PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072745

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072745

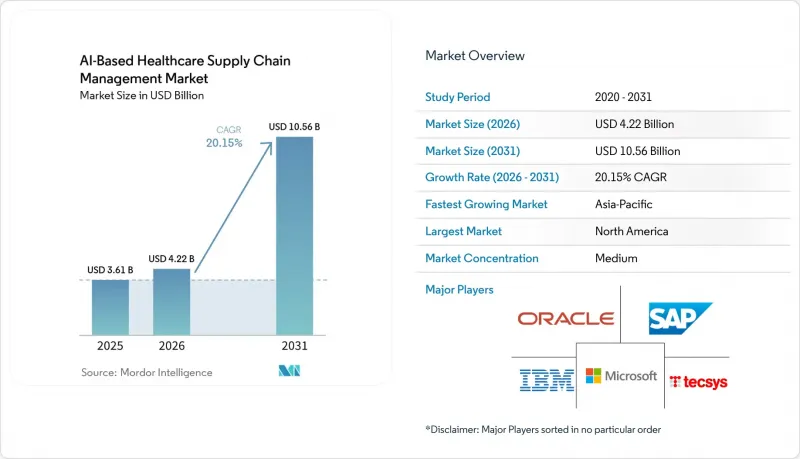

AI-Based Healthcare Supply Chain Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the AI-based healthcare supply chain management market is expected to grow from USD 3.61 billion in 2025 to USD 4.22 billion in 2026 and is forecasted to reach USD 10.56 billion by 2031 at 20.15% CAGR over 2026-2031.

This report is Segmented by Solution Type (Demand Planning and Inventory Optimization, Procurement and Supplier Management, and Others), Deployment Mode (Cloud-Based and On-Premise), End-User (Hospitals and Clinics, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global AI-Based Healthcare Supply Chain Management Market Trends and Insights

Rising Pressure to Cut Healthcare Operating Costs

The AI-based healthcare supply chain management market is gaining momentum because provider margins remain under pressure and supply chain leaders are being asked to show measurable savings within shorter budgeting cycles. Health systems are therefore focusing first on use cases where savings are easiest to verify, especially demand planning, contract compliance, and automated procurement checks that can reduce leakage and avoid excess stock. A 2025 partnership between Tufts Medicine and Premier generated USD 15 million in annual supply chain savings through AI-assisted inventory management and contracting analytics, which supports the case for broader operational rollouts.The AI-based healthcare supply chain management market is also benefiting from a structural change in procurement behavior, where health systems are moving away from static catalog dependence toward real-time monitoring of pricing, supplier compliance, and off-contract buying. That change expands the role of software beyond purchasing administration and brings AI deeper into sourcing strategy, spend governance, and replenishment planning. GHX also noted that a 2025 Experian survey found that 50% of healthcare decision-makers saw data quality as a top barrier to capturing these savings, which shows that the savings logic is established even when execution remains uneven.

AI and Big-Data Adoption in Healthcare Logistics

The AI-based healthcare supply chain management market is still in an early scale-up stage, even though demand forecasting, inventory optimization, and supply planning are already recognized as high-value AI use cases. The real barrier is often not the AI model itself, but the absence of normalized item masters, clean procurement records, and reliable interfaces between ERP, EHR, warehouse, and supplier systems. GHX reported in July 2025 that it supports more than USD 220 billion in annual supply chain spend across over 4,100 providers and 600 suppliers in North America, which shows why incumbents with rich transaction data can train stronger domain models than many software-only entrants. The AI-based healthcare supply chain management market is therefore being shaped by data scale and data quality as much as by algorithm choice, and that favors vendors that already sit inside high-volume healthcare trading networks.

Data-Privacy and Cyber-Risk Exposure

The AI-based healthcare supply chain management market faces a meaningful adoption brake because healthcare buyers are being asked to trust AI systems that sit across large vendor ecosystems and influence critical stock, contract, and compliance decisions. The HSCC Cybersecurity Working Group stated in its April 2026 AI Third-Party Risk Guide that many healthcare organizations still maintain incomplete or outdated vendor inventories and that AI-specific risks often go unreported by vendors. Proofpoint's 2025 Ponemon healthcare cybersecurity report also found that 93% of healthcare organizations experienced a cyberattack in the previous 12 months and that 60% of respondents said protecting data used in AI systems was difficult or very difficult. This concern goes beyond simple breach risk, because procurement committees also worry about regulatory exposure, operational disruption, and the credibility of vendors that cannot clearly explain how their AI models are governed. The AI-based healthcare supply chain management market will therefore continue to see slower decisions in organizations where legal, security, and procurement teams want stronger assurance before expanding AI authority across replenishment and supplier workflows.

Other drivers and restraints analyzed in the detailed report include:

- Growing Complexity of Cold-Chain Biologics Flows

- Global Serialization / Track-and-Trace Mandates

- High Up-Front Integration Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Demand Planning and Inventory Optimization held 40.61% of AI-based healthcare supply chain management market share in 2025, making it the largest solution category by revenue. The segment leads because hospitals, distributors, and manufacturers can see direct value when AI models combine historical demand, procedure schedules, epidemiological indicators, and supplier lead times to improve replenishment timing. The AI-based healthcare supply chain management market rewards this category because it addresses a daily operating problem with measurable consequences in waste, stockouts, emergency buying, and working capital.

Procurement and Supplier Management is the fastest-growing solution type and is forecasted to expand at a 24.6% CAGR through 2031, which reflects how quickly supplier governance is becoming a digital and continuous process. The AI-based healthcare supply chain management industry is moving in this direction because health systems want AI-monitored contract compliance, automated exception handling, and supplier risk scoring instead of periodic manual review cycles. Warehouse and Inventory Execution remains an important part of the AI-based healthcare supply chain management market because labor shortages, error reduction, and throughput reliability matter as much as forecasting accuracy. AI-guided autonomous mobile robots and goods-to-person systems reduce pick errors and lower dependence on manual movement in consolidated service centers and hospital distribution environments. Workflow Automation and Control Tower Platforms are becoming more central because buyers want a single place to manage planning alerts, procurement signals, logistics disruptions, and fulfillment priorities. Medline launched its Mpower AI platform with Northwestern Medicine and Providence in September 2025, using Microsoft Azure AI to create a next-generation supply chain solution that ties multiple operational layers together. In the AI-based healthcare supply chain management market, this integration layer matters because it turns separate forecasting and procurement tools into part of one coordinated operating model.

Complete Report Scope:

- By Solution Type

- Demand Planning and Inventory Optimization

- Procurement and Supplier Management

- Logistics and Distribution Optimization

- Warehouse and Inventory Execution

- Workflow Automation and Control Tower Platforms

- By Deployment Mode

- Cloud-Based

- On-Premise

- By End-User

- Hospitals and Clinics

- Pharmaceutical and Biotech Companies

- Medical Device Manufacturers

- Third-Party Logistics Providers (3PLs)

- Distributors and Wholesalers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 40.11% of AI-based healthcare supply chain management market share in 2025, which kept it as the largest regional market. The region leads because healthcare delivery networks are large, digital maturity is relatively high, and provider and distributor systems are more deeply integrated than in many other markets. The full enforcement milestone for the Drug Supply Chain Security Act on May 27, 2025 strengthened that position by requiring electronic and package-level traceability across prescription drug trading partners. The United States also sees stronger demand for tools that can reduce contract leakage, improve replenishment discipline, and support more auditable workflows across large health systems. This regional structure makes North America the clearest current proof point for enterprise-scale deployment in the AI-based healthcare supply chain management market.

Europe remains an important but more mixed regional environment for the AI-based healthcare supply chain management market because strong compliance demand sits beside more complex integration realities. The region's direction is shaped by the EU Falsified Medicines Directive, the European Medicines Verification Organization framework, and the added friction created by GDPR requirements for data handling and cross-border deployments. The United Kingdom, France, and Italy are also advancing AI-assisted procurement and supply pilots as hospitals work under tighter operating budgets and ongoing service pressure. The AI-based healthcare supply chain management market in Europe therefore combines strong regulatory logic with a slower operational rollout pattern.

Asia-Pacific is projected to expand at a 23.35% CAGR in AI-based healthcare supply chain management market size through 2031, making it the fastest-growing regional market. Growth is being driven by regulatory reform, pharmaceutical export complexity, rising digital infrastructure investment, and stronger supply chain modernization across China, India, Japan, and Southeast Asia. The AI-based healthcare supply chain management market in Asia-Pacific is therefore expanding quickly because manufacturers and distributors are facing both regulatory and operational reasons to digitize. Middle East and Africa, along with South America, remain earlier-stage regions in the AI-based healthcare supply chain management market, but their long-term structure is improving. The GCC benefits from established serialization systems in Saudi Arabia and the UAE, while South Africa offers a focused use case in multi-temperature pharmaceutical distribution. Brazil's SNCM framework and Argentina's ANMAT traceability model create stronger data foundations in South America, especially for pharmaceutical distributors and larger hospital networks. GS1-aligned barcode and EPCIS standards also help lower integration friction for multi-country deployments by giving trading partners a more common data vocabulary.

- Amazon Web Services (AWS)

- Blue Yonder Group Inc.

- Cardinal Health

- CloudMedx Inc.

- IBM

- Kinaxis Inc.

- Koninklijke Philips

- LogITag Systems

- Mckesson

- Medtronic

- Microsoft

- Oracle

- Resilinc Corporation

- SAP

- Syft (GHX)

- Tecsys Inc.

- TractManager (symplr)

- Vizient

- Zebra Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Pressure to Cut Healthcare Operating Costs

- 4.2.2 AI and Big-Data Adoption in Healthcare Logistics

- 4.2.3 Growing Complexity of Cold-Chain Biologics Flows

- 4.2.4 Global Serialization / Track-and-Trace Mandates

- 4.2.5 Autonomous Mobile Robots Optimizing Hospital Stock

- 4.2.6 Hospital-at-Home Models Needing Dynamic Fulfillment

- 4.3 Market Restraints

- 4.3.1 Data-Privacy and Cyber-Risk Exposure

- 4.3.2 High Up-Front Integration Cost

- 4.3.3 Sparse Labeled Data for Niche SKUs

- 4.3.4 Shortage of AI-Supply-Chain Hybrid Talent

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Solution Type

- 5.1.1 Demand Planning and Inventory Optimization

- 5.1.2 Procurement and Supplier Management

- 5.1.3 Logistics and Distribution Optimization

- 5.1.4 Warehouse and Inventory Execution

- 5.1.5 Workflow Automation and Control Tower Platforms

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.3 By End-User

- 5.3.1 Hospitals and Clinics

- 5.3.2 Pharmaceutical and Biotech Companies

- 5.3.3 Medical Device Manufacturers

- 5.3.4 Third-Party Logistics Providers (3PLs)

- 5.3.5 Distributors and Wholesalers

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Amazon Web Services (AWS)

- 6.3.2 Blue Yonder Group Inc.

- 6.3.3 Cardinal Health

- 6.3.4 CloudMedx Inc.

- 6.3.5 IBM

- 6.3.6 Kinaxis Inc.

- 6.3.7 Koninklijke Philips N.V.

- 6.3.8 LogiTag Systems

- 6.3.9 McKesson Corporation

- 6.3.10 Medtronic plc

- 6.3.11 Microsoft Corporation

- 6.3.12 Oracle

- 6.3.13 Resilinc Corporation

- 6.3.14 SAP SE

- 6.3.15 Syft (GHX)

- 6.3.16 Tecsys Inc.

- 6.3.17 TractManager (symplr)

- 6.3.18 Vizient Inc.

- 6.3.19 Zebra Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment