PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072800

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072800

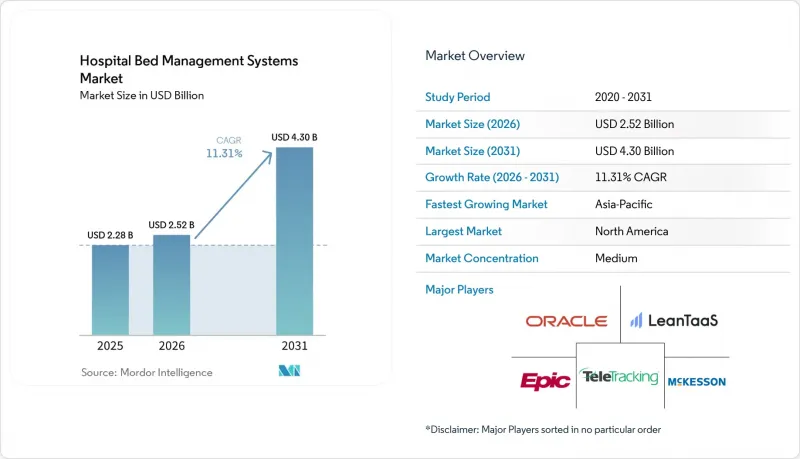

Hospital Bed Management Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the hospital bed management systems market is expected to increase from USD 2.28 billion in 2025 to USD 2.52 billion in 2026 and reach USD 4.30 billion by 2031, growing at a CAGR of 11.31% over 2026-2031.

This report is Segmented by Component (Software, Hardware, Services), Deployment Mode (Cloud-Based, On-Premises), Type (Real-Time Bed Tracking Systems, and Others), End-User (General Hospitals, Specialty, and Other End-Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Hospital Bed Management Systems Market Trends and Insights

Rising Hospital Admissions and Bed Occupancy Pressure

The hospital bed management systems market is gaining support from sustained pressure on hospital capacity and from the limited room many systems have for physical bed expansion. OECD data showed that the average bed-to-population ratio across member countries fell to 4.2 beds per 1,000 people in 2023, extending the longer decline seen across most high-income systems. Japan and South Korea remained exceptions at 12.5 and 12.6 beds per 1,000 people, but even that larger installed base increases the need for orchestration so distributed bed estates do not become fragmented. Once occupancy rises above the practical resilience ceiling, hospitals are no longer just buying efficiency software and are instead buying operating headroom that helps avoid canceled elective procedures, emergency department diversions, and delayed admission penalties. That dynamic keeps the hospital bed management systems market closely tied to inpatient pressure, regardless of whether a system has a low bed base or a large distributed estate.

Need for Faster Patient Flow and Shorter Length of Stay

The hospital bed management systems market is also being lifted by the need to reduce avoidable bed days and shorten length of stay without adding physical capacity. Queensland Health data cited by Alcidion showed that patients medically ready for discharge but still awaiting coordination represented 25% of inpatient bed days, and the related cost exceeded AUD 6.5 million per 500-bed hospital annually. Queen's Health Systems in Hawaii cut patient length of stay by 0.7 days within 6 months of implementing GE HealthCare's Command Center, and it did so without adding any physical beds. Each avoided bed day creates incremental admissions capacity at zero marginal infrastructure cost, which is why patient flow spending is increasingly treated as a revenue and throughput tool rather than only a cost program.

High Implementation and Integration Costs

The hospital bed management systems market still faces a clear barrier from the high upfront cost of implementation across mixed hospital IT estates. Multi-site rollouts often require custom HL7 connectors, workflow redesign, vendor consulting, and extended deployment support, which can stretch payback periods beyond what community and district hospitals can absorb in one budget cycle. The challenge grows when bed management must connect with a primary EHR, laboratory systems, pharmacy platforms, environmental services scheduling, and patient transport tools at the same time. In lower-income settings, that cost burden often limits adoption to the largest private hospital groups with stronger digital budgets. Underfunded early deployments can also stop at the reporting layer, which leaves hospitals with dashboards that describe flow problems but do not automate the workflows needed to correct them.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of EHR-Integrated Bed Allocation Workflows

- Rapid Shift to Cloud-Based Hospital Operations Platforms

- Cybersecurity and Data-Privacy Risk Around Real-Time Occupancy Data

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 62.21% of the hospital bed management systems market share in 2025. That leadership reflects the shift away from hardware-heavy RTLS deployments and toward recurring SaaS subscriptions, configuration-led contracts, and software modules that continue generating revenue after go-live. Predictive analytics, AI-driven discharge orchestration, and multi-site command center dashboards are all software-led capabilities that deepen the role of digital operating intelligence. Hardware still supports real-time tracking through RTLS tags, BLE sensors, and bedside terminals, but it is losing relative weight as existing networks and cloud APIs take over more of the data layer.

The hospital bed management systems market is expected to see the services segment expand at an 11.53% CAGR through 2031. That pace reflects the difficulty of integrating bed management platforms with EHRs, workforce scheduling tools, environmental services workflows, and RTLS hardware from several vendors. Services growth also shows that hospitals need workflow redesign and clinical process support, not only software configuration, if they want sustained throughput gains. This revenue mix favors vendors that can combine technology delivery with operational change management, and it supports continued reinvestment into AI features that increase platform stickiness.

Cloud-based deployment accounted for 65.61% share of the hospital bed management systems market size in 2025. That dual lead in adoption and scale shows that the market has already moved beyond the early inflection point for cloud infrastructure. A cloud model gives health systems one view across a network, faster site activation, and less internal server maintenance for IT teams that are already stretched by large clinical platforms. It also supports easier expansion into multi-facility command center models, which depend on fast and consistent data exchange across hospitals.

The hospital bed management systems market is anticipated to see cloud-based deployment grow at a 12.65% CAGR through 2031. On-premises systems still keep a residual role in public health settings with strict data sovereignty rules and in high-security hospitals where data residency remains a hard requirement. Even so, the choice of deployment mode now shapes how widely bed management can connect with staffing, surgery scheduling, and environmental services workflows. Cloud therefore acts as a strategic operating choice rather than only an IT preference.

Complete Report Scope:

- By Component

- Software

- Hardware

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- By Type

- Real-Time Bed Tracking Systems

- Patient Flow Management Systems

- Bed Capacity Planning Systems

- Integrated Bed Management Platforms

- By End-User

- General Hospitals

- Specialty Hospitals

- Ambulatory Surgical Centers

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America accounted for 44.25% share of the hospital bed management systems market size in 2025. The region benefits from dense multi-site health systems, mature EHR environments, and an operating culture that links bed performance to reimbursement outcomes under value-based care. The United States remains the largest country market in the region, and the strong installed base of Epic Systems and Oracle Health gives EHR-native bed management tools a meaningful distribution advantage. In Canada, acute-care occupancy already exceeded 85% in multiple provinces according to OECD data, which is pushing procurement of real-time capacity tools beyond the traditionally cautious public procurement cycle. Mexico is moving forward through public hospital modernization, although adoption remains slower outside major metropolitan systems because of budget limits.

Europe is the second-largest regional block in the hospital bed management systems market. Germany, the United Kingdom, and France anchor demand, with the United Kingdom standing out because persistent discharge delays and chronic bed shortages create a clear case for digital patient flow tools. Alcidion reported that its Miya Precision deployment across Herefordshire and Worcestershire Health and Care NHS Trust delivered a 5-day reduction in average length of stay during the first program phase. Across the region, procurement is shaped not only by throughput needs but also by compliance with national health data rules and broader cybersecurity requirements.

Asia-Pacific is projected to be the fastest-growing region in the hospital bed management systems market, with a projected CAGR of 13.76% through 2031. In China and India, government-backed hospital modernization creates greenfield openings for cloud-native deployment because legacy integration barriers are often lighter than in mature Western systems. Australia continues to act as an early adopter, and GE HealthCare's Command Center deployment across The Alfred, Caulfield, and Sandringham hospitals in Melbourne gives the region a reference case for broader adoption. Middle East and Africa and South America remain earlier-stage markets, but growth potential is supported by GCC hospital construction programs, Saudi Arabia's healthcare infrastructure agenda, and private hospital investments in Brazil and Argentina.

- Alcidion Group Limited

- Allscripts

- Central Logic, Inc.

- Dedalus S.p.A.

- Epic Systems

- GE Healthcare

- Infor, Inc.

- Intersystems

- Koninklijke Philips

- LeanTaaS, Inc.

- Mckesson

- MEDITECH, Inc.

- Omnicell

- Oracle

- Qventus, Inc.

- Siemens Healthineers

- TeleTracking Technologies, Inc.

- The Access Group

- Veradigm

- WellSky Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Hospital Admissions and Bed Occupancy Pressure

- 4.2.2 Need for Faster Patient Flow and Shorter Length of Stay

- 4.2.3 Expansion of EHR-Integrated Bed Allocation Workflows

- 4.2.4 Rapid Shift to Cloud-Based Hospital Operations Platforms

- 4.2.5 Real-Time Bed Turnover Auditability for Multi-Site Health Systems

- 4.2.6 Infection-Control Driven Demand for Isolation and Cohort Bed Orchestration

- 4.3 Market Restraints

- 4.3.1 High Implementation and Integration Costs

- 4.3.2 Legacy EHR and HIS Interoperability Complexity

- 4.3.3 Limited Digital-Operations Budget in Public and Smaller Hospitals

- 4.3.4 Cybersecurity and Data-Privacy Risk Around Real-Time Occupancy Data

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Hardware

- 5.1.3 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.3 By Type

- 5.3.1 Real-Time Bed Tracking Systems

- 5.3.2 Patient Flow Management Systems

- 5.3.3 Bed Capacity Planning Systems

- 5.3.4 Integrated Bed Management Platforms

- 5.4 By End-User

- 5.4.1 General Hospitals

- 5.4.2 Specialty Hospitals

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Alcidion Group Limited

- 6.3.2 Allscripts Healthcare Solutions, Inc.

- 6.3.3 Central Logic, Inc.

- 6.3.4 Dedalus S.p.A.

- 6.3.5 Epic Systems Corporation

- 6.3.6 GE HealthCare

- 6.3.7 Infor, Inc.

- 6.3.8 InterSystems Corporation

- 6.3.9 Koninklijke Philips N.V.

- 6.3.10 LeanTaaS, Inc.

- 6.3.11 McKesson Corporation

- 6.3.12 MEDITECH, Inc.

- 6.3.13 Omnicell, Inc.

- 6.3.14 Oracle

- 6.3.15 Qventus, Inc.

- 6.3.16 Siemens Healthineers AG

- 6.3.17 TeleTracking Technologies, Inc.

- 6.3.18 The Access Group

- 6.3.19 Veradigm LLC

- 6.3.20 WellSky Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment