and Other Types), by Silage Type (Cereals, Legumes, and Other Silage Types), and by Geography (North America, Europe, Asia-Pacific, South America, Middle-East, and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Global Silage Additives Market Trends and Insights

Intensifying Dairy and Beef Productivity Targets

The increasing focus on maximizing milk and beef production per animal is driving the silage additives market, as these products are essential for improving ration efficiency and forage quality. The United States Department of Agriculture (USDA) projects that average milk production per cow will reach 11.07 metric tons by 2026, highlighting the need for high-quality silage to support such productivity. Supporting this, Lallemand reported in 2025 that its MAGNIVA Platinum grass silage inoculant improved neutral detergent fiber digestibility by 5.4 percentage points over 160 days, resulting in an additional 1.23 kg of daily milk yield per cow during the trials. These results emphasize the role of silage additives in enhancing livestock output, shifting purchasing decisions to focus on their contribution to milk and meat production rather than just treatment costs. In regions with limited forage acreage, this shift is even more critical, as operations must achieve higher productivity from the same land base. Consequently, the growing demand for silage additives reflects the increasing priority placed on efficiency and output in livestock management.

Scaling Industrial Livestock and Forage Systems

The silage additives market is also expanding as industrial livestock systems spread across China, India, and Brazil, increasing the use of standardized forage preservation inputs. In China, the Ministry of Agriculture and Rural Affairs' feed-saving plan released in 2025 promotes silage use to reduce grain dependence in feed rations. Xinhua reported in February 2026 that Tongliao in Inner Mongolia had 80.39 million hectares of silage corn in 2025, showing how quickly the forage base is being scaled for commercial livestock systems. The FAO and the OECD also project global livestock output to grow by 16.6% through 2034, with lower-middle-income countries driving proportionately stronger herd expansion. That trend broadens the customer base for entry-level inoculants, buffered acid blends, and region-specific preservation products in the silage additives market.

Raw Material and Organic Acid Price Volatility

Raw material price remain volatile in the silage additives market because organic acid products are exposed to volatile chemical feedstocks and energy costs. This pressure is strongest in the propionic acid and formic acid lines, where margins are thinner and customers are often more price-sensitive. Large commercial dairies can absorb these moves more easily through longer supply contracts, but smaller operators often cut application rates or shift to lower-specification products when prices rise. European feed additive rules also limit downward reformulation because product specifications and purity standards must still be maintained during cost spikes. That combination slows adoption in price-sensitive regions and puts mid-scale manufacturers under more pressure in the silage additives market.

Other drivers and restraints analyzed in the detailed report include:

- Feed Shrink and Dry Matter Loss Reduction Focus

- Shift Toward Biological Inoculants and Precision Fermentation

- Regulatory Approval and Labeling Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Inoculants held the largest share, accounting for 45.0% of the silage additives market share in 2025. Their lead came from broad use across corn, grass, and legume silage, along with a clear return on investment in intensive dairy and beef systems. Organic acids and salts are the fastest-growing additive type, registering 6.0% CAGR through 2026-2031, with buffered and blended acid preservatives gaining traction as producers shift away from neat formic acid products. This growth is tied to demand for safer, less corrosive formulations and to the need for flexible preservation tools in regions where inoculant handling and cold-chain reliability are less consistent.

Within the remaining segments of the silage additives market, combination inoculants are gaining premium demand because they pair rapid pH reduction with stronger aerobic stability at feedout. Homofermentative inoculants continue to serve simpler ensiling conditions, while heterofermentative products are seeing greater use in high-dry-matter corn systems where heating risks are high. Enzymes, fermentation and spoilage control additives, and adsorbents are also expanding their role as farms place more emphasis on fiber digestibility, mold control, and mycotoxin management. Other additive types, including sugar-based and nutrient-based products, remain niche but relevant in wet forage and legume silage programs, especially in the Asia-Pacific and Africa.

Complete Report Scope:

- Additive Type

- Inoculants

- Homofermentative

- Heterofermentative

- Combination Inoculants

- Organic Acids and Salts

- Formic Acid and Formates

- Propionic Acid and Propionates

- Lactic Acid and Lactates

- Buffered/Blended Acid Preservatives

- Enzymes

- Fiber-Digesting Enzymes

- Starch-Digesting Enzymes

- Multi-enzyme Blends

- Adsorbents

- Clay and Mineral Adsorbents

- Fiber and Grain Carriers

- Fermentation & Spoilage Control Additives

- Mold Inhibitors (Non-Acid Based)

- Aerobic Stability Enhancers

- Other Types

- Sugar-based Additives

- Nutrient-based Additives

- Inoculants

- Silage Type

- Grass Silage

- Cereals

- Corn

- Sorghum

- Oats

- Barley

- Other Cereal Silage

- Legumes

- Alfalfa

- Clover

- Other Legume Silage

- Mixed Forage Silage

- Other Specialty Silage

- Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- Turkey

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America held 34.5% of the silage additives market share in 2025, making it the largest regional market. The United States maintains this lead because corn silage systems are highly mechanized, and large dairies closely monitor feed performance. The United States Department of Agriculture reported milk production at 222.6 billion pounds in 2025 in the United States and a milking herd of 9.06 million head, which keeps silage volumes and additive demand high. Regional growth is reflecting mature penetration but continued value expansion through multi-strain products. Canada and Mexico add incremental demand as intensive dairy and beef operations expand and suppliers widen access to premium formulations.

Asia-Pacific is projected to record the fastest 7.0% CAGR during 2026-2031 in the silage additives market, with China and India providing most of the new demand. China's 2025 Feed-Saving Action Plan promotes the use of silage to reduce grain dependence, strengthening the case for preservation inputs across commercial livestock systems. South America is projected to grow, led by Brazil, while the Middle East and Africa are also seeing rising demand as commercial dairy operations expand in hot climates that increase the risk of aerobic spoilage.

Europe is set to grow at a descent CAGR during 2026-2031 in the silage additives market, with Germany, France, the United Kingdom, and the Netherlands leading the way. The region remains mature yet remains active because aerobic stability and certification standards shape buying decisions. Germany's Deutsche Landwirtschafts-Gesellschaft testing framework acts as a quality filter, rewarding suppliers that can continue to demonstrate efficacy under defined silage protocols. The 2024 hexamine ban forced reformulation across part of the regional portfolio, and ADDCON completed the move to hexamine-free KOFASIL LP and KOFASIL Ultra by November 2024. Russia remains a sizable silage market, but import access and local production constraints slow the adoption of premium products.

- Archer-Daniels-Midland Company

- BASF SE

- Alltech, Inc.

- Lallemand Inc.

- Volac International Limited

- Novonesis A/S

- Corteva, Inc.

- Kemin Industries, Inc.

- ADDCON GmbH

- H. Wilhelm Schaumann GmbH

- Agri-King, Inc.

- EW Nutrition

- Josera GmbH & Co. KG

- Nutreco N.V.

- Cargill, Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Intensifying dairy and beef productivity targets

- 4.2.2 Scaling industrial livestock and forage systems

- 4.2.3 Feed shrink and dry matter loss reduction focus

- 4.2.4 Shift toward biological inoculants and precision fermentation

- 4.2.5 Mycotoxin risk control in high-moisture silage

- 4.2.6 Faster bunker turnaround and early feedout needs

- 4.3 Market Restraints

- 4.3.1 Raw material and organic acid price volatility

- 4.3.2 Regulatory approval and labeling burden

- 4.3.3 Live-microbe storage and application sensitivity

- 4.3.4 Performance variability from forage heterogeneity

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 Additive Type

- 5.1.1 Inoculants

- 5.1.1.1 Homofermentative

- 5.1.1.2 Heterofermentative

- 5.1.1.3 Combination Inoculants

- 5.1.2 Organic Acids and Salts

- 5.1.2.1 Formic Acid and Formates

- 5.1.2.2 Propionic Acid and Propionates

- 5.1.2.3 Lactic Acid and Lactates

- 5.1.2.4 Buffered/Blended Acid Preservatives

- 5.1.3 Enzymes

- 5.1.3.1 Fiber-Digesting Enzymes

- 5.1.3.2 Starch-Digesting Enzymes

- 5.1.3.3 Multi-enzyme Blends

- 5.1.4 Adsorbents

- 5.1.4.1 Clay and Mineral Adsorbents

- 5.1.4.2 Fiber and Grain Carriers

- 5.1.5 Fermentation & Spoilage Control Additives

- 5.1.5.1 Mold Inhibitors (Non-Acid Based)

- 5.1.5.2 Aerobic Stability Enhancers

- 5.1.6 Other Types

- 5.1.6.1 Sugar-based Additives

- 5.1.6.2 Nutrient-based Additives

- 5.1.1 Inoculants

- 5.2 Silage Type

- 5.2.1 Grass Silage

- 5.2.2 Cereals

- 5.2.2.1 Corn

- 5.2.2.2 Sorghum

- 5.2.2.3 Oats

- 5.2.2.4 Barley

- 5.2.2.5 Other Cereal Silage

- 5.2.3 Legumes

- 5.2.3.1 Alfalfa

- 5.2.3.2 Clover

- 5.2.3.3 Other Legume Silage

- 5.2.4 Mixed Forage Silage

- 5.2.5 Other Specialty Silage

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Netherlands

- 5.3.3.7 Russia

- 5.3.3.8 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Australia

- 5.3.4.5 New Zealand

- 5.3.4.6 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Turkey

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Egypt

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Archer-Daniels-Midland Company

- 6.4.2 BASF SE

- 6.4.3 Alltech, Inc.

- 6.4.4 Lallemand Inc.

- 6.4.5 Volac International Limited

- 6.4.6 Novonesis A/S

- 6.4.7 Corteva, Inc.

- 6.4.8 Kemin Industries, Inc.

- 6.4.9 ADDCON GmbH

- 6.4.10 H. Wilhelm Schaumann GmbH

- 6.4.11 Agri-King, Inc.

- 6.4.12 EW Nutrition

- 6.4.13 Josera GmbH & Co. KG

- 6.4.14 Nutreco N.V.

- 6.4.15 Cargill, Incorporated

- 6.5 Market Opportunities and Future Outlook