PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072695

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072695

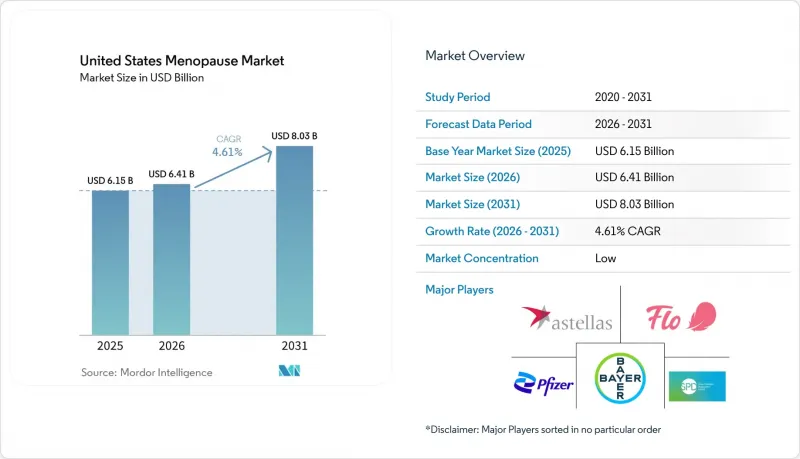

United States Menopause - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united states menopause market size is expected to increase from USD 6.15 billion in 2025 to USD 6.41 billion in 2026 and reach USD 8.03 billion by 2031, growing at a CAGR of 4.61% over 2026-2031.

This report is Segmented by Treatment Type (Prescription Hormonal, Non-Hormonal, Dietary Supplements & OTC), Symptom Focus (Vasomotor, GSM, Sleep & Mood, Bone & Sexual Health), Route of Administration (Oral, Transdermal/Topical, Vaginal, Injectable), and Distribution Channel (Retail Pharmacies, Online/DTC, Hospital Pharmacies, Specialty Clinics). Market Forecasts are Provided in Terms of Value (USD).

United States Menopause Market Trends and Insights

Large Symptomatic Female Cohort Entering Menopause

The United States menopause market is supported by a dense demographic wave as later Baby Boomers and early Generation X women move through menopause at the same time. The country adds nearly 1.3 million new menopause entrants each year, which keeps the care pool expanding even when broader health spending becomes cautious. This population is entering menopause with greater familiarity with digital care tools and with a stronger willingness to ask for treatment instead of accepting symptoms without support. That combination raises the likelihood of multi-modal care, including supplements, prescriptions, and virtual consultations, rather than one-time symptom management. The result is a durable demand base for the United States menopause market that is tied more to population structure and symptom burden than to discretionary spending.

Rising Awareness and Destigmatization of Menopause Care

The United States menopause market is benefiting from a clear change in how menopause is discussed at work, in clinics, and across consumer health channels. Awareness is improving through employer education, women's health advocacy, and a broader media focus on symptoms that were often minimized in the past. The Society for Women's Health Research found that 64% of employees want menopause-related workplace benefits, which shows that treatment demand is now visible inside employer settings as well as in physician offices. This change is especially important in areas such as GSM, sleep disruption, and mood symptoms, where women often delay care or never raise the issue at all. The FDA's July 2025 expert panel added further legitimacy to active treatment by focusing directly on hormone therapy risk and benefit communication.

Legacy Hormone Therapy Safety Overhang

The United States menopause market still carries the effects of older hormone therapy risk perceptions, especially in general practice settings. A recent JAMA Internal Medicine reanalysis of Women's Health Initiative trial data showed that hormone therapy can offer a net cardiovascular benefit for women aged 50-59 with vasomotor symptoms when timing and age at initiation are considered. Even so, prescribing behavior remains uneven because not all clinicians interpret current evidence in the same way. The American Academy of Family Physicians published guidance in July 2025 that continued to frame menopausal hormone therapy as having limited benefits and significant harms, which shows that professional messaging still differs across care settings. This leaves many eligible women untreated or delayed in treatment, which slows the conversion of clinical demand into realized sales across the United States menopause market.

Other drivers and restraints analyzed in the detailed report include:

- Non-Hormonal Prescription Innovation

- Employer-Sponsored and Virtual Menopause Care

- Liver-Monitoring and Reimbursement Friction For NK-Targeted Therapies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dietary supplements & OTC support products held 84.87% of the United States menopause market share in 2025, which reflects the long-standing habit of self-directed symptom management through easily accessible products. Their reach is broad because these products are sold through retail pharmacies, grocery outlets, and direct online subscriptions, which gives them a visibility advantage that prescription therapies cannot match. This leadership position, however, does not mean the category is secure from disruption. Prescription non-hormonal therapies are projected to grow at a 5.06% CAGR through 2031, which points to a gradual but meaningful shift in the United States menopause market toward clinically guided treatment options.

That shift is visible in how prescription and OTC boundaries are starting to blur. Bonafide Health launched Thermella in September 2024 as an OTC NK3R antagonist supplement priced at USD 40-45 per month, using the same broad biological pathway that has attracted strong interest in prescription vasomotor care. Within hormonal prescriptions, companies with broad portfolios still hold an important place because they cover both systemic and local treatment needs. Pfizer's menopause hormone therapy portfolio includes Premarin, Prempro, Estring, Premarin Vaginal Cream, and Duavee, which gives it coverage across multiple patient profiles and symptom settings. Mayne Pharma also reported USD 178.4 million in FY2025 revenue from its women's health business, with strong growth from IMVEXXY and BIJUVA, supported in part by a more favorable regulatory tone toward local estrogen therapies.

Vasomotor symptoms accounted for 53.83% of the United States menopause market size in 2025, which reflects how hot flashes and night sweats remain the main triggers for women to seek treatment. The leading drug launches in recent years have centered on this symptom group, and that focus has reinforced both physician attention and commercial investment. The approval of newer NK-targeted therapies has strengthened the prescription pathway for women who want relief without hormone use or who cannot take hormone therapy. That said, the United States menopause market is not staying limited to vasomotor care alone, because untreated symptoms in other categories are now drawing more clinical focus.

Genitourinary syndrome of menopause is forecast to expand at a 6.12% CAGR through 2031, making it the fastest-growing symptom segment in the United States menopause market. This growth reflects better recognition of GSM as a chronic and progressive condition rather than a narrow or optional quality-of-life issue. The segment had been held back by patient reluctance to discuss vaginal symptoms and by uneven provider familiarity with diagnosis and long-term management. Growth is also being supported by local estrogen options and by broader awareness that menopause care often requires treatment across multiple symptom clusters rather than in one isolated complaint. Sleep and mood symptoms could also become more commercially important if ongoing work around elinzanetant confirms benefits beyond vasomotor control, because that would widen the practical treatment scope for a single prescription class.

Complete Report Scope:

- By Treatment Type

- Prescription Hormone Therapies

- Systemic Estrogen-Only Therapies

- Estrogen-Progestogen Combination Therapies

- Local Vaginal Estrogen Therapies

- Prescription Non-Hormonal Therapies

- NK-Targeted Therapies

- SSRI / SNRI and Other Symptom-Targeted Prescriptions

- SERM and Other Non-Estrogen Therapies

- Dietary Supplements & OTC Support Products

- Prescription Hormone Therapies

- By Primary Symptom Focus

- Vasomotor Symptoms

- Genitourinary Syndrome of Menopause

- Sleep and Mood Symptoms

- Bone, Sexual Health, and Healthy Aging Support

- By Route of Administration

- Oral

- Transdermal / Topical

- Vaginal

- Injectable / Other

- By Distribution Channel

- Retail Pharmacies & Drugstores

- Online Pharmacies & Direct-to-Consumer

- Hospital / Health-System Pharmacies

- Specialty Clinics & Virtual Menopause Platforms

List of Companies Covered in this Report:

- Alloy, Inc.

- Astellas Pharma

- Bayer

- Bonafide Health, LLC

- Duchesnay USA Inc.

- Elektra Health

- Estroven (i-Health, Inc.)

- Evernow

- Flo Health Inc.

- Gennev

- Kindra

- Lisa Health

- Mayne Pharma

- MenoLabs (Dr. Reddy's Laboratories Ltd.)

- Midi Health

- O Positiv Health

- Padagis LLC

- Pfizer

- SPD Swiss Precision Diagnostics GmbH (Clearblue)

- Womaness

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Large Symptomatic Female Cohort Entering Menopause

- 4.2.2 Rising Awareness and Destigmatization of Menopause Care

- 4.2.3 Non-Hormonal Prescription Innovation

- 4.2.4 Preference For Hormone-Free and Natural Symptom Relief

- 4.2.5 Large Untreated Population with Conversion Runway

- 4.2.6 Employer-Sponsored and Virtual Menopause Care

- 4.3 Market Restraints

- 4.3.1 Legacy Hormone-Therapy Safety Overhang

- 4.3.2 Stringent Evidence and Regulatory Burden

- 4.3.3 Liver-Monitoring and Reimbursement Friction For NK-Targeted Therapies

- 4.3.4 Import-Cost Pressure on Hormone Formulations

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Treatment Type

- 5.1.1 Prescription Hormone Therapies

- 5.1.1.1 Systemic Estrogen-Only Therapies

- 5.1.1.2 Estrogen-Progestogen Combination Therapies

- 5.1.1.3 Local Vaginal Estrogen Therapies

- 5.1.2 Prescription Non-Hormonal Therapies

- 5.1.2.1 NK-Targeted Therapies

- 5.1.2.2 SSRI / SNRI and Other Symptom-Targeted Prescriptions

- 5.1.2.3 SERM and Other Non-Estrogen Therapies

- 5.1.3 Dietary Supplements & OTC Support Products

- 5.1.1 Prescription Hormone Therapies

- 5.2 By Primary Symptom Focus

- 5.2.1 Vasomotor Symptoms

- 5.2.2 Genitourinary Syndrome of Menopause

- 5.2.3 Sleep and Mood Symptoms

- 5.2.4 Bone, Sexual Health, and Healthy Aging Support

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Transdermal / Topical

- 5.3.3 Vaginal

- 5.3.4 Injectable / Other

- 5.4 By Distribution Channel

- 5.4.1 Retail Pharmacies & Drugstores

- 5.4.2 Online Pharmacies & Direct-to-Consumer

- 5.4.3 Hospital / Health-System Pharmacies

- 5.4.4 Specialty Clinics & Virtual Menopause Platforms

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Alloy, Inc.

- 6.3.2 Astellas Pharma Inc.

- 6.3.3 Bayer AG

- 6.3.4 Bonafide Health, LLC

- 6.3.5 Duchesnay USA Inc.

- 6.3.6 Elektra Health

- 6.3.7 Estroven (i-Health, Inc.)

- 6.3.8 Evernow

- 6.3.9 Flo Health Inc.

- 6.3.10 Gennev

- 6.3.11 Kindra

- 6.3.12 Lisa Health

- 6.3.13 Mayne Pharma Group Limited

- 6.3.14 MenoLabs (Dr. Reddy's Laboratories Ltd.)

- 6.3.15 Midi Health

- 6.3.16 O Positiv Health

- 6.3.17 Padagis LLC

- 6.3.18 Pfizer Inc.

- 6.3.19 SPD Swiss Precision Diagnostics GmbH (Clearblue)

- 6.3.20 Womaness

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment