PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072480

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072480

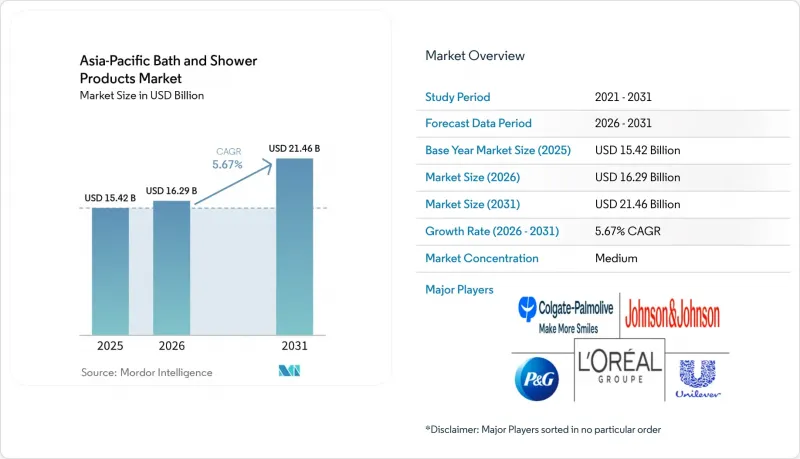

Asia-Pacific Bath and Shower Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, asia-Pacific bath & shower products market size in 2026 is estimated at USD 16.29 billion, growing from 2025 value of USD 15.42 billion with 2031 projections showing USD 21.46 billion, growing at 5.67% CAGR over 2026-2031.

This report is Segmented by Product Type (Bar Soap, Body Wash Shower/Gel, and Other Types), Category (Conventional and Organic), End-User (Kids/Children, and Adult), Distribution Channel (Supermarket/Hypermarket, Convenience/Grocery Stores, and More), and Geography (China, Japan, India, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Bath and Shower Products Market Trends and Insights

Innovation in Moisturizing and Exfoliating Products

Product innovation in moisturizing and exfoliating formulations is reshaping consumer expectations across Asia-Pacific markets. Unilever's March 2025 launch of Lifebuoy's Skin Solutions range exemplifies this trend, combining premium skincare benefits with traditional hygiene functions to capture consumers seeking multifunctional products. The convergence of skincare and body care categories is particularly pronounced in markets like Japan, where consumers increasingly demand concentrated care products that address specific skin concerns while maintaining cleansing efficacy. This trend is driving brands to invest in advanced formulation technologies that can deliver visible skin benefits beyond basic cleansing. The shift toward specialized products targeting different body parts and skin conditions is creating new market segments and premium pricing opportunities. Asian consumers' growing sophistication in ingredient awareness is pushing manufacturers to develop products with clinically proven benefits rather than relying solely on traditional marketing claims.

Demand for pH-Balanced, Sulfate-Free Products

Consumer awareness of harsh chemical ingredients is driving unprecedented demand for gentler formulations across the region. Research on palm-based surfactants indicates that sodium laureth sulfate alternatives and amino acid-based surfactants demonstrate lower cytotoxicity while maintaining effective cleansing properties . This scientific validation is particularly relevant in markets like Australia and Singapore, where consumers actively seek products that minimize skin irritation while delivering superior cleansing performance. The trend extends beyond premium segments, with mass-market brands reformulating existing products to eliminate sulfates and adjust pH levels to match skin's natural acidity. Regulatory frameworks in several ASEAN countries are beginning to recognize these formulation improvements, with some markets considering preferential treatment for products meeting specific mildness criteria. Growing demand for ASEAN Sensitive Skin Care products is encouraging brands to launch mild, pH-balanced bath and shower formulations. The shift toward sulfate-free formulations is creating supply chain challenges as manufacturers source alternative surfactants, but it's also opening opportunities for brands that can effectively communicate these benefits to increasingly educated consumers.

Concerns Over Chemicals and Allergens

Consumer anxiety over chemical ingredients is constraining market growth as safety-conscious buyers delay purchases or avoid certain product categories entirely. Indonesia's BPOM identified 16 cosmetic products containing hazardous ingredients including mercury, retinoic acid, hydroquinone, lead, and Red K10 dye in early 2025, highlighting persistent safety concerns that undermine consumer confidence. These safety violations create ripple effects across the market, as consumers become more cautious about product selection and demand greater transparency in ingredient disclosure. The challenge is particularly acute for brands operating across multiple APAC markets with varying regulatory standards and consumer awareness levels. Companies must invest significantly in reformulation, safety testing, and consumer education to address these concerns while maintaining product efficacy. The trend toward ingredient transparency is creating competitive advantages for brands that can clearly communicate product safety and ingredient sourcing, but it's also increasing operational complexity and costs across the supply chain.

Other drivers and restraints analyzed in the detailed report include:

- Natural and Organic Ingredient Demand

- Sustainability and Eco-friendly Packaging

- Presence of Counterfeit Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Body wash and shower gel products captured 34.22% market share in 2025 while simultaneously achieving the fastest growth at 5.74% CAGR through 2031, reflecting consumer migration from traditional bar soaps toward liquid formulations. This dual leadership position underscores how liquid formats better accommodate modern formulation innovations like pH-balancing, sulfate-free surfactants, and specialized moisturizing ingredients that consumers increasingly demand. Bar soap maintains significant presence despite declining relative share, particularly in price-sensitive markets and rural areas where traditional cleansing preferences persist. The "Other Product Types" segment, encompassing body scrubs, exfoliators, bath salts, and shower oils, represents the most dynamic category as brands expand beyond basic cleansing to offer specialized treatments targeting specific skin concerns and wellness experiences.

The product type evolution reflects deeper changes in consumer behavior, particularly in developed APAC markets where bathing rituals are becoming more elaborate and wellness-focused. Japan's soap market demonstrates this transition, with solid soap gaining renewed interest for concentrated care and natural ingredients, while liquid formats dominate urban areas seeking convenience and advanced formulations. Innovation in moisturizing and exfoliating products is creating new subcategories within each format, as brands like Unilever introduce hybrid products that combine traditional hygiene functions with premium skincare benefits. This trend toward multifunctional products is reshaping traditional product boundaries and creating opportunities for brands that can effectively communicate enhanced benefits while maintaining competitive pricing across diverse APAC markets with varying consumer sophistication levels.

The organic segment's 6.22% CAGR significantly outpaces conventional products despite the latter maintaining 67.15% market share in 2025, indicating a fundamental shift in consumer preferences toward natural formulations. This growth differential suggests that organic products are capturing an increasing share of new market entrants and category switchers, particularly among younger demographics and urban consumers with higher disposable incomes. Conventional products retain dominance through established distribution networks, competitive pricing, and brand loyalty, but face mounting pressure to reformulate with cleaner ingredients and sustainable packaging to remain competitive.

Consumer research demonstrates that packaging materials and certification labels strongly influence perceived naturalness and quality, creating competitive advantages for organic brands that invest in authentic sustainability credentials. The Body Shop's Community Fair Trade program, spanning 18 groups across 14 countries, exemplifies how organic brands are building authentic supply chain stories that resonate with environmentally conscious consumers. Regulatory harmonization through the ASEAN Cosmetic Directive is facilitating organic product market entry by standardizing certification requirements across member countries. The challenge for conventional brands lies in transitioning toward cleaner formulations while maintaining cost competitiveness and product performance standards that consumers expect from established brands.

Complete Report Scope:

- By Product Type

- Bar Soap

- Body Wash/ShowerGel

- Other Product Types

- By Category

- Conventional

- Organic

- By End-User

- Kids/Children

- Adult

- By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

- By Geography

- China

- India

- Japan

- Australia

- New Zealand

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- Reckitt Benckiser Group PLC

- Unilever

- Johnson & Johnson

- Beiersdorf AG

- Kao Corporation

- Godrej Consumer Products Limited

- Colgate-Palmolive Company

- Plum Island Soap Co.

- Amorepacific Corporation

- LG H&H Co., Ltd.

- Procter & Gamble

- Dabur India Ltd

- Marico Limited

- L'Oreal S.A.

- Emami Limited

- Shiseido Company, Limited

- L'Occitane International S.A.

- Innisfree Corporation

- Tata Consumer Products Limited

- The Estee Lauder Companies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Innovation in Moisturizing and Exfoliating Products

- 4.2.2 Demand for pH-Balanced, Sulfate-Free Products

- 4.2.3 Natural and Organic Ingredient Demand

- 4.2.4 Sustainability and Eco-friendly Packaging

- 4.2.5 Influence of Social Media and Celebrity Endorsement

- 4.2.6 Expansion of E-commerce Channels

- 4.3 Market Restraints

- 4.3.1 Concerns Over Chemicals and Allergens

- 4.3.2 Presence of Counterfeit Products

- 4.3.3 Frequent Brand Switching Behavior

- 4.3.4 Regulatory Ingredient Restrictions

- 4.4 Consumer Demand Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Bar Soap

- 5.1.2 Body Wash/ShowerGel

- 5.1.3 Other Product Types

- 5.2 By Category

- 5.2.1 Conventional

- 5.2.2 Organic

- 5.3 By End-User

- 5.3.1 Kids/Children

- 5.3.2 Adult

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Convenience/Grocery Stores

- 5.4.3 Online Retail Stores

- 5.4.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 China

- 5.5.2 India

- 5.5.3 Japan

- 5.5.4 Australia

- 5.5.5 New Zealand

- 5.5.6 South Korea

- 5.5.7 Thailand

- 5.5.8 Singapore

- 5.5.9 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Reckitt Benckiser Group PLC

- 6.4.2 Unilever

- 6.4.3 Johnson & Johnson

- 6.4.4 Beiersdorf AG

- 6.4.5 Kao Corporation

- 6.4.6 Godrej Consumer Products Limited

- 6.4.7 Colgate-Palmolive Company

- 6.4.8 Plum Island Soap Co.

- 6.4.9 Amorepacific Corporation

- 6.4.10 LG H&H Co., Ltd.

- 6.4.11 Procter & Gamble

- 6.4.12 Dabur India Ltd

- 6.4.13 Marico Limited

- 6.4.14 L'Oreal S.A.

- 6.4.15 Emami Limited

- 6.4.16 Shiseido Company, Limited

- 6.4.17 L'Occitane International S.A.

- 6.4.18 Innisfree Corporation

- 6.4.19 Tata Consumer Products Limited

- 6.4.20 The Estee Lauder Companies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK