PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072865

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072865

Fortified Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

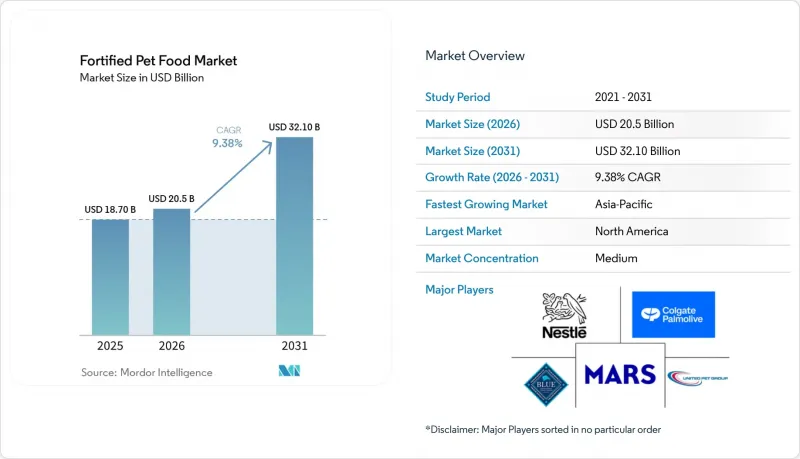

According to Mordor Intelligence, the fortified pet food market size is anticipated to increase from USD 18.7 billion in 2025 to USD 20.5 billion in 2026 and reach USD 32.1 billion by 2031, growing at a CAGR of 9.38% over 2026-2031.

This report is Segmented by Product Type (Dry Food, Wet Food, Treats and Snacks, and More ), by Pet Type (Dog, Cat, and Others), by Fortificant (Vitamin Enriched, Mineral Enriched, and More), by Distribution Channel (Supermarkets and Hypermarkets, Specialty Pet Stores, and More), and by Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Fortified Pet Food Market Trends and Insights

Premiumization of Pet Diets

Upgrading to super-premium fortified formulas is a prominent trend reflecting the humanization of pets. According to the American Pet Products Association (APPA) 2025 State of the Industry Report, pet owner spending in the United States reached USD 158 billion in 2025. Despite relatively stable pet food prices, this growth suggests that increased consumption volume, rather than inflation, is driving the fortified pet food market. Similar trends are emerging in other regions, where pet owners are increasingly opting for premium nutrition products enriched with functional ingredients such as omega-3 fatty acids, probiotics, and joint-support nutrients to enhance pet health and wellness.

Humanization Trend in Emerging Markets

Disposable income growth in China, India, and key Southeast Asian economies is driving stronger adoption of fortified pet food that mirrors human wellness trends. As reported in the China Pet Industry White Paper (2025), referenced by the State Council Information Office of China, the urban pet dog and cat market in the country reached CNY 300.2 billion (USD 41.3 billion) in 2024. This growth highlights the increasing expenditure on premium pet care products and specialized nutrition solutions. Comparable trends are observed in other developing markets, driven by rising pet ownership, higher disposable incomes, and the growth of e-commerce platforms. These factors are boosting demand for fortified pet foods containing functional ingredients aimed at enhancing overall pet health and wellness. Brands are introducing gently cooked fresh diets and kibble-wet hybrids that highlight whole-food ingredients, reflecting how human-grade cues are influencing the fortified pet food market.

Volatility in Specialty Micronutrient Costs

Peru reduced its 2026 anchovy quota by 36% to 1.91 million metric tons, cutting the primary raw material for fish oil that underpins omega-3 fortification and driving spot prices toward USD 5,000 per metric ton. Aquaculture accounts for over 70% of the global 1.2 million metric ton fish-oil supply, leaving pet food formulators to compete for shrinking residual volumes and expose them to sudden cost spikes. Vitamin premix pricing is equally erratic because environmental shutdowns at Chinese and Indian plants periodically constrict output and create supply gaps. Large manufacturers hedge through vertical integration and long-term contracts, whereas smaller brands must either raise retail prices or reformulate with alternative sources, such as krill oil from suppliers like Aker BioMarine, eroding competitiveness in premium segments.

Other drivers and restraints analyzed in the detailed report include:

- Advancements in Nutrient-Microencapsulation

- Veterinary Endorsement Programs

- Stringent Fortification Labeling Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dry food held the largest share, accounting for 46.0% of the fortified pet food market size in 2025, but the fortified pet food market tied to dry kibble is projected to rise only modestly as consumers migrate toward fresh and wet textures. Functional supplements are forecast to grow at the fastest rate, with a 13.8% CAGR, catering to joint, gut, and immune needs that cannot be addressed by base diets alone. Treats and snacks benefit from daily-use dental products endorsed by the Veterinary Oral Health Council, reinforcing loyalty to fortified regimens. Wet food's projected significant CAGR growth is underpinned by new capacity, such as the USD 85 million Brazilian plant Mars opened in 2025.

The fortified pet food market share commanded by functional supplements is likely to expand as owners layer chewables and toppers onto kibble, reflecting an unbundling of nutrition. Regulatory clarity under the 2024 labeling rules, which separate complete diets from supplements, should filter out exaggerated claims and steer spending toward clinically backed products. Dry food is unlikely to disappear, yet future success will hinge on palatability upgrades and microencapsulated inclusions that keep the segment relevant for value-conscious shoppers.

Dog held the largest share, accounting for 58.0% of the fortified pet food market in 2025, though obesity management formulas are showing faster momentum than general canine kibble. The cat segment has recorded a significant share, but rising apartment living and targeted urinary or hairball solutions are driving the fortified pet food market for feline offerings to grow at the fastest rate, with a 10.4% CAGR through 2026-2031. Others, covering small mammals and exotics, remain a sub-1% niche yet draw high spend per kilogram from dedicated owners.

Veterinary advocacy regarding feline-specific nutritional needs is contributing to the introduction of premium wet food and probiotic products aimed at addressing common health issues in indoor cats. Companies that integrate veterinary education efforts with online subscription-based distribution models are well-positioned to expand their market share. Meanwhile, canine-focused brands must enhance their product portfolios in areas such as dental care, mobility support, and weight management to maintain competitiveness. Failure to do so may result in increased investment in shelf space, product development, and innovation being directed toward the faster-growing feline segment within the fortified pet food market.

Complete Report Scope:

- By Product Type

- Dry Food

- Wet Food

- Treats and Snacks

- Functional Supplements

- Others

- By Pet Type

- Dog

- Cat

- Others

- By Fortificant

- Vitamin Enriched

- Mineral Enriched

- Probiotic Fortified

- Omega-3 Fortified

- Multi-functional Blend

- By Distribution Channel

- Supermarkets and Hypermarkets

- Specialty Pet Stores

- Veterinary Clinics

- Online Retail

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America retained the largest market share at 35% of 2025 revenue, supported by high per-pet spending and entrenched veterinary endorsement programs. Capacity additions such as Mars's USD 450 million Royal Canin plant in Ohio and Nestle Purina's USD 195 million Wisconsin upgrade expand therapeutic diet output and bolster supply resilience. Asia-Pacific is the fastest region, forecast to advance at an 11.8% CAGR over 2026-2031 as e-commerce penetration spreads fortified super-premium formulas into tier-2 and tier-3 cities. Rising disposable incomes and urban pet ownership in China and India reinforce the momentum of premiumization and drive greater uptake of functional supplements.

Europe is experiencing steady growth, supported by sustainability-focused consumers in Germany, the United Kingdom, and France. Additionally, the regulatory oversight of the European Food Safety Authority enhances claim credibility and promotes the development of scientifically formulated products. In South America, growth is driven by Brazil's expanding middle class and the establishment of Mars's new wet-food facility in Sao Paulo state, which is fostering the adoption of fortified diets. The Middle East is witnessing improved adoption rates, supported by high per-capita income in Saudi Arabia and the United Arab Emirates, as well as the ongoing expansion of modern retail channels. In Africa, the market remains underdeveloped. However, urbanization in South Africa and Nigeria is gradually increasing awareness of the advantages of functional pet nutrition.

Collectively, these regional dynamics diversify revenue streams and cushion suppliers against localized economic shocks. Manufacturing investments in high-demand geographies shorten lead times and reduce foreign-exchange exposure, supporting further expansion of the fortified pet food market. Digital platforms that transcend brick-and-mortar limitations allow brands to harmonize product launches and marketing across continents. As clinical validation of functional ingredients gains global visibility, each region is projected to deepen its contribution to overall category growth through 2031.

List of Companies Covered in this Report:

- Mars, Incorporated

- Nestle Purina PetCare (Nestle S.A.)

- Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company)

- Blue Buffalo Pet Products, Inc. (General Mills, Inc.)

- United Pet Group, Inc. (Spectrum Brands Holdings, Inc.)

- Archer-Daniels-Midland Company

- Diamond Pet Foods, Inc. (Schell & Kampeter, Inc.)

- Sunshine Mills, Inc.

- Tiernahrung Deuerer GmbH

- Wellness Pet Company (Clearlake Capital Group, L.P.)

- Freshpet, Inc.

- Simmons Pet Food, Inc. (Simmons Foods, Inc.)

- ITail Corporation PCL (Thai Union Group PCL)

- Farmina Pet Foods Holding B.V.

- Heristo Aktiengesellschaft

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumization of pet diets

- 4.2.2 Humanization trend in emerging markets

- 4.2.3 Advancements in nutrient-microencapsulation

- 4.2.4 Veterinary endorsement programs

- 4.2.5 Rise of DNA-based personalized pet nutrition

- 4.2.6 Expansion of insect-based fortified proteins

- 4.3 Market Restraints

- 4.3.1 Volatility in specialty micronutrient costs

- 4.3.2 Stringent fortification-labeling regulations

- 4.3.3 Limited shelf-life perception of probiotic formats

- 4.3.4 Ethical concerns around novel protein sources

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Dry Food

- 5.1.2 Wet Food

- 5.1.3 Treats and Snacks

- 5.1.4 Functional Supplements

- 5.1.5 Others

- 5.2 By Pet Type

- 5.2.1 Dog

- 5.2.2 Cat

- 5.2.3 Others

- 5.3 By Fortificant

- 5.3.1 Vitamin Enriched

- 5.3.2 Mineral Enriched

- 5.3.3 Probiotic Fortified

- 5.3.4 Omega-3 Fortified

- 5.3.5 Multi-functional Blend

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets and Hypermarkets

- 5.4.2 Specialty Pet Stores

- 5.4.3 Veterinary Clinics

- 5.4.4 Online Retail

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Mars, Incorporated

- 6.4.2 Nestle Purina PetCare (Nestle S.A.)

- 6.4.3 Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company)

- 6.4.4 Blue Buffalo Pet Products, Inc. (General Mills, Inc.)

- 6.4.5 United Pet Group, Inc. (Spectrum Brands Holdings, Inc.)

- 6.4.6 Archer-Daniels-Midland Company

- 6.4.7 Diamond Pet Foods, Inc. (Schell & Kampeter, Inc.)

- 6.4.8 Sunshine Mills, Inc.

- 6.4.9 Tiernahrung Deuerer GmbH

- 6.4.10 Wellness Pet Company (Clearlake Capital Group, L.P.)

- 6.4.11 Freshpet, Inc.

- 6.4.12 Simmons Pet Food, Inc. (Simmons Foods, Inc.)

- 6.4.13 ITail Corporation PCL (Thai Union Group PCL)

- 6.4.14 Farmina Pet Foods Holding B.V.

- 6.4.15 Heristo Aktiengesellschaft

7 Market Opportunities and Future Outlook