PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072757

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072757

Digital Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

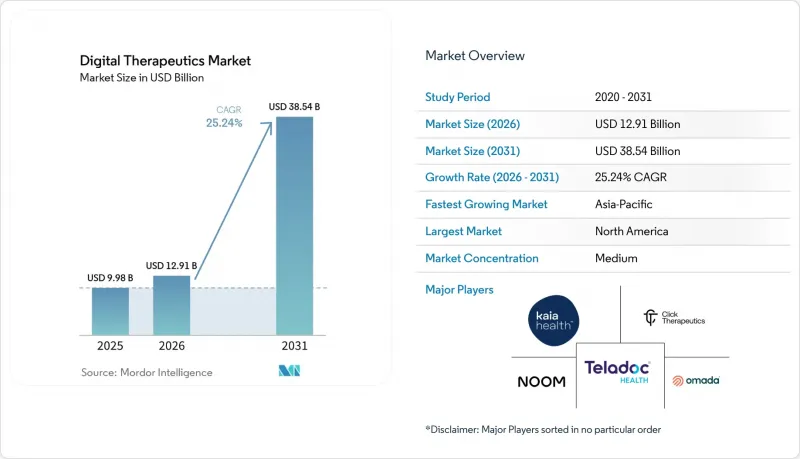

According to Mordor Intelligence, the digital therapeutics market size is projected to be USD 9.98 billion in 2025, USD 12.91 billion in 2026, and reach USD 38.54 billion by 2031, growing at a CAGR of 25.24% from 2026 to 2031.

This report is Segmented by Type (Software, Hardware, Services), Application (Prevention, Management, Treatment), Indication (Diabetes, Obesity, and More), Business Model (Direct-To-Consumer, B2B, Fee-For-Service), End User (Patients, Providers, Payers, Employers), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Digital Therapeutics Market Trends and Insights

Rising Chronic Disease Burden Demands Scalable Intervention Platforms

The digital therapeutics market is growing rapidly due to the increasing prevalence of chronic diseases, which demand scalable care models beyond traditional in-person support. Diabetes remains a key focus area because of its significant care burden, measurable outcomes, and the ability for payers to link digital interventions with medication adherence, glycated hemoglobin levels, and hospitalization risks. Cleveland Clinic's findings on the Twin Precision Treatment platform demonstrated its potential in reducing medication use for type 2 diabetes, strengthening the case for software-driven cardiometabolic care. This approach is now extending to obesity, hypertension, and cardiovascular risk management, where digital programs are integrated with drug therapies and coaching to enhance adherence and care continuity.

AI-Enabled Personalization Raises the Clinical Performance Bar

Personalization is becoming a critical factor in the digital therapeutics market as static content fails to engage diverse patient profiles or improve outcomes effectively. A 2025 trial highlighted the success of Lumen, an AI-driven voice coach, in delivering problem-solving therapy with results comparable to human coaching. Another study emphasized the benefits of reinforcement learning in personalizing interventions for depression and anxiety, showing significant improvements over non-personalized approaches. Buyers are increasingly prioritizing AI-driven solutions that enhance clinical responses and reduce care costs. Vendors offering patient-specific adaptations are better positioned in coverage discussions, particularly in mental health and chronic disease programs, where dropout rates remain a challenge. This trend is raising the performance standards across the market.

Reimbursement Fragmentation Constrains Scalable Commercial Models

The digital therapeutics market faces limited commercial access due to fragmented reimbursement frameworks across payers, countries, and care settings. In the U.S., the 2025 Physician Fee Schedule introduced G-codes for digital mental health devices, but the absence of national pricing leaves access reliant on contractor-level pricing and local billing processes. Reimbursement strategies for prescription digital therapeutics vary widely, with policy design playing a critical role in patient access, provider adoption, and commercial scalability. This creates a divide between companies capable of managing extended coverage timelines and those restricted to employer-direct or cash-pay models.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Normalization of SaMD Creates Institutional Access Pathways

- Accelerating Payer Adoption Through Outcome-Linked Contracting

- Engagement Attrition Undermines Real-World Evidence Generation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, software solutions held 53.78% of the digital therapeutics market, driven by app-based therapy models that bypass the need for specialized hardware. This segment thrived due to rapid distribution, seamless updates, and reduced delivery costs, establishing it as the commercial backbone for early and mid-stage players. Hardware remained the smallest segment, primarily serving a supportive role integrated with sensors, wearables, or other connected devices. Software's centrality in the digital therapeutics market was reinforced, especially in scenarios where mobile interfaces sufficed for clinical pathways without requiring remote monitoring.

Services are projected to grow at a 27.10% CAGR from 2026 to 2031, reflecting a shift in buyer preferences toward managed care layers around software. Health systems, payers, and employers increasingly value care navigation, coaching, reporting, and implementation support to enhance activation, continuity, and accountability. This shift is driving the market toward ongoing program delivery rather than one-time licensing or app subscriptions. Software remains the core therapeutic engine, while services emerge as the commercial layer translating adoption into measurable outcomes.

Prevention accounted for 42.25% of the digital therapeutics market in 2025, supported by strong adoption in diabetes prevention, smoking cessation, and weight management. These areas had established a solid commercial foundation due to employer and health plan funding for preventive measures with familiar behavior-change models. Prevention's lower clinical complexity compared to prescription treatments enabled broader deployment across large member pools, making it the largest application segment in 2025. However, growth is now shifting toward active disease management.

Management is expected to grow at a 28.56% CAGR through 2031, driven by rising demand for programs demonstrating cost-offset benefits in cardiometabolic care and chronic conditions. Omada Health reported Q1 2026 revenue of USD 78 million, a 42% year-over-year increase, with total members exceeding 1.02 million, showcasing the scalability of management-focused platforms. Treatment remains the smallest segment due to stricter authorization and evidence requirements, but the revenue mix is increasingly favoring management as payers prioritize cost-control programs over general wellness initiatives.

Complete Report Scope:

- By Type

- Softwares

- Hardware

- Services

- By Application

- Prevention

- Management

- Treatment

- By Indication

- Diabetes

- Obesity

- Gastrointestinal Disorders

- Cardiovascular Disease

- Central Nervous System Disorders

- Respiratory Disorders

- Smoking Cessation

- Other Indications

- By Business Model

- Direct-to-Consumer

- Business-to-Business

- Fee-for-Service

- By End User

- Patients

- Providers

- Payers

- Employers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America accounted for 41.25% of the global digital therapeutics market, making it the largest regional contributor by revenue and the most commercially advanced market. This leadership stemmed from the FDA's regulatory framework, a strong employer self-insurance base, active venture-backed developments, and institutional readiness for software-driven care models. The 2025 Physician Fee Schedule introduced reimbursement codes for digital mental health treatment devices, creating a formal billing mechanism despite pending national pricing.

Europe remained the second-largest regional market, with Germany leading due to its DiGA model, the most structured national reimbursement pathway for digital therapeutics. In 2025, the DiGA program recorded 695,000 activated prescriptions, costing EUR 171 million (USD 184 million), reflecting 64% year-over-year growth. From January 2026, Germany required at least 20% of DiGA reimbursement pricing to be tied to measured outcomes, favoring platforms with robust real-world data systems. Other European countries, including the UK, France, Italy, and Spain, are progressing gradually, while partnerships like GAIA and Daiichi Sankyo Europe demonstrate the use of the German pathway for broader commercialization.

The Asia-Pacific region is the fastest-growing digital therapeutics market, with a projected CAGR of 27.60% from 2026 to 2031. Growth is driven by rising chronic disease prevalence, expanding digital health infrastructure, and formal software-as-medical-device pathways in Japan, South Korea, and Australia. By 2025, South Korea approved 14 digital therapeutics products, including the insomnia treatment Somzz, showcasing regulatory progress. Japan's PMDA framework and Australia's TGA pathway are advancing structured approval and reimbursement processes, particularly in mental health and diabetes care.

- 2Morrow

- Akili

- Better Therapeutics, LLC

- Big Health Ltd

- Biofourmis Inc.

- Canary Health, Inc.

- Click Therapeutics, Inc.

- DarioHealth Corp.

- Huma Therapeutics Limited

- IQVIA

- Kaia Health Software GmbH

- Lark Technologies, Inc.

- Medtronic

- Noom, Inc.

- Omada Health

- Otsuka

- Resmed

- Teladoc Health

- Virta Health Corp.

- Welldoc, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Chronic Disease Burden Requiring Continuous Out-of-Clinic Care

- 4.2.2 Accelerating Payer Adoption of Value-Based Digital Care Pathways

- 4.2.3 Prescription Digital Therapeutics Integration with GLP-1 and Other Drug Regimens

- 4.2.4 AI-Enabled Personalization and Adaptive Coaching Increasing Clinical Persistence

- 4.2.5 Greater Employer Demand for Measurable Productivity and Adherence Outcomes

- 4.2.6 Regulatory Normalization of SaMD, PDURS, and Reimbursement Pathways

- 4.3 Market Restraints

- 4.3.1 Uneven Reimbursement Coverage Across Indications and Payers

- 4.3.2 High Evidence Generation Cost for Clinical Validation and Real-World Proof

- 4.3.3 Low Persistence and Engagement Drop-Off After Initial Adoption

- 4.3.4 Integration Friction with EHR, Claims, and Provider Workflows

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Type

- 5.1.1 Softwares

- 5.1.2 Hardware

- 5.1.3 Services

- 5.2 By Application

- 5.2.1 Prevention

- 5.2.2 Management

- 5.2.3 Treatment

- 5.3 By Indication

- 5.3.1 Diabetes

- 5.3.2 Obesity

- 5.3.3 Gastrointestinal Disorders

- 5.3.4 Cardiovascular Disease

- 5.3.5 Central Nervous System Disorders

- 5.3.6 Respiratory Disorders

- 5.3.7 Smoking Cessation

- 5.3.8 Other Indications

- 5.4 By Business Model

- 5.4.1 Direct-to-Consumer

- 5.4.2 Business-to-Business

- 5.4.3 Fee-for-Service

- 5.5 By End User

- 5.5.1 Patients

- 5.5.2 Providers

- 5.5.3 Payers

- 5.5.4 Employers

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 2Morrow, Inc.

- 6.3.2 Akili, Inc.

- 6.3.3 Better Therapeutics, LLC

- 6.3.4 Big Health Ltd

- 6.3.5 Biofourmis Inc.

- 6.3.6 Canary Health, Inc.

- 6.3.7 Click Therapeutics, Inc.

- 6.3.8 DarioHealth Corp.

- 6.3.9 Huma Therapeutics Limited

- 6.3.10 IQVIA Holdings Inc.

- 6.3.11 Kaia Health Software GmbH

- 6.3.12 Lark Technologies, Inc.

- 6.3.13 Medtronic plc

- 6.3.14 Noom, Inc.

- 6.3.15 Omada Health, Inc.

- 6.3.16 Otsuka Pharmaceutical Co., Ltd.

- 6.3.17 ResMed Inc.

- 6.3.18 Teladoc Health, Inc.

- 6.3.19 Virta Health Corp.

- 6.3.20 Welldoc, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment