PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072679

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072679

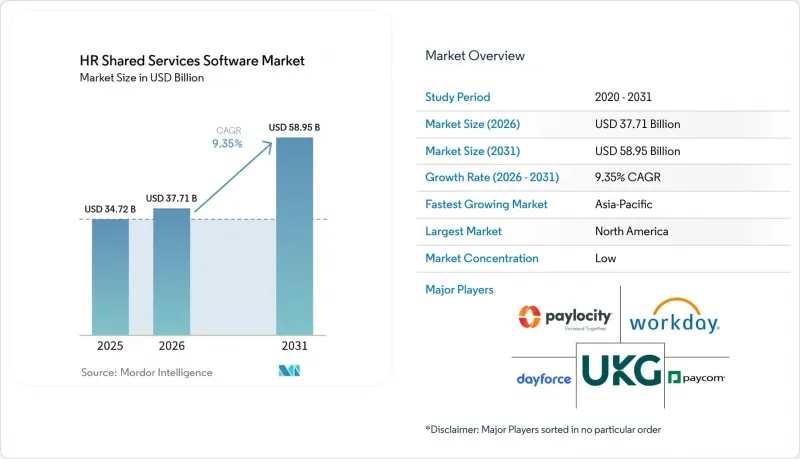

HR Shared Services Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the HR shared services software market size is expected to increase from USD 34.72 billion in 2025 to USD 37.71 billion in 2026 and reach USD 58.95 billion by 2031, growing at a CAGR of 9.35% over 2026-2031.

This report is Segmented by Deployment Model (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and More), Application (Core HR and Employee Self-Service; Case Management and Ticketing, and More), End-User Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global HR Shared Services Software Market Trends and Insights

AI-Enabled Case Resolution and Knowledge Retrieval Accelerates Tier-0 Deflection

The biggest shift in the HR shared services software market is the move from advisory AI to agentic AI that can resolve cases without human escalation. Oracle introduced Fusion Agentic Applications for HR in April 2026, using coordinated AI agents that can work across policy hierarchies, approval flows, and employee records to complete actions end to end. ServiceNow also extended its HRSD release in December 2025 with agentic flows that use retrieval-augmented generation for tier-0 queries and critical case routing. As deflection rates rise, the cost base of shared service centers falls, allowing more HR staff to shift into employee relations and advisory work. That is lifting the ROI bar in the HR shared services software market for platforms that cannot prove case resolution at scale.

Expansion of Employee Self-Service Expectations Reshapes Platform Architecture

Employee expectations in HR shared services have evolved dramatically. By 2026, employees want far more than simple password resets or pay-stub downloads; they expect portals to handle complex multi-step requests, such as recalculating leave after maternity return, confirming equity grants during role changes, and updating benefits after life events, without HR desk intervention. Microsoft highlighted this shift with its Employee Self-Service Agent, built on Copilot, which unified HR, IT, and campus services into a single enterprise-wide experience, resulting in measurable ticket deflection. Enterprise HR-AI budgets surged to USD 1.6 million in 2026, a tenfold increase from 2023, driven by use cases such as onboarding automation, HR document creation, and AI-assisted workflows. Meanwhile, SHRM emphasized that frontline and deskless workers make up 80% of the global workforce, prompting vendors to prioritize mobile-first, biometric-authenticated, and SMS-accessible support layers rather than browser-only portals.

Data Privacy and Sensitive Employee Record Exposure Elevates Deployment Risk

HR shared services platforms consolidate salary, health, disciplinary, immigration, and performance data in a single system, which increases the risk profile of the HR shared services software market. That concentration creates both a larger attack surface and a more serious compliance burden for buyers. The CMS Law tracker recorded 191 employee-data fines totaling EUR 360,807,141 (USD 389.7 million), and the 2026 coordinated action from the EDPB has tightened attention on employer transparency. Italy's data protection authority also issued a warning in 2026 regarding a Slack-based stress-detection tool, citing a risk of future GDPR Article 9 violations even without a confirmed breach. As a result, procurement cycles in the HR shared services software market are taking longer, as legal, privacy, and security teams require ISO 27001, DPIA, and sub-processor evidence before signing contracts.

Other drivers and restraints analyzed in the detailed report include:

- Centralization of Multi-Country HR Operations Creates Demand For Unified Platforms

- Rising Compliance Burden Across Payroll, Leave, and Employee Documentation Drives Platform Adoption

- Integration Friction Across HRIS, Payroll, Identity, and Document Systems Delays Value Realization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment accounted for 66.12% of the HR shared services software market in 2025, making it the standard choice across enterprise HR operations. Enterprises continue to favor cloud because feature updates arrive faster there, especially for AI, automation, and agentic service tools. Hybrid deployment remains the fastest-growing model and is projected to grow at 11.75% through 2031. That pattern reflects a practical response to data-residency and audit needs rather than a retreat from cloud.

The HR shared services software market for hybrid deployment is projected to expand at a 11.75% CAGR through 2031 as organizations split workloads across cloud and on-premises environments. In regulated settings, payroll and identity data often stay in private infrastructure while service delivery, analytics, and AI capabilities move into cloud layers. This mix is becoming more common in sectors and countries where sensitive employee records cannot be fully migrated to public cloud environments. On-premise deployments continue to lose ground in new projects because legacy ERP links and long license cycles slow migration decisions. The result is a more mature HR shared services software market, where deployment choices are increasingly driven by workload sensitivity and governance needs.

Large enterprises accounted for 62.50% of 2025 revenue in the HR shared services software market. That lead reflects the scale economics of shared service centers, centralized SLA management, and multi-country payroll orchestration. These organizations can spread software spending across very large employee populations and many legal entities. They also place greater weight on multilingual support, depth of compliance, and breadth of workflow when selecting platforms.

Medium-sized enterprises are projected to grow at 12.31% CAGR through 2031, making them the fastest-growing buyer group in this segmentation. Cloud delivery and modular pricing are opening access to case management, document handling, and analytics for firms that previously could not justify the costs of enterprise-grade deployment. Many of these buyers are entering the HR shared services software market during their first acquisition or international expansion, which means they often have little legacy shared services infrastructure to unwind. That makes them attractive greenfield opportunities for incumbent and challenger vendors alike. ISG found that 84% of organizations planned to change their HR sourcing model within 2 years, with the expansion of internal shared services identified as a major lever

Complete Report Scope:

- By Deployment Model

- Cloud-Based

- On-Premise

- Hybrid

- By End User Enterprise Size

- Large Enterprises

- Medium-Sized Enterprises

- By Application

- Core HR and Employee Self-Service

- Case Management and Ticketing

- Workflow Automation and Employee Journeys

- Document Management and E-Signature

- Workforce Analytics and Reporting

- Payroll and Benefits Support

- Talent and Learning Support

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Information Technology and Telecom

- Retail and E-commerce

- Industrial Manufacturing

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 42.00% of the HR shared services software market in 2025, maintaining the region's lead. The region benefits from large enterprise budgets, mature shared service center models, and a dense software vendor base. Buying behavior also favors SaaS procurement and faster deployment of AI-led workflows in employee support. Many HR professionals in the US states with workforce-related AI laws were unaware of those rules, which helps explain why buyers want stronger compliance guardrails in their platforms. Canada adds another layer of complexity through province-level payroll and leave rules and bilingual workplace needs in Quebec, which supports demand for enterprise-grade systems.

Europe remained the second-largest regional market for HR shared services software. GDPR and the EU AI Act have raised the minimum standard for governance, auditability, and transparency across HR platforms used in the region. Coordinated enforcement actions have increased scrutiny of employer transparency obligations in employee data processing. Germany and the United Kingdom anchor regional demand, and the UK's holiday pay recordkeeping rules, effective April 6, 2026, created a near-term trigger for document management modules. South America remains smaller, but Brazil and Argentina are seeing increased interest from multinationals seeking compliant regional HR data platforms.

Asia-Pacific is projected to grow at 14.25% CAGR through 2031, the fastest regional pace in the HR shared services software market. Growth is being supported by India's expanding IT hiring base, the digitization of China's manufacturing workforce, and healthcare HR modernization across Southeast Asia. Surveys show that 75% of organizations in the region were already using AI in HR, and 63% expected AI budgets to rise in 2026, although only 11% felt fully prepared to scale AI across the enterprise. The Middle East, led by Saudi Arabia and the UAE, and parts of Africa, especially South Africa and Nigeria, remain earlier-stage opportunities tied to conglomerate expansion, multinational subsidiaries, and demand for compliance-ready HR infrastructure.

- Workday, Inc.

- UKG Inc.

- Dayforce, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- BambooHR LLC

- HiBob Ltd.

- Darwinbox Digital Solutions Private Limited

- Cezanne HR Limited

- Neocase Software

- Rippling People Center Inc.

- Factorial HR, S.L.

- SAP SuccessFactors

- Zalaris ASA

- Ramco Systems Limited

- Servicenow

- Deel Inc.

- PayFit SAS

- Paychex, Inc.

- Neocase Software

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Expansion Of Employee Self-Service Expectations

- 4.3.2 AI-Enabled Case Resolution And Knowledge Retrieval

- 4.3.3 Centralization Of Multi-Country HR Operations

- 4.3.4 Rising Compliance Burden Across Payroll, Leave, And Employee Documentation

- 4.3.5 Cross-Functional Workflow Automation For Joiner-Mover-Leaver Journeys

- 4.3.6 Demand For Multilingual Shared-Service Support After Mergers And Acquisitions

- 4.4 Market Restraints

- 4.4.1 Data Privacy And Sensitive Employee Record Exposure

- 4.4.2 Integration Friction Across HRIS, Payroll, Identity, And Document Systems

- 4.4.3 Weak Process Ownership And Poor Data Harmonization Limit ROI

- 4.4.4 Governance Risk From Agentic AI In High-Stakes HR Decisions

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By End User Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Medium-Sized Enterprises

- 5.3 By Application

- 5.3.1 Core HR and Employee Self-Service

- 5.3.2 Case Management and Ticketing

- 5.3.3 Workflow Automation and Employee Journeys

- 5.3.4 Document Management and E-Signature

- 5.3.5 Workforce Analytics and Reporting

- 5.3.6 Payroll and Benefits Support

- 5.3.7 Talent and Learning Support

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Information Technology and Telecom

- 5.4.4 Retail and E-commerce

- 5.4.5 Industrial Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday, Inc.

- 6.4.2 UKG Inc.

- 6.4.3 Dayforce, Inc.

- 6.4.4 Paycom Software, Inc.

- 6.4.5 Paylocity Holding Corporation

- 6.4.6 BambooHR LLC

- 6.4.7 HiBob Ltd.

- 6.4.8 Darwinbox Digital Solutions Private Limited

- 6.4.9 Cezanne HR Limited

- 6.4.10 Neocase Software

- 6.4.11 Rippling People Center Inc.

- 6.4.12 Factorial HR, S.L.

- 6.4.13 SAP SuccessFactors

- 6.4.14 Zalaris ASA

- 6.4.15 Ramco Systems Limited

- 6.4.16 Servicenow

- 6.4.17 Deel Inc.

- 6.4.18 PayFit SAS

- 6.4.19 Paychex, Inc.

- 6.4.20 Neocase Software

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment