PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072756

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072756

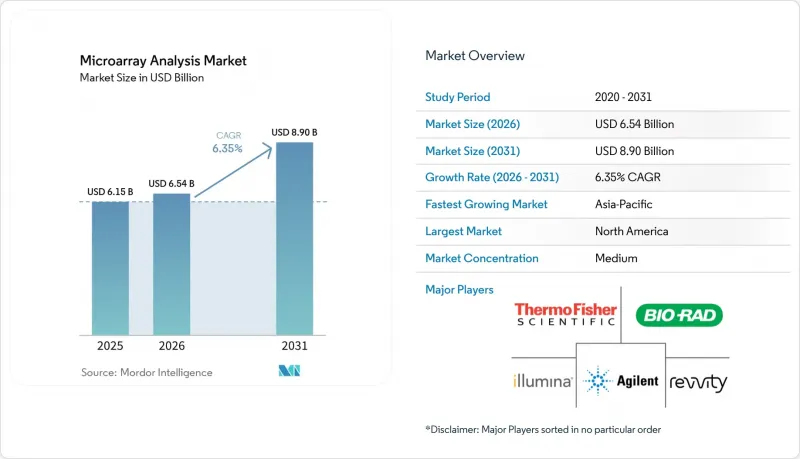

Microarray Analysis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the microarray analysis market size is expected to grow from USD 6.15 billion in 2025 to USD 6.54 billion in 2026 and is forecast to reach USD 8.90 billion by 2031 at 6.35% CAGR over 2026-2031.

This report is Segmented by Product and Services (Instruments, Consumables, Software and Services), Type (DNA, Protein, Tissue, Carbohydrate, Peptide Microarrays), Application (Genomic Profiling, Gene Expression, Drug Discovery, and More), End User (Academic and Research Centers, Pharmaceutical Developers and More), and Geography (North America, Europe, and More). Forecasts are Provided in Value (USD).

Global Microarray Analysis Market Trends and Insights

Expanding Personalized Medicine and Companion Diagnostics Use Cases

The microarray analysis market is gaining support from the broader role of companion diagnostics in oncology drug development. Regulatory pathways that allow clinical development and diagnostic assay validation to proceed in parallel have made array-based patient stratification more practical for mid-stage trials. This matters because drug developers can use established array chemistries earlier in study design and maintain them across later validation work. That approach also creates recurring consumable demand because the validated chemistry often stays linked to the program across the drug's commercial life. The microarray analysis market benefits further when precision oncology testing expands access through commercial partnerships and connected multiomics strategies that keep arrays relevant within broader clinical workflows. In the microarray analysis market, this creates demand that is more durable than one-time research procurement because the testing workflow becomes part of the treatment development path.

Rising Genomics and Proteomics Research Funding

The microarray analysis market has a stable demand base because public research funding continues to support large academic and translational programs. The American Association for Cancer Research reported that the US National Cancer Institute received USD 7.35 billion for FY2026, which was USD 128 million above FY2025, while the NIH budget reached USD 47.2 billion for FY2026. NIH funding priorities also continue to support bioinformatics, translational bioinformatics, and computational biology work that aligns with multi-omics studies and cross-platform analysis. In the microarray analysis market, the most important effect of this funding is not instrument purchases alone, but steady consumable use at medical centers and biobank programs processing large sample volumes. Thermo Fisher Scientific's April 2026 collaboration with Singapore's PRECISE-SG100K program shows how public and institutional genomics infrastructure can translate into long-cycle procurement for integrated proteomics and array-linked workflows. The microarray analysis market therefore retains a strong base of recurring demand even when private R&D budgets fluctuate.

Competition from Next-Generation Sequencing Substitution

The microarray analysis market faces real substitution pressure from next-generation sequencing, but the effect is not uniform across applications. In exploratory research and novel variant discovery, sequencing has a clear advantage because arrays only interrogate known targets. A 2025 study in the International Journal of Molecular Sciences reported that long-read sequencing detected 2.86 times more structural variants than microarray-based short-read approaches in low-complexity and dark genomic regions. Even so, the microarray analysis market remains competitive in genome-wide association studies, pharmacogenomics, and clinical chromosomal analysis, where validated panels, throughput economics, and workflow familiarity still favor arrays. The American College of Medical Genetics and Genomics continues to recommend chromosomal microarray analysis as a first-tier clinical test in several developmental and neurodevelopmental settings, which supports ongoing clinical use. The main risk for the microarray analysis market over the later forecast years is that sequencing cost curves could narrow the price gap in large-cohort genotyping.

Other drivers and restraints analyzed in the detailed report include:

- AI-Assisted Array Design and Signal Interpretation Adoption

- Growth of High-Throughput Biomarker Discovery Workflows

- Limited Skilled Bioinformatics Talent for Array Data Pipelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Consumables captured 48.31% of revenue in 2025, which kept them as the largest component of the microarray analysis market size within product and services. Their leading position reflects the recurring need for reagents, probes, chips, and related materials across the installed base of laboratory systems. This pattern is likely to remain firm in the early forecast period because many laboratories replace instruments only after several years, while consumables are purchased continuously. In the microarray analysis market, that creates a stable revenue stream even when capital spending slows. Thermo Fisher Scientific's October 2025 launch of the SwiftArrayStudio Microarray Analyzer also reinforced the product stack by pairing a higher-throughput instrument with new array content for pharmacogenomics and population-scale GWAS work.

Instruments are projected to grow at an 8.38% CAGR between 2026 and 2031, which makes them the fastest-growing category in this part of the microarray analysis market. That pace reflects a replacement cycle in which automation-ready analyzers are displacing legacy scanners that require more manual intervention. Thermo Fisher stated that SwiftArrayStudio can process up to 1,536 samples in a standard five-day work week and can reduce hands-on time by up to 40%, which directly addresses throughput-sensitive purchasing in pharmacogenomics and agrigenomics laboratories. Software and services are also becoming more central in the microarray analysis industry because cloud bioinformatics and AI-assisted interpretation are shifting spending from one-time product sales toward recurring subscriptions. QIAGEN's QIAsprint Connect, presented at SLAS 2026, shows how vendors are extending workflow control beyond analysis into upstream automation and sample preparation. As a result, boundaries between instruments, consumables, and software are narrowing inside the microarray analysis market.

DNA microarrays held 42.24% of revenue in 2025, which gave them the largest microarray analysis market share within the type segment. Their lead comes from long use in genome-wide association studies, cytogenetics, and pharmacogenomic screening, where validated probe sets and reference databases still provide a strong practical advantage. The October 2025 launch of Thermo Fisher's Axiom PangenomePro Array added broader SNP content for more diverse ancestral populations, which helps address prior limits in genotyping panel representation. Illumina's DRAGEN Array v1.4.0 update in May 2026 also showed continued investment in DNA array infrastructure through better cytogenetics, GAINLOH support, and improved mosaic detection. In the microarray analysis market, this keeps DNA arrays relevant where repeatability and established workflows matter more than exploratory sequencing depth.

Protein microarrays are projected to grow at a 7.52% CAGR through 2031, making them the fastest-growing type in the microarray analysis market. Demand is rising because high-plex protein profiling fits biomarker discovery, autoantibody screening, and companion diagnostic development that cannot be addressed by nucleic acid analysis alone. A May 2026 study in npj Precision Oncology reported 100% concordance across tissue, plasma, and urine samples in mutation-positive colorectal cancer cases using a plasmonic microarray-based KRAS detection approach. Tissue microarrays remain important for pathology research, while carbohydrate and peptide arrays support smaller but growing use cases in immunology and vaccine work. These adjacent formats expand the role of the microarray analysis market beyond established DNA workflows into a wider multi-omics setting.

Complete Report Scope:

- By Product and Services

- Instruments

- Consumables

- Software and Services

- By Type

- DNA Microarrays

- Protein Microarrays

- Tissue Microarrays

- Carbohydrate Microarrays

- Peptide Microarrays

- By Application

- Genomic Profiling

- Gene Expression Analysis

- Drug Discovery

- Biomarker Identification

- Epigenetics

- By End User

- Academic and Research Centers

- Pharmaceutical Developers

- Biotechnology Firms

- Molecular Diagnostic Laboratories

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 46.22% of the microarray analysis market share in 2025, which kept it as the largest regional contributor. The region benefits from high pharmaceutical and biotechnology R&D density, established reimbursement pathways for array-based testing, and a regulatory structure that supports companion diagnostic development. In the microarray analysis market, commercial activity is especially concentrated around Boston-Cambridge and the San Francisco Bay Area, where academic medical centers, CROs, and biopharmaceutical firms create dense demand clusters. Federal research support also remains a major foundation for regional demand. AACR reported that the National Cancer Institute received USD 7.35 billion in FY2026 under the Consolidated Appropriations Act, 2026, which supports long-cycle genomics spending across funded institutions.

Europe remains the second-largest region in the microarray analysis market, led by Germany, the United Kingdom, France, Italy, and Spain. Regional demand is supported by academic cytogenetics programs, pharmaceutical clinical trial networks, and public health genomics activity. Asia-Pacific is forecast to grow at an 8.65% CAGR through 2031, which makes it the fastest-growing regional block in the microarray analysis market. Growth is being driven by infrastructure investment in China, expanding multi-omics activity in India, and broader clinical profiling activity across Japan and other developed healthcare systems.

The microarray analysis market is still smaller in the Middle East and Africa and in South America, but both regions are showing more institutional activity. GCC countries are building biobanking and hospital genomics capacity, while South Africa remains an important reference point for chromosomal microarray testing in sub-Saharan Africa. South America is led by Brazil and Argentina, where university research networks and clinical trial activity support biomarker screening demand. The continuing Centers for Genomics Research Capacity Building opportunity, which remains active through October 2026, points to structured support for genomics infrastructure in lower-resource markets.

- Abcam

- Agilent Technologies

- Arrayit

- Bio-Rad Laboratories

- CapitalBio Technology Co., Ltd.

- Danaher

- Roche

- Illumina

- Merck

- Microarrays Inc.

- PathogenDx, Inc.

- QIAGEN

- RayBiotech Life, Inc.

- Revvity, Inc.

- SCHOTT

- Sengenics Corporation

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Personalized Medicine and Companion Diagnostics Use Cases

- 4.2.2 Rising Genomics and Proteomics Research Funding

- 4.2.3 Growth of High-Throughput Biomarker Discovery Workflows

- 4.2.4 AI-Assisted Array Design and Signal Interpretation Adoption

- 4.2.5 Lab Automation Demand for Sample-to-Insight Efficiency

- 4.2.6 Public Health and Agricultural Genomics Demand for Multiplex Screening

- 4.3 Market Restraints

- 4.3.1 Competition from Next-Generation Sequencing Substitution

- 4.3.2 Limited Skilled Bioinformatics Talent for Array Data Pipelines

- 4.3.3 Instrument, Consumable, and Quality Compliance Cost Burden

- 4.3.4 Fluorophore and Specialized Reagent Supply Concentration Risk

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product and Services

- 5.1.1 Instruments

- 5.1.2 Consumables

- 5.1.3 Software and Services

- 5.2 By Type

- 5.2.1 DNA Microarrays

- 5.2.2 Protein Microarrays

- 5.2.3 Tissue Microarrays

- 5.2.4 Carbohydrate Microarrays

- 5.2.5 Peptide Microarrays

- 5.3 By Application

- 5.3.1 Genomic Profiling

- 5.3.2 Gene Expression Analysis

- 5.3.3 Drug Discovery

- 5.3.4 Biomarker Identification

- 5.3.5 Epigenetics

- 5.4 By End User

- 5.4.1 Academic and Research Centers

- 5.4.2 Pharmaceutical Developers

- 5.4.3 Biotechnology Firms

- 5.4.4 Molecular Diagnostic Laboratories

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Abcam plc

- 6.3.2 Agilent Technologies, Inc.

- 6.3.3 Arrayit Corporation

- 6.3.4 Bio-Rad Laboratories, Inc.

- 6.3.5 CapitalBio Technology Co., Ltd.

- 6.3.6 Danaher Corporation

- 6.3.7 F. Hoffmann-La Roche Ltd.

- 6.3.8 Illumina, Inc.

- 6.3.9 Merck KGaA

- 6.3.10 Microarrays Inc.

- 6.3.11 PathogenDx, Inc.

- 6.3.12 QIAGEN N.V.

- 6.3.13 RayBiotech Life, Inc.

- 6.3.14 Revvity, Inc.

- 6.3.15 SCHOTT AG

- 6.3.16 Sengenics Corporation

- 6.3.17 Thermo Fisher Scientific Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment