PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072801

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072801

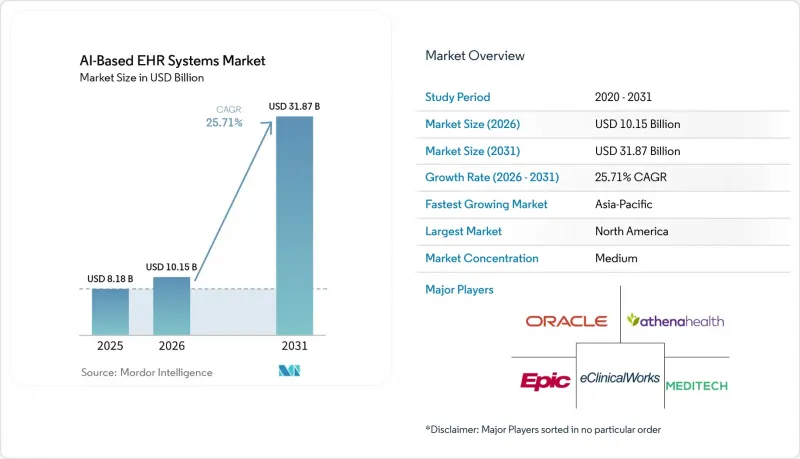

AI-Based EHR Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the AI-based EHR systems market is expected to grow from USD 8.18 billion in 2025 to USD 10.15 billion in 2026 and is forecasted to reach USD 31.87 billion by 2031 at 25.71% CAGR over 2026-2031.

This report is Segmented by EHR Type (On-Premise Electronic Health Records Software, and Others), Technology (Machine Learning, Deep Learning, and Others), Application (Data Management and Organization, and Others), End-User (Hospitals, Clinics, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global AI-Based EHR Systems Market Trends and Insights

Rising Demand for Ambient Clinical Scribing

Ambient clinical scribing has become the clearest short-cycle adoption path in the AI-based EHR systems market because it addresses a daily documentation burden that clinicians feel in nearly every patient encounter. Health systems have moved faster here because documentation pressure affects visit flow, physician capacity, staff burnout, and after-hours charting in ways that are immediate and measurable. At Intermountain Health, clinicians using Dragon Copilot saw a 27% reduction in time spent in notes per appointment across tracking from April 2024 through December 2025, and across five academic medical centers, AI scribe access cut total EHR time by 13.4 minutes per visit. That matters because the AI-based EHR systems market is increasingly being judged on recovered clinician time and documentation quality, not only on software feature breadth. At the same time, payer interest in downcoding responses to richer AI-generated notes means some systems may see documentation quality improve faster than reimbursement yield, which changes the economic case for deployment at scale. This keeps demand strong, but it also pushes buyers to justify ambient tools through productivity, compliance quality, and clinician experience rather than through revenue uplift alone.

EHR-Native AI Integration in Core Workflows

EHR vendors embedding AI directly inside their own platforms mark a deeper structural shift in the AI-based EHR systems market because workflow control is moving back toward the system of record. Epic put native AI Charting into live use in February 2026, and its Curiosity foundation models and Agent Factory platform show a clear effort to keep AI orchestration at the platform layer rather than leave it to external tools. Oracle has taken a similar direction by positioning AI-driven electronic health records as native workflow tools, not as add-on modules that sit outside the main record environment. As that pattern spreads, the AI-based EHR systems market gives third-party vendors less room to win on simple integration alone, because large platforms can bundle documentation, summarization, and workflow assistance into core contracts. This is pushing specialist AI firms toward areas such as revenue cycle intelligence, prior authorization, population health, and specialty-specific automation where EHR incumbency is weaker. The effect is not the disappearance of external AI vendors, but a shift in where margins can still be defended.

Patient Consent Limits for Ambient Audio Capture

Consent limits remain a structural brake on the AI-based EHR systems market because ambient capture involves live audio from clinical encounters, not simply retrospective text processing. Several U.S. states apply two-party consent rules under wiretapping laws, which creates uneven deployment conditions for health systems operating across multiple jurisdictions. The issue is harder in practice than in policy documents because workflows must explain consent clearly, capture it consistently, and ensure that the record shows how audio-derived text entered the chart. An NHS England pilot conducted from May through September 2025 found that when an ambient scribe was not integrated directly into the EHR, clinicians resorted to copying and pasting AI-generated notes, which introduced both safety concerns and traceability gaps. That finding matters for the AI-based EHR systems market because it shows that disconnected workarounds do not remove the consent problem, they simply move it into less visible parts of the workflow. Vendors that cannot offer native, auditable integration will therefore face slower adoption in organizations with stricter legal review.

Other drivers and restraints analyzed in the detailed report include:

- Interoperability Mandates and FHIR Adoption

- Value-Based Care and Revenue Integrity Pressure

- Clinical Liability and Human Review Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SaaS electronic health records held 49.52% of the AI-based EHR systems market share in 2025, reflecting the continuation of multi-year migration away from on-premise infrastructure. In the AI-based EHR systems market, SaaS stands out because continuous model updates, fast rollout of ambient scribing improvements, and vendor-managed cloud inference reduce local hardware dependence. SaaS also gives provider networks a more practical path to deploy improvements across hospitals, outpatient sites, and multi-specialty clinics without separate hardware cycles for each location. These advantages have made cloud delivery the default choice for buyers that value scale, update speed, and centralized governance.

Custom-built electronic health records are projected to grow at 26.33% CAGR through 2031, showing that some health systems still prefer to build tailored AI layers on top of FHIR-ready data environments. That pattern suggests the AI-based EHR industry is not moving toward a single packaged architecture, because large enterprises with internal engineering resources want tighter control over workflow logic, specialty requirements, and internal orchestration. In effect, the line between packaged SaaS and custom development is becoming less rigid as platforms expose more controlled customization layers. On-premise deployments still persist in large academic medical centers and federal environments with sovereign data requirements, but their AI capabilities remain more constrained by inference latency, self-hosting burdens, and slower model update cycles.

Machine learning retained 57.41% share in 2025, which shows how deeply predictive models are already embedded across deterioration alerts, risk stratification, revenue cycle automation, and patient flow management. Much of this installed base predates the current generative AI cycle, which is why the AI-based EHR systems market still leans heavily on established machine learning infrastructure even as newer tools receive more attention. Providers continue to rely on these models because they support operational decisions that are measurable, recurrent, and closely tied to quality and financial performance. The installed machine learning layer also gives vendors a base from which newer AI tools can be attached more easily inside existing EHR workflows. This helps explain why mature predictive capabilities still anchor the technology mix even while other modalities expand more quickly.

Natural language processing is forecasted to grow at 25.87% CAGR through 2031, making it the fastest-moving technology layer in the AI-based EHR systems market. Its growth is tied less to general chatbot adoption and more to ambient documentation, ICD coding automation, and clinical documentation integrity workflows that sit close to daily clinical operations. Deep learning is also gaining traction where models need to process narrative notes, lab values, and imaging-related information together, although deployment moves more slowly when regulatory requirements become more demanding.

Complete Report Scope:

- By EHR Type

- On-Premise Electronic Health Records Software

- SaaS Electronic Health Records

- Custom-Built Electronic Health Records

- By Technology

- Machine Learning

- Deep Learning

- Natural Language Processing

- By Application

- Data Management and Organization

- Data Analysis and Insights

- Predictive Analytics

- Virtual Medical Assistance

- Clinical Decision Support

- Clinical Documentation Integrity and Coding Support

- By End-User

- Hospitals

- Clinics

- Ambulatory Surgical Centers

- Diagnostic Centers

- Other End-Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America held 46.48% share of the AI-based EHR systems market size in 2025, supported by the region's dense Epic and Oracle Health installed base and by reimbursement structures that reward detailed documentation. In the AI-based EHR systems market, that reimbursement logic makes documentation integrity a financial priority for leadership teams, not only an IT issue. The United States remains the core demand center because value-based contracts make better risk capture and cleaner records commercially meaningful across provider organizations. ONC's HTI-5 proposal and the compliance buildout around prior authorization APIs are also accelerating FHIR readiness across the broader North American provider and payer ecosystem.

Asia-Pacific is forecasted to grow at 27.66% CAGR through 2031, which makes it the fastest-rising regional pool in the AI-based EHR systems market. Growth is being driven by government-led digital health programs in India and by the acceleration of AI integration mandates across Japan, South Korea, and Australia. The region also has large patient volumes and many under-documented care settings, which increases the value of multilingual documentation tools and specialty models. Cost discipline matters more here than in North America, so deployment models that reduce compute intensity and shorten implementation cycles are likely to gain faster traction. This means Asia-Pacific is not only a demand story for new software, but also a proving ground for scalable and lower-cost enterprise AI operations.

Europe held a meaningful share in 2025, and the AI-based EHR systems market there is supported by NHS digital transformation programs and Germany's hospital digitization fund even though GDPR complexity and fragmented national standards slow implementation. The EU AI Act, combined with MDR and IVDR obligations, adds a longer compliance path for new entrants and gives established vendors with regulatory processes more protection. In the Middle East and Africa and in South America, sovereign healthcare investment and ongoing digitization create longer-cycle opportunities for vendors that can support Arabic- and Portuguese-language clinical workflows. These regions remain smaller today, but they are strategically important because future growth will depend on how well vendors adapt models, interfaces, and governance to under-resourced settings.

- Abridge AI, Inc.

- AdvancedMD

- Allscripts

- Amazon Web Services, Inc.

- Athenahealth

- CitiusTech

- CureMD Healthcare

- eClinicalWorks

- Epic Systems

- Google Cloud

- Health Catalyst, Inc.

- Intersystems

- Meditech

- Microsoft

- Netsmart Technologies, Inc.

- NextGen Healthcare

- Oracle

- PointClickCare

- Practice Fusion, Inc.

- Suki AI, Inc.

- Veradigm

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Ambient Clinical Scribing

- 4.2.2 EHR-Native AI Integration in Core Workflows

- 4.2.3 Interoperability Mandates and FHIR Adoption

- 4.2.4 Value-Based Care and Revenue Integrity Pressure

- 4.2.5 Multilingual Specialty Models for Under-Documented Settings

- 4.2.6 GPU-Efficient Enterprise AI Deployment Models

- 4.3 Market Restraints

- 4.3.1 Patient Consent Limits for Ambient Audio Capture

- 4.3.2 Clinical Liability and Human Review Requirements

- 4.3.3 Cybersecurity and Centralized Data Exposure

- 4.3.4 Token, Inference, and Latency Economics at Scale

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By EHR Type

- 5.1.1 On-Premise Electronic Health Records Software

- 5.1.2 SaaS Electronic Health Records

- 5.1.3 Custom-Built Electronic Health Records

- 5.2 By Technology

- 5.2.1 Machine Learning

- 5.2.2 Deep Learning

- 5.2.3 Natural Language Processing

- 5.3 By Application

- 5.3.1 Data Management and Organization

- 5.3.2 Data Analysis and Insights

- 5.3.3 Predictive Analytics

- 5.3.4 Virtual Medical Assistance

- 5.3.5 Clinical Decision Support

- 5.3.6 Clinical Documentation Integrity and Coding Support

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Clinics

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Diagnostic Centers

- 5.4.5 Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Abridge AI, Inc.

- 6.3.2 AdvancedMD, Inc.

- 6.3.3 Allscripts Healthcare, LLC

- 6.3.4 Amazon Web Services, Inc.

- 6.3.5 athenahealth, Inc.

- 6.3.6 CitiusTech Inc.

- 6.3.7 CureMD Healthcare

- 6.3.8 eClinicalWorks

- 6.3.9 Epic Systems Corporation

- 6.3.10 Google Cloud

- 6.3.11 Health Catalyst, Inc.

- 6.3.12 InterSystems Corporation

- 6.3.13 MEDITECH

- 6.3.14 Microsoft Corporation

- 6.3.15 Netsmart Technologies, Inc.

- 6.3.16 NextGen Healthcare, Inc.

- 6.3.17 Oracle Corporation

- 6.3.18 PointClickCare

- 6.3.19 Practice Fusion, Inc.

- 6.3.20 Suki AI, Inc.

- 6.3.21 Veradigm LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment