PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073235

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073235

Africa Pet Food - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

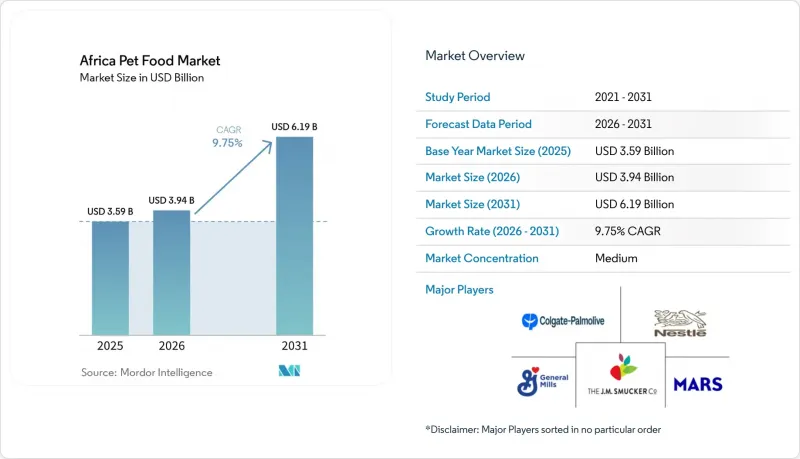

According to Mordor Intelligence, the africa pet food market size is projected to grow from USD 3.59 billion in 2025 to USD 3.94 billion in 2026 and is forecast to reach USD 6.19 billion by 2031 at 9.75% CAGR over 2026-2031.

This report is Segmented by Pet Food Product (Food, Pet Nutraceuticals/Supplements, and More), by Pets (Cats, Dogs, and Other Pets), by Distribution Channel (Convenience Stores, Online Channel, and More), and Geography (South Africa and Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Africa Pet Food Market Trends and Insights

Rising Pet Humanization and Premium Nutrition Demand

The Africa pet food market is being reshaped by a steady shift in how urban households think about animal care and daily feeding. Pet ownership is moving closer to a family-care model in larger cities, which is boosting interest in branded diets, higher-quality ingredients, clearer labels, and products tailored to age, condition, and lifestyle. This change matters because it supports repeat purchasing behavior, not just occasional trade-up buying, and that gives the Africa pet food market a stronger base for sustained growth. The same pattern is also helping premium dry food, functional treats, and targeted formulas gain visibility even when overall household budgets remain tight, because pet nutrition is becoming a more deliberate spend rather than a casual add-on. In practice, companies that explain product benefits clearly and align them with digestive support, skin health, and life-stage needs are better placed to gain traction as the Africa pet food market matures. Formal labeling and ingredient disclosure remain important trust signals in this shift, especially in South Africa's organized retail system.

Expansion of Modern Retail and Specialty Pet Channels

The Africa pet food market is also benefiting from a broader shift in how products are sold, displayed, and replenished across formal trade. Supermarkets are treating pet food as a more defined destination category, which improves visibility, range depth, and pack-size choice for shoppers who want both entry-level and premium options. Specialty retail is adding another layer to the Africa pet food market because it can carry therapeutic diets, supplements, and niche products that general trade often cannot support at scale. This matters for category development because better shelf presentation and stronger in-store advice tend to reduce consumer hesitation and encourage migration from informal feeding to packaged diets. In South Africa, the scale of specialist retail has already created a stronger premium ecosystem, with Absolute Pets operating more than 200 stores and helping extend access to higher-value categories across multiple urban locations. That retail depth gives the Africa pet food market a clearer path to premiumization than would be possible through fragmented neighborhood trade alone.

High Price Sensitivity Outside Premium Urban Clusters

Price remains the biggest barrier to wider adoption of packaged food across the Africa pet food market. Commercial diets are well established in the main urban centers, but the Africa pet food market still depends on converting a much larger base of owners who continue to feed pets with household food or low-cost informal alternatives. This challenge is sharper outside the main metropolitan clusters, where consumers have less room for trade-up spending and often buy in small quantities, constrained by strict daily budget limits. In Nigeria, the reported rise in the price of a 15 kg bag of dog food from NGN 40,000 to NGN 70,000, or from USD 25 to USD 44, shows how quickly affordability can narrow when local currencies weaken, or input costs rise. The practical result is that brands that rely too heavily on imported premium formulas face a narrower addressable base in the Africa pet food market than topline pet ownership would suggest. Companies that build economy dry food lines with local inputs and relevant pack sizes are more likely to unlock broader adoption.

Other drivers and restraints analyzed in the detailed report include:

- Local Manufacturing and Import Substitution in Key Hubs

- Functional Diets for Health, Weight, and Skin Support

- Limited Cold Chain and Logistics Coverage for Moist and Fresh Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Food held 73.6% market share in the Africa pet food market in 2025, and that leadership reflects the basic commercial feeding pattern seen across most countries on the continent. Dry food, especially kibble, remains the largest format because it is affordable, easy to transport, and suitable for retail systems that range from formal supermarkets to smaller neighborhood outlets. Wet food is present in premium urban channels, especially in South Africa, but its reach is still much narrower because storage and logistics requirements are more demanding. Treats are growing as owners look for products tied to training, bonding, and occasional indulgence, and that is widening shelf variety in organized trade. Nutraceuticals and supplements are also gaining space in the Africa pet food industry as vet guidance and health-led positioning make owners more comfortable with functional add-ons, while local product innovation, such as game meat treats, gives South African brands a distinct point of difference.

The Africa pet food market size for pet veterinary diets is set to grow fastest at a 11.7% CAGR through 2031, underscoring how quickly health-led feeding is becoming a serious premium category rather than a narrow clinic-only niche. Demand is strongest in formulas linked to skin issues, digestion, weight control, renal care, and urinary health, because these are conditions owners can understand and monitor with veterinary support. Colgate-Palmolive Company, through Hill's Pet Nutrition Inc., and Nestle S.A., through Purina, retain strong positions here because clinic distribution and professional trust are harder for newer entrants to replicate quickly. South Africa's regulatory environment also shapes the segment, as products sold through formal channels must meet labeling and feed compliance requirements, which raise the entry bar for companies without strong regulatory resources. That makes veterinary diets one of the clearest examples of how the Africa pet food market is moving up the value ladder, even while mass-market affordability remains important.

Complete Report Scope:

- Pet Food Product

- Food

- By Sub Product

- Dry Pet Food

- By Sub Dry Pet Food

- Kibbles

- Other Dry Pet Food

- By Sub Dry Pet Food

- Wet Pet Food

- Dry Pet Food

- By Sub Product

- Pet Nutraceuticals/Supplements

- By Sub Product

- Milk Bioactives

- Omega-3 Fatty Acids

- Probiotics

- Proteins and Peptides

- Vitamins and Minerals

- Other Nutraceuticals

- By Sub Product

- Pet Treats

- By Sub Product

- Crunchy Treats

- Dental Treats

- Freeze-dried and Jerky Treats

- Soft And Chewy Treats

- Other Treats

- By Sub Product

- Pet Veterinary Diets

- By Sub Product

- Derma Diets

- Diabetes

- Digestive Sensitivity

- Obesity Diets

- Oral Care Diets

- Renal

- Urinary tract disease

- Other Veterinary Diets

- By Sub Product

- Food

- Pets

- Cats

- Dogs

- Other Pets

- Distribution Channel

- Convenience Stores

- Online Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Other Channels

- Geography

- South Africa

- Rest of Africa

List of Companies Covered in this Report:

- Wellness Pet Company Inc. (Clearlake Capital Group, L.P.)

- Hill's Pet Nutrition Inc. (Colgate-Palmolive Company)

- Affinity Petcare S.A (Agrolimen S.A.)

- Farmina Pet Foods (Russo Mangimi)

- General Mills Inc.

- Mars Incorporated

- Nestle S.A. (Purina)

- Schell & Kampeter Inc. (Diamond Pet Foods)

- Virbac S.A.

- Symply Pet Food Limited

- Burgess Pet Care Group plc

- PLB International

- The J.M. Smucker Company

- Inspired Pet Nutrition Limited (Dalton Bidco Limited)

- Monge and C. S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions And Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Consumer Trends

5 SUPPLY AND PRODUCTION DYNAMICS

- 5.1 Trade Analysis

- 5.2 Ingredient Trends

- 5.3 Value Chain And Distribution Channel Analysis

- 5.4 Regulatory Framework

- 5.5 Market Drivers

- 5.5.1 Rising pet humanization and premium nutrition demand

- 5.5.2 Expansion of modern retail and specialty pet channels

- 5.5.3 Local manufacturing and import substitution in key hubs

- 5.5.4 Functional diets for health, weight, and skin support

- 5.5.5 Informal feeding conversion into packaged pet food

- 5.5.6 E-commerce and direct-to-consumer brand reach

- 5.6 Market Restraints

- 5.6.1 High price sensitivity outside premium urban clusters

- 5.6.2 Weak online penetration in most African markets

- 5.6.3 Fragmented regulation and labeling compliance across countries

- 5.6.4 Limited cold chain and logistics coverage for moist and fresh formats

6 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 6.1 Pet Food Product

- 6.1.1 Food

- 6.1.1.1 By Sub Product

- 6.1.1.1.1 Dry Pet Food

- 6.1.1.1.1.1 By Sub Dry Pet Food

- 6.1.1.1.1.1.1 Kibbles

- 6.1.1.1.1.1.2 Other Dry Pet Food

- 6.1.1.1.1.1 By Sub Dry Pet Food

- 6.1.1.1.2 Wet Pet Food

- 6.1.1.1.1 Dry Pet Food

- 6.1.1.1 By Sub Product

- 6.1.2 Pet Nutraceuticals/Supplements

- 6.1.2.1 By Sub Product

- 6.1.2.1.1 Milk Bioactives

- 6.1.2.1.2 Omega-3 Fatty Acids

- 6.1.2.1.3 Probiotics

- 6.1.2.1.4 Proteins and Peptides

- 6.1.2.1.5 Vitamins and Minerals

- 6.1.2.1.6 Other Nutraceuticals

- 6.1.2.1 By Sub Product

- 6.1.3 Pet Treats

- 6.1.3.1 By Sub Product

- 6.1.3.1.1 Crunchy Treats

- 6.1.3.1.2 Dental Treats

- 6.1.3.1.3 Freeze-dried and Jerky Treats

- 6.1.3.1.4 Soft And Chewy Treats

- 6.1.3.1.5 Other Treats

- 6.1.3.1 By Sub Product

- 6.1.4 Pet Veterinary Diets

- 6.1.4.1 By Sub Product

- 6.1.4.1.1 Derma Diets

- 6.1.4.1.2 Diabetes

- 6.1.4.1.3 Digestive Sensitivity

- 6.1.4.1.4 Obesity Diets

- 6.1.4.1.5 Oral Care Diets

- 6.1.4.1.6 Renal

- 6.1.4.1.7 Urinary tract disease

- 6.1.4.1.8 Other Veterinary Diets

- 6.1.4.1 By Sub Product

- 6.1.1 Food

- 6.2 Pets

- 6.2.1 Cats

- 6.2.2 Dogs

- 6.2.3 Other Pets

- 6.3 Distribution Channel

- 6.3.1 Convenience Stores

- 6.3.2 Online Channel

- 6.3.3 Specialty Stores

- 6.3.4 Supermarkets/Hypermarkets

- 6.3.5 Other Channels

- 6.4 Geography

- 6.4.1 South Africa

- 6.4.2 Rest of Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Key Strategic Moves

- 7.2 Market Share Analysis

- 7.3 Brand Positioning Matrix

- 7.4 Market Claim Analysis

- 7.5 Company Landscape

- 7.6 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 7.6.1 Wellness Pet Company Inc. (Clearlake Capital Group, L.P.)

- 7.6.2 Hill's Pet Nutrition Inc. (Colgate-Palmolive Company)

- 7.6.3 Affinity Petcare S.A (Agrolimen S.A.)

- 7.6.4 Farmina Pet Foods (Russo Mangimi)

- 7.6.5 General Mills Inc.

- 7.6.6 Mars Incorporated

- 7.6.7 Nestle S.A. (Purina)

- 7.6.8 Schell & Kampeter Inc. (Diamond Pet Foods)

- 7.6.9 Virbac S.A.

- 7.6.10 Symply Pet Food Limited

- 7.6.11 Burgess Pet Care Group plc

- 7.6.12 PLB International

- 7.6.13 The J.M. Smucker Company

- 7.6.14 Inspired Pet Nutrition Limited (Dalton Bidco Limited)

- 7.6.15 Monge and C. S.p.A.

8 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS