PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072638

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072638

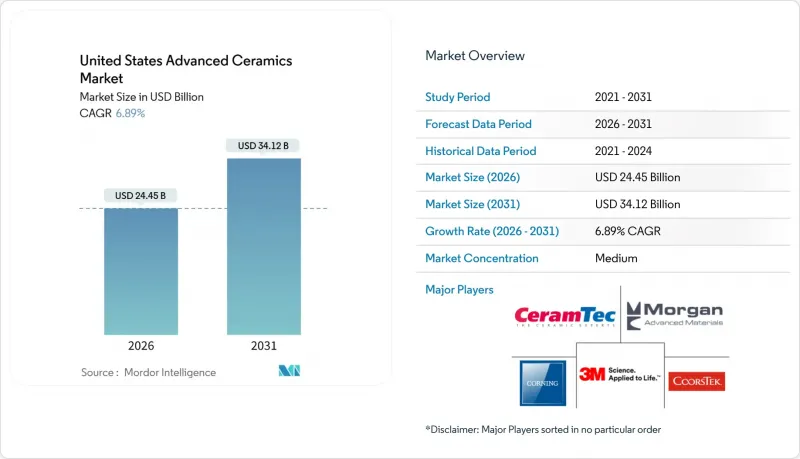

United States Advanced Ceramics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states advanced ceramics market size is estimated at USD 24.45 billion in 2026, and is expected to reach USD 34.12 billion by 2031, at a CAGR of 6.89% during the forecast period (2026-2031).

This report is Segmented by Material Type (Alumina, Titanate, Zirconia, Silicon Carbide, and Other Types), Class Type (Monolithic Ceramics, Ceramic Matrix Composites, and Ceramic Coatings), and End-User Industry (Electrical and Electronics, Automotive and Transportation, Industrial, Chemicals, Medical, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

United States Advanced Ceramics Market Trends and Insights

Strong Demand from Aerospace and Defense

In 2024, the Pentagon inked MACH contracts, pushing the boundaries of ceramic matrix composite (CMC) procurement. These contracts target operations at extreme temperatures, surpassing the limits of nickel superalloys. The Army's Extended Range Cannon Artillery project is leading the charge, specifying silicon-carbide liners that extend barrel life. This move is accelerating the adoption of reaction-bonded SiC components. Meanwhile, in the commercial aerospace arena, GE Aerospace's RISE demonstrator is leveraging CMC shrouds, achieving significant weight reduction per aircraft and translating to fuel savings. Further underscoring the military's commitment, a grant under the Defense Production Act Title III was announced in March 2025. This initiative aims to repatriate a portion of the military's ceramic supply, reducing dependence on foreign sources. Together, these initiatives are not only driving demand for advanced ceramics into mainstream production but also providing suppliers with a clearer, multiyear outlook.

Electronics and Semiconductor Miniaturization Surge

As logic scales down to 2-nanometer nodes and high-bandwidth memory stacks, ceramic consumption per chip package rises. Intel's Ohio megasite, set to commence volume production in late 2026, is projected to consume significant amounts of alumina substrates annually. The National Advanced Packaging Manufacturing Program is co-funding glass-ceramic interposers, which reduce signal loss at frequencies above 100 GHz. This advancement paves the way for chiplet architectures in AI accelerators. Presently, a single high-end accelerator boasts numerous multilayer ceramic capacitors, each handling transient currents at high levels, a significant increase from 2020 figures. Given that sub-micron delaminations can lead to latent field failures, there's a growing reliance on inspection regimes utilizing automated optical and computed-tomography systems. This surge in electronics not only fuels immediate volume growth but also drives up average selling prices for high-purity powders and substrate blanks.

High Production and Machining Costs

Precision grinding with diamond tools incurs significant costs for material removal. This cost escalates for intricate geometries, especially when metal alloys are used. While ceramic turbocharger rotors offer efficiency benefits, they come with a premium over their nickel-based counterparts. This price difference confines their use to high-end vehicle trims. Producers face yield losses due to shrinkage variability. To counter this, they oversize green bodies and then machine them back to the desired tolerance, a process that extends production time. Although binder-jetting can significantly reduce the need for this secondary machining, the high cost of alumina and silicon-carbide powders hinders their widespread adoption for industrial parts. The cost challenges are expected to diminish as powder synthesis techniques advance and hybrid manufacturing processes become more refined.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Deployment of 5G and Power-Electronics Infrastructure

- Federal Funding for Hypersonic and Space Programs

- Brittleness and Design-Flexibility Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Alumina accounted for 41.46% of the advanced ceramics market share in 2025, thanks to its cost-performance ratio, making it ideal for semiconductor chambers, ballistic armor, and wear-resistant plant components. As demand for EV inverters grows, the need for substrates with high heat dissipation capabilities has surged, propelling Wolfspeed to achieve substantial substrate revenue in fiscal 2025. Titanate-based dielectrics, though smaller in tonnage, are advancing at a 7.82% CAGR through 2031, powered by the densification of 5G base stations and automotive radar modules that need high-permittivity capacitors.

Under the tightening regulations of ISO 6474-2:2024, there's a new mandate for granular traceability in medical-grade alumina. This has led to a spike in compliance costs, particularly burdening smaller mills. Meanwhile, the emergence of binder-jettable silicon-nitride powders is revolutionizing the industry. These innovations are significantly reducing turbine-component lead times and achieving a notable reduction in material waste. Life-cycle assessments highlight the advantages of silicon-carbide pump seals, which are extending the mean time between failures in corrosive environments. This significant enhancement justifies the premium on material costs. As designers increasingly prioritize uptime and miniaturization, it's anticipated that while alumina will maintain its foothold in commodity substrates, its market share will wane post-2028, giving way to the rising volumes of titanate and silicon-carbide.

Complete Report Scope:

- By Material Type

- Alumina

- Titanate

- Zirconia

- Silicon Carbide

- Other Material Types

- By Class Type

- Monolithic Ceramics

- Ceramic Matrix Composites

- Ceramic Coatings

- By End-user Industry

- Electrical and Electronics

- Automotive and Transportation

- Industrial

- Chemicals

- Medical

- Other End-user Industries

List of Companies Covered in this Report:

- 3M

- Blasch Precision Ceramics, Inc.

- CeramTec GmbH

- CoorsTek Inc.

- Corning Incorporated

- Elan Technology

- Ferrotec Corporation

- KYOCERA Corporation

- Materion Corporation

- Morgan Advanced Materials

- Saint-Gobain

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strong Demand from Aerospace and Defense

- 4.2.2 Electronics and Semiconductor Miniaturization Surge

- 4.2.3 Rapid Deployment of 5G and Power-Electronics Infrastructure

- 4.2.4 Federal Funding for Hypersonic and Space Programs

- 4.2.5 Additive Manufacturing Adoption Reducing Lead-Times

- 4.3 Market Restraints

- 4.3.1 High Production and Machining Costs

- 4.3.2 Brittleness and Design-Flexibility Constraints

- 4.3.3 Critical Mineral Supply-Chain Vulnerability

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products and Services

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Alumina

- 5.1.2 Titanate

- 5.1.3 Zirconia

- 5.1.4 Silicon Carbide

- 5.1.5 Other Material Types

- 5.2 By Class Type

- 5.2.1 Monolithic Ceramics

- 5.2.2 Ceramic Matrix Composites

- 5.2.3 Ceramic Coatings

- 5.3 By End-user Industry

- 5.3.1 Electrical and Electronics

- 5.3.2 Automotive and Transportation

- 5.3.3 Industrial

- 5.3.4 Chemicals

- 5.3.5 Medical

- 5.3.6 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Blasch Precision Ceramics, Inc.

- 6.4.3 CeramTec GmbH

- 6.4.4 CoorsTek Inc.

- 6.4.5 Corning Incorporated

- 6.4.6 Elan Technology

- 6.4.7 Ferrotec Corporation

- 6.4.8 KYOCERA Corporation

- 6.4.9 Materion Corporation

- 6.4.10 Morgan Advanced Materials

- 6.4.11 Saint-Gobain

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment