PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072874

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072874

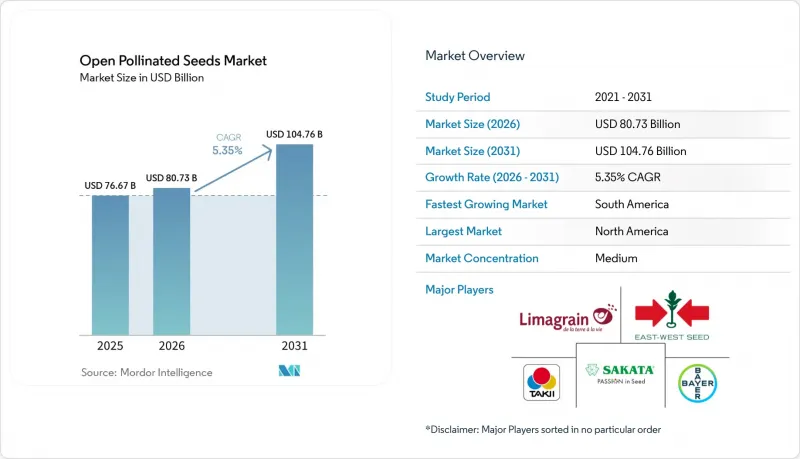

Open Pollinated Seeds - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the open pollinated seeds market was valued at USD 76.67 billion in 2025 and is projected to grow from USD 80.73 billion in 2026 to USD 104.76 billion by 2031, at a CAGR of 5.35% during the forecast period from 2026 to 2031.

This report is Segmented by Breeding Technology (Hybrids and Open Pollinated Varieties and Hybrid Derivatives), by Crop Type (Row Crops and Vegetables), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Global Open Pollinated Seeds Market Trends and Insights

Rising Demand for Organic and Heirloom Produce

Consumer preference for organic and heirloom produce is bolstering the open pollinated seeds market, elevating the commercial value of traditional and organically bred crop varieties. This trend gained further momentum in April 2024, when the European Parliament adopted its position on the proposed Plant Reproductive Material (PRM) regulation. The new provisions ease the marketing and exchange of conservation varieties and organic heterogeneous material. This reform is poised to enhance market access for diverse open-pollinated cultivars, prized for their genetic diversity, local adaptation, and distinct product characteristics. With retailers and organic producers on the lookout for differentiated crop varieties, these regulatory shifts are solidifying the long-term demand for open pollinated seeds throughout Europe.

Seed-Saving Economics for Smallholder Farmers

Smallholder farmers, aiming to cut production costs, are increasingly turning to open-pollinated seeds, primarily due to the ability to save and reuse these seeds. A study published in the Food Security journal in March 2026 highlights that population-based cultivars, akin to open-pollinated varieties, offer an economical breeding strategy for resource-limited farming. These cultivars demonstrate consistent performance across varied agroecological settings. While hybrids necessitate repeated purchases, open-pollinated varieties empower farmers to save seeds for subsequent planting cycles. This not only enhances affordability but also boosts adoption rates among small-scale producers. Such economic benefits are bolstering the sustained demand for open-pollinated seeds, especially in developing agricultural regions.

Lower Yield Ceiling versus Hybrid Seeds

Farmers, especially in commercial production systems where output directly impacts profitability, often prioritize yield maximization. As a result, they frequently opt for hybrid varieties, drawn by their higher yield potential, uniformity, and responsiveness to intensive management. This preference not only attracts investments from growers and seed companies but also curtails the adoption of open-pollinated seeds in high-productivity systems. The Food and Agriculture Organization of the United Nations reports that hybrid maize seeds dominate, covering over 60% of the global maize area. This underscores the strong inclination towards hybrid genetics in one of the world's largest seed markets, intensifying the competitive pressure on open-pollinated varieties and stifling the growth of the open-pollinated seeds market.

Other drivers and restraints analyzed in the detailed report include:

- Need for Climate-Resilient Locally Adapted Varieties

- Expansion of Regenerative and Low-Input Farming Systems

- Seed-Health and Phytosanitary Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The open pollinated seeds market share for the hybrid segment was the largest 73.1% in 2025, reflecting the strong preference for high-yielding and uniform seed varieties across commercial agriculture. Hybrids dominate major field crops due to their enhanced productivity, consistency, and adaptability to modern farming systems. This dominance is driven by continuous advancements in breeding, improved disease resistance, and compatibility with mechanized farming practices. Commercial growers increasingly view hybrid seed purchases as a critical production input, sustaining demand and reinforcing the segment's leading position in both developed and emerging agricultural markets.

The hybrid market size is forecast to grow at the fastest CAGR of 5.5% from 2026 to 2031, supported by ongoing advances in breeding technologies and the introduction of improved crop genetics. The expansion of hybrid development into additional crop categories is broadening their commercial significance beyond traditional applications. Seed companies are investing in breeding programs to enhance stress tolerance, yield stability, and agronomic performance. Meanwhile, open-pollinated varieties remain significant in seed-saving systems, localized farming practices, and organic production, creating a balanced market structure that supports both commercial innovation and farmer diversity.

Complete Report Scope:

- Breeding Technology

- Hybrids

- Non-Transgenic Hybrids

- Transgenic Hybrids

- Insect Resistant Hybrids

- Open Pollinated Varieties and Hybrid Derivatives

- Hybrids

- By Crop Type

- Row Crops

- Fiber Crops

- Cotton

- Other Fiber Crops

- Forage Crops

- Alfalfa

- Forage Corn

- Forage Sorghum

- Other Forage Crops

- Grains and Cereals

- Corn

- Rice

- Sorghum

- Wheat

- Other Grains and Cereals

- Oilseeds

- Canola, Rapeseed and Mustard

- Soybean

- Sunflower

- Other Oilseeds

- Pulses

- Fiber Crops

- Vegetables

- Brassicas

- Cabbage

- Cauliflower and Broccoli

- Other Brassicas

- Cucurbits

- Cucumber and Gherkin

- Pumpkin and Squash

- Other Cucurbits

- Roots and Bulbs

- Garlic

- Onion

- Potato

- Other Roots and Bulbs

- Solanaceae

- Chilli

- Eggplant

- Tomato

- Other Solanaceae

- Unclassified Vegetables

- Asparagus

- Lettuce

- Okra

- Peas

- Spinach

- Other Unclassified Vegetables

- Brassicas

- Row Crops

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- Italy

- Spain

- United Kingdom

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Thailand

- Philippines

- Indonesia

- Australia

- Rest of Asia-Pacific

- Middle East

- Iran

- Turkey

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Tanzania

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held the largest 35.2% revenue share in 2025, supported by advanced seed technology adoption, strong commercial farming systems, and extensive investment in crop breeding. The region benefits from well-established seed replacement practices and a highly developed agricultural value chain that encourages continuous adoption of improved varieties. Farmers increasingly utilize advanced genetics to improve productivity, resilience, and profitability across major crops. Strong research capabilities, extensive distribution networks, and ongoing product innovation continue to reinforce North America's leadership position in the global seed industry and support sustained market demand.

South America is forecast to grow at the fastest CAGR of 6.3% from 2026 to 2031, driven by expanding cultivation areas, rising adoption of improved seed varieties, and increasing agricultural exports. Countries across the region continue to invest in modern farming practices that support higher yields and better crop performance. Seed companies are strengthening their presence through breeding programs tailored to local growing conditions and evolving farmer requirements. The combination of favorable agricultural resources, expanding commercial production, and growing technology adoption continues to create attractive opportunities for seed industry expansion throughout the region.

Africa and the Middle East are becoming increasingly important growth regions as governments and agricultural organizations prioritize productivity improvements and seed system development. According to the United States Department of Agriculture Economic Research Service, more than 90% of corn, soybean, and cotton acreage in the United States utilized genetically engineered varieties in 2025, demonstrating the continuing importance of advanced breeding technologies in commercial agriculture. Similar efforts to improve seed quality, varietal performance, and farmer access are supporting modernization initiatives across emerging agricultural economies and encouraging broader adoption of improved seed varieties.

- Groupe Limagrain Holding

- East-West Seed International Ltd.

- Takii & Co., Ltd.

- Sakata Seed Corporation

- Rijk Zwaan Zaadteelt en Zaadhandel B.V.

- Bejo Zaden B.V.

- KWS SAAT SE & Co. KGaA

- Bayer AG

- Namdhari Seeds Pvt Ltd.

- Syngenta Crop Protection AG (Syngenta Group)

- Enza Zaden Beheer B.V.

- DLF Seeds A/S (DLF amba)

- RAGT Semences SAS (RAGT SA)

- Nongwoo Bio Co., Ltd. (NongHyup Group)

- Beidahuang Kenfeng Seed Co., Ltd. (Beidahuang Agribusiness Group Co., Ltd.)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.1.2 Vegetables

- 4.2 Most Popular Traits

- 4.2.1 Cabbage and Onion

- 4.2.2 Rice and Corn

- 4.2.3 Tomato and Chilli

- 4.2.4 Wheat and Cotton

- 4.3 Breeding Techniques

- 4.3.1 Row Crops and Vegetables

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Rising demand for organic and heirloom produce

- 4.6.2 Seed-saving economics for smallholder farmers

- 4.6.3 Need for climate-resilient locally adapted varieties

- 4.6.4 Expansion of regenerative and low-input farming systems

- 4.6.5 European Union organic seed derogation phaseout to 2036

- 4.6.6 Participatory breeding and farmer-led trial platforms

- 4.7 Market Restraints

- 4.7.1 Lower yield ceiling versus hybrid seeds

- 4.7.2 Lower private R and D intensity than hybrid-led categories

- 4.7.3 Pollinator-dependent seed production risk

- 4.7.4 Seed-health and phytosanitary compliance burden

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Insect Resistant Hybrids

- 5.1.2 Open Pollinated Varieties and Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 By Crop Type

- 5.2.1 Row Crops

- 5.2.1.1 Fiber Crops

- 5.2.1.1.1 Cotton

- 5.2.1.1.2 Other Fiber Crops

- 5.2.1.2 Forage Crops

- 5.2.1.2.1 Alfalfa

- 5.2.1.2.2 Forage Corn

- 5.2.1.2.3 Forage Sorghum

- 5.2.1.2.4 Other Forage Crops

- 5.2.1.3 Grains and Cereals

- 5.2.1.3.1 Corn

- 5.2.1.3.2 Rice

- 5.2.1.3.3 Sorghum

- 5.2.1.3.4 Wheat

- 5.2.1.3.5 Other Grains and Cereals

- 5.2.1.4 Oilseeds

- 5.2.1.4.1 Canola, Rapeseed and Mustard

- 5.2.1.4.2 Soybean

- 5.2.1.4.3 Sunflower

- 5.2.1.4.4 Other Oilseeds

- 5.2.1.5 Pulses

- 5.2.1.1 Fiber Crops

- 5.2.2 Vegetables

- 5.2.2.1 Brassicas

- 5.2.2.1.1 Cabbage

- 5.2.2.1.2 Cauliflower and Broccoli

- 5.2.2.1.3 Other Brassicas

- 5.2.2.2 Cucurbits

- 5.2.2.2.1 Cucumber and Gherkin

- 5.2.2.2.2 Pumpkin and Squash

- 5.2.2.2.3 Other Cucurbits

- 5.2.2.3 Roots and Bulbs

- 5.2.2.3.1 Garlic

- 5.2.2.3.2 Onion

- 5.2.2.3.3 Potato

- 5.2.2.3.4 Other Roots and Bulbs

- 5.2.2.4 Solanaceae

- 5.2.2.4.1 Chilli

- 5.2.2.4.2 Eggplant

- 5.2.2.4.3 Tomato

- 5.2.2.4.4 Other Solanaceae

- 5.2.2.5 Unclassified Vegetables

- 5.2.2.5.1 Asparagus

- 5.2.2.5.2 Lettuce

- 5.2.2.5.3 Okra

- 5.2.2.5.4 Peas

- 5.2.2.5.5 Spinach

- 5.2.2.5.6 Other Unclassified Vegetables

- 5.2.2.1 Brassicas

- 5.2.1 Row Crops

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 Italy

- 5.3.3.4 Spain

- 5.3.3.5 United Kingdom

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Thailand

- 5.3.4.5 Philippines

- 5.3.4.6 Indonesia

- 5.3.4.7 Australia

- 5.3.4.8 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Iran

- 5.3.5.2 Turkey

- 5.3.5.3 Saudi Arabia

- 5.3.5.4 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Tanzania

- 5.3.6.3 Nigeria

- 5.3.6.4 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Groupe Limagrain Holding

- 6.4.2 East-West Seed International Ltd.

- 6.4.3 Takii & Co., Ltd.

- 6.4.4 Sakata Seed Corporation

- 6.4.5 Rijk Zwaan Zaadteelt en Zaadhandel B.V.

- 6.4.6 Bejo Zaden B.V.

- 6.4.7 KWS SAAT SE & Co. KGaA

- 6.4.8 Bayer AG

- 6.4.9 Namdhari Seeds Pvt Ltd.

- 6.4.10 Syngenta Crop Protection AG (Syngenta Group)

- 6.4.11 Enza Zaden Beheer B.V.

- 6.4.12 DLF Seeds A/S (DLF amba)

- 6.4.13 RAGT Semences SAS (RAGT SA)

- 6.4.14 Nongwoo Bio Co., Ltd. (NongHyup Group)

- 6.4.15 Beidahuang Kenfeng Seed Co., Ltd. (Beidahuang Agribusiness Group Co., Ltd.)

7 KEY STRATEGIC QUESTIONS FOR FEED ADDITIVE CEOS