PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072543

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072543

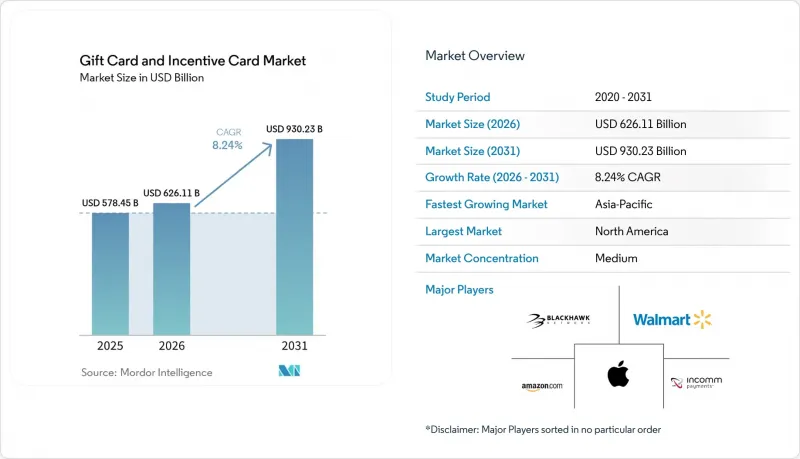

Gift Card and Incentive Card - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the gift card and incentive card market size is projected to expand from USD 578.45 billion in 2025 and USD 626.11 billion in 2026 to USD 930.23 billion by 2031, registering a CAGR of 8.24% between 2026 to 2031.

This report is Segmented by Card Type (Open-Loop Card and Closed-Loop Card), Format Type (Digital Card and Physical Card), Consumer Type (Individual (B2C) and Corporate (B2B)), Distribution Channel (Online and Offline), Industry of Application (Food and Beverages, and More), and by Region (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Gift Card and Incentive Card Market Trends and Insights

E-Commerce Boom Accelerating Digital Gift-Card Adoption

Online retail captured 27% of U.S. holiday purchases in the 2025 season, climbing 7.8% year-over-year, as consumers leveraged early promotions and mobile-first checkout flows that embed gift-card funding directly into cart workflows[2]. Digital gift cards now command over 50% of total unit sales globally, reversing the dominance of physical formats for the first time, with Millennials showing 70% preference for instant-delivery e-gifts that bypass postal latency. The presence of gift balances within wallets further shortens time-to-first redemption as consumers no longer need to keep or handle physical cards. Online payment studies also show broad wallet linking by cardholders, a shift that helps new digital gift issuers meet consumers at their preferred payment method during peak seasons.

Rise of Corporate Loyalty & Incentive Programs

Corporate gift-card allocations account for 30% of program budgets in North America and 34% in Europe, with 70% of North American firms anticipating moderate-to-significant increases in 2026 usage as enterprises shift from cash bonuses to prepaid instruments that avoid payroll-tax triggers and deliver instant digital deployment. The average North American B2B gift-card denomination climbed to USD 193 in 2025, up from USD 142 the prior year, as channel incentive programs targeting sales teams favor higher-value cards to reward quarterly quotas. API-first platforms plug into HR and CRM systems to trigger reward issuance automatically upon defined milestones, which cuts manual processing and speeds delivery at scale. Consolidation activity in 2024 also strengthened API catalogs and enterprise reach, improving coverage across brands and payout options for corporate-led programs.

Escalating Gift-Card Fraud & Cyber-Crime

Total reported fraud losses grew strongly in 2024, and gift cards remain a common vector for scammers where the payment method is specified. The Federal Trade Commission data shows increased losses and a large share of impostor-scam activity, which places pressure on issuers and retailers to enhance consumer education and in-store controls. Platforms deploy advanced threat intelligence and apply AI to detect anomalies, while tokenization replaces sensitive data across a growing share of transactions. Technology vendors also highlight the mechanics of account takeover and code harvesting, recommending secure packaging and monitoring to reduce draining schemes. New rules coming into effect in 2026 mandate reasonable procedures for fraud prevention at retail, which will further institutionalize best practices for staff training and point-of-sale safeguards. These measures converge with online security standards to strengthen the consumer protection baseline across channels.

Other drivers and restraints analyzed in the detailed report include:

- Cashless-Payment Ecosystems & Digital Wallets Proliferation

- AI-Driven Personalization Improving Breakage Economics

- Rising Open-Loop Activation & Interchange Fees for SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Closed-loop cards held 63.96% in 2025, while open-loop options are projected to grow faster at 9.77% CAGR through 2031 as acceptance breadth attracts corporate and cross-merchant use. The largest retailers continue to prefer closed-loop cards to retain margin and data visibility, but open-loop networks widen coverage through partnerships and real-time authorization improvements that reduce funding delays. Network acceptance growth among major card brands increases the utility of open-loop prepaid gift cards in domestic and cross-border contexts, lifting buyer confidence in universal redemption. An API that supports on-demand issuance and loading enables program managers to align card types to use cases, from highly targeted offers in closed ecosystems to general-purpose rewards that spend anywhere. This flexibility sustains a bifurcated structure in the gift card and incentive cards market as large retailers continue to lean on proprietary programs while enterprise buyers diversify into open-loop for broad acceptance.

Open-loop programs also benefit from security advances such as tokenization and risk-scoring tools at authorization, which reduce false positives and fraud risk on prepaid flows. On the closed-loop side, network exclusions lessen regulatory overhead and give issuers freedom to design product features that reinforce loyalty, app adoption, and reload behaviors. Aggregators support both models by adding packaging safeguards and encryption for activation flows that mitigate card-draining schemes at retail as more brands layer QR codes and wallets into issuance, open-loop and closed-loop formats converge on instant digital experiences that replace plastic as the default. The net effect is a gradual expansion of open-loop share, though closed-loop scale remains resilient where mobile ordering, loyalty integrations, and breakage economics favor proprietary ecosystems.

Physical cards held a 56.61% share in 2025, and digital formats are projected to grow at a 13.45% CAGR as issuance, delivery, and redemption consolidate in mobile workflows. Digital balances accessed through wallets eliminate the need to handle plastic, which accelerates first-use timing and reduces the chance of loss or damage. Top digital programs now integrate personalization features from SMS delivery to scheduled gifting and video messages, which expand engagement beyond holidays into everyday occasions. Retailers and restaurants that moved to digital gifts report significant reductions in single-use plastic, aligning with sustainability commitments and packaging regulations that favor dematerialization. Wallet ubiquity also lowers friction at the physical point of sale because balances are ready for tap-to-pay alongside cards and loyalty IDs.

Physical cards maintain relevance when presentation matters, such as corporate events or occasions where a tangible token adds perceived value. Merchants mitigate fraud risks on physical units with secure packaging and clearer tamper indicators while adding QR-based activation that links to immediate digital use. Hybrid formats that blend greeting cards with scannable codes bridge sentiment and instant redemption, widening appeal to senders preferring a physical artifact with digital convenience. As environmental standards tighten and network targets phase out first-use PVC, dematerialized formats gain a structural cost and compliance advantage. This creates room for faster innovation cycles in the gift card and incentive cards market as issuers iterate digital features without retooling physical supply chains.

Complete Report Scope:

- By Card Type

- Open-Loop Card

- Closed-Loop Card

- By Format Type

- Digital Card

- Physical Card

- By Consumer Type

- Individual (B2C)

- Corporate (B2B)

- By Distribution Channel

- Online

- Offline

- By Industry of Application

- Food and Beverages

- Health, Wellness, and Beauty

- Apparel, Footwear, and Accessories

- Consumer Electronics

- Other Industries

- By Region

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Benelux (Belgium, Netherlands, and Luxembourg)

- Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Geography Analysis

North America held 40.06% in 2025, with the United States providing a large base of consumers and enterprises using gift value across retail and dining. Consumer payments surveys show wallet linking rising among both debit and credit holders, and mobile payments are increasing their share of point-of-sale transactions compared to the prior year. State-level policy actions increase focus on secure packaging and fraud-prevention expectations for retailers, which shape implementation timelines and cost models for physical programs. Corporate incentive outlooks signal larger budgets in 2026, pointing to continued B2B scaling as companies automate issuance flows into employee and channel programs. Acceptance expansion among networks also improves the practicality of open-loop prepaid for cross-merchant use, complementing the large footprint of closed-loop leaders.

Asia-Pacific leads growth at a projected 10.23% CAGR, supported by interoperable real-time payment systems and high mobile wallet penetration. In India, program managers launched intelligent gift-card platforms with configurable discounts and product scoping, reducing time-to-personalization and aligning issuance to local consumer behavior. Network acceptance continues to widen in Japan and other markets, which raises utility for open-loop products in face-to-face and online flows. As wallet ecosystems become the default for transit, retail, and services, digital gift storage and redemption become native behaviors. These patterns align Asia-Pacific to higher digital growth for the gift card and incentive cards market, with corporate and consumer demand converging on mobile use cases.

Europe shows steady expansion amid increasing environmental standards and data protection obligations that shape program design. Producer responsibility and packaging content rules tighten, which supports paper substrates and digital format adoption among issuers seeking to reduce plastic content. In employee benefits, a 2024 spin-off added capital flexibility and acquisition optionality, enabling growth in digital-native benefits platforms across Spain and Mexico while sustaining core European markets. Central and Eastern Europe sees closed-loop hybrids progressing as mall operators and retail networks adopt data-rich gift platforms that favor local commerce and on-premise redemption. As wallet coverage grows and network acceptance expands, open-loop utility increases, but closed-loop programs continue to anchor merchant loyalty strategies across key countries.

- Amazon.com Inc.

- Apple Inc.

- Walmart Inc.

- Blackhawk Network Holdings Inc.

- InComm Payments

- PayPal Holdings Inc.

- Visa Inc.

- Mastercard Inc.

- American Express Co.

- Sodexo SA

- Carrefour SA

- Auchan Group SA

- Aldi Group

- Starbucks Corp.

- Target Corp.

- Givex Corp.

- Swile

- WeGift

- GiftCloud

- Paytronix Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce boom accelerating digital gift-card adoption

- 4.2.2 Rise of corporate loyalty & incentive programs

- 4.2.3 Cashless-payment ecosystems & digital wallets proliferation

- 4.2.4 AI-driven personalization improving breakage economics

- 4.2.5 Sustainability push favouring dematerialised gift cards

- 4.2.6 Blockchain-secured, cross-border gift-card platforms

- 4.3 Market Restraints

- 4.3.1 Escalating gift-card fraud & cyber-crime

- 4.3.2 Divergent global fee / expiry regulations

- 4.3.3 Rising open-loop activation & interchange fees for SMEs

- 4.3.4 Tariff-driven cost spikes in plastic card supply chains

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Card Type

- 5.1.1 Open-Loop Card

- 5.1.2 Closed-Loop Card

- 5.2 By Format Type

- 5.2.1 Digital Card

- 5.2.2 Physical Card

- 5.3 By Consumer Type

- 5.3.1 Individual (B2C)

- 5.3.2 Corporate (B2B)

- 5.4 By Distribution Channel

- 5.4.1 Online

- 5.4.2 Offline

- 5.5 By Industry of Application

- 5.5.1 Food and Beverages

- 5.5.2 Health, Wellness, and Beauty

- 5.5.3 Apparel, Footwear, and Accessories

- 5.5.4 Consumer Electronics

- 5.5.5 Other Industries

- 5.6 By Region

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Colombia

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Benelux (Belgium, Netherlands, and Luxembourg)

- 5.6.3.7 Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines)

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Amazon.com Inc.

- 6.4.2 Apple Inc.

- 6.4.3 Walmart Inc.

- 6.4.4 Blackhawk Network Holdings Inc.

- 6.4.5 InComm Payments

- 6.4.6 PayPal Holdings Inc.

- 6.4.7 Visa Inc.

- 6.4.8 Mastercard Inc.

- 6.4.9 American Express Co.

- 6.4.10 Sodexo SA

- 6.4.11 Carrefour SA

- 6.4.12 Auchan Group SA

- 6.4.13 Aldi Group

- 6.4.14 Starbucks Corp.

- 6.4.15 Target Corp.

- 6.4.16 Givex Corp.

- 6.4.17 Swile

- 6.4.18 WeGift

- 6.4.19 GiftCloud

- 6.4.20 Paytronix Systems Inc.

7 Market Opportunities & Future Outlook

- 7.1 Embedding gift and incentive cards in omni-channel loyalty and cross-sector promotional strategies

- 7.2 Build or license scalable API solutions to enable partners and merchants to issue, manage, and track gift/incentive cards efficiently at scale