PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073592

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073592

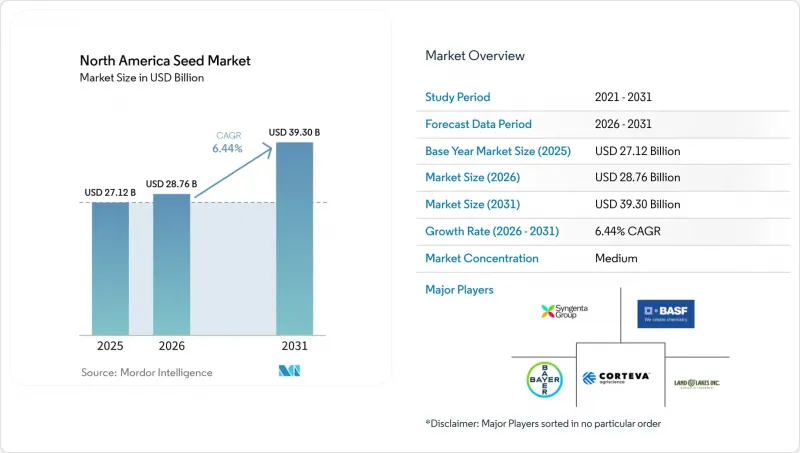

North America Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america seed market size is projected to expand from USD 27.1 billion in 2025 and USD 28.8 billion in 2026 to USD 39.2 billion by 2031, registering a CAGR of 6.3% between 2026 to 2031.

This report is Segmented by Breeding Technology (Hybrids and Open Pollinated Varieties and Hybrid Derivatives), by Cultivation Mechanism (Open Field and Protected Cultivation), by Crop Type (Row Crops and Vegetables), and by Geography (Canada, Mexico, United States, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

North America Seed Market Trends and Insights

Yield Improvements with Advanced Transgenic Hybrids

Multi-trait stacking remains the strongest value driver in the North America seed market, especially across corn and soybeans. According to the United States Department of Agriculture (USDA), 87% of cotton acres and 84% of corn acres were planted with stacked seeds in 2025. This replacement cycle is tied to clear field performance, which supports premium pricing when yield and protection gains are visible season after season. The premium pricing is supported by the yield advantage, which helps sustain grower margins despite fluctuating commodity prices. Furthermore, multi-mode insect protection minimizes the need for refuge areas, streamlining field operations.

Biofuel Feedstock Acreage Support for Corn and Soybean Seed Demand

Renewable fuel policy is one of the most durable acreage supports for the North America seed market. In the United States, policy support, such as the Renewable Fuel Standard (RFS) and rising mandates for renewable diesel, are encouraging greater use of corn for ethanol and soybean oil for biodiesel. The United States Department of Agriculture (USDA) Economic Research Service projected soybean oil use for biomass-based diesel at 13.9 billion pounds in 2025, a 6% increase from the prior year's revised estimate, signaling stronger demand for oilseed-oriented genetics. This has strengthened demand for both crops, leading farmers to maintain or expand planted acreage. Recent analyses show that biofuel policies are projected to be a critical factor absorbing growing corn and soybean supplies and supporting farm-level prices, especially as yield improvements continue to increase output per acre.

Trait-Stack Approval and Stewardship Delays

Regulatory timelines still slow parts of the North America seed market, especially for stacked biotech products that need coordinated review across the Animal and Plant Health Inspection Service (APHIS), Environmental Protection Agency (EPA), and Food and Drug Administration (FDA). The process became less predictable after a United States District Court vacated the United States Department of Agriculture (USDA) 2020 final rule on Genetically Engineered organisms (GE) organisms in December 2024, which forced Animal and Plant Health Inspection Service (APHIS) to restore older permitting, notification, and petition processes. Canada adds another review layer through its Plant with Novel Traits process, and United States Department of Agriculture (USDA) Foreign Agricultural Service reported 103 submissions and 261 field trials in 2024. These parallel reviews lengthen commercialization timelines and reduce launch flexibility across the North America seed market.

Other drivers and restraints analyzed in the detailed report include:

- Precision Seeding and Hybrid Prescription Adoption

- Protected Cultivation Lift for Premium Vegetable Seed Demand

- Farm-Saved Seed Pressure in Pulses and Forage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrids are the largest segment, 81.7% of the North America seed market share in 2025, and also the fastest-growing segment, forecast to grow at a 6.6% CAGR through 2026 to 2031. Within transgenic hybrids, herbicide-tolerant lines continue to lead in spending, while insect-resistant and stacked-trait packages offer the highest premium potential in crops such as corn, soybean, canola, and cotton. Open-pollinated varieties and hybrid derivatives remain significant in forage, pulse, and specialty grains, where farm-saved seed retains commercial relevance. This division highlights the concentration of the North America seed industry in row crops, while lower-barrier categories exhibit a more diverse market structure.

In North America, the market for open-pollinated (OP) varieties and hybrid derivatives in seeds represents a significant segment of the broader seed industry, particularly for crops such as corn, soybean, vegetables, and specialty horticultural crops. Large commercial farms predominantly prefer hybrid seeds due to their productivity benefits, while OP varieties maintain niche demand in areas such as organic farming, local food systems, and specialty vegetable production. Hybrid derivatives are increasingly being developed with advanced traits, including drought tolerance, herbicide resistance, and enhanced oil or protein content, further solidifying their prominence in the North American seed market.

Complete Report Scope:

- By Breeding Technology

- Hybrids

- Non-Transgenic Hybrids

- Transgenic Hybrids

- Herbicide Tolerant Hybrids

- Insect Resistant Hybrids

- Other Traits

- Open Pollinated Varieties and Hybrid Derivatives

- Hybrids

- By Cultivation Mechanism

- Open Field

- Protected Cultivation

- By Crop Type

- Row Crops

- Fiber Crops

- Cotton

- Other Fiber Crops

- Forage Crops

- Alfalfa

- Forage Corn

- Forage Sorghum

- Other Forage Crops

- Grains and Cereals

- Corn

- Rice

- Sorghum

- Wheat

- Other Grains and Cereals

- Oilseeds

- Canola, Rapeseed and Mustard

- Soybean

- Sunflower

- Other Oilseeds

- Pulses

- Fiber Crops

- Vegetables

- Brassicas

- Cabbage

- Cauliflower and Broccoli

- Other Brassicas

- Cucurbits

- Cucumber and Gherkin

- Pumpkin and Squash

- Other Cucurbits

- Roots and Bulbs

- Garlic

- Onion

- Potato

- Other Roots and Bulbs

- Solanaceae

- Chilli

- Eggplant

- Tomato

- Other Solanaceae

- Unclassified Vegetables

- Asparagus

- Lettuce

- Okra

- Peas

- Spinach

- Carrot

- Other Unclassified Vegetables

- Brassicas

- Row Crops

- By Geography

- Canada

- Mexico

- United States

- Rest of North America

List of Companies Covered in this Report:

- Corteva Agriscience

- Bayer AG

- Land O'Lakes, Inc.

- Syngenta Group

- BASF SE

- KWS SAAT SE & Co. KGaA

- Sakata Seed Corporation

- Groupe Limagrain Holding S.A.

- FMC Corporation

- DLF A/S

- Rijk Zwaan Zaadteelt en Zaadhandel B.V.

- Enza Zaden Holding B.V.

- Beck's Superior Hybrids, Inc.

- Stine Seed Company

- GROWMARK, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 Executive Summary and Key Findings

3 Report Offers

4 Key Industry Trends

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.1.2 Vegetables

- 4.2 Most Popular Traits

- 4.2.1 Alfalfa and Cotton

- 4.2.2 Cucumber and Cabbage

- 4.2.3 Rice and Corn

- 4.2.4 Tomato and Onion

- 4.2.5 Wheat and Soybean

- 4.3 Breeding Techniques

- 4.3.1 Row Crops and Vegetables

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Yield Improvements with Advanced Transgenic Hybrids

- 4.6.2 Biofuel Feedstock Acreage Support for Corn and Soybean Seed Demand

- 4.6.3 Precision Seeding and Hybrid Prescription Adoption

- 4.6.4 Protected Cultivation Lift for Premium Vegetable Seed Demand

- 4.6.5 Identity-Preserved and High-Oleic Specialty Crop Programs

- 4.6.6 Biological Seed-Treatment Bundling Around Premium Genetics

- 4.7 Market Restraints

- 4.7.1 Trait-Stack Approval and Stewardship Delays

- 4.7.2 Farm-Saved Seed Pressure in Pulses and Forage

- 4.7.3 Corn Rootworm Resistance Eroding Premium Trait Value

- 4.7.4 Dicamba Trait-System Regulatory Volatility

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Insect Resistant Hybrids

- 5.1.1.2.3 Other Traits

- 5.1.2 Open Pollinated Varieties and Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 By Cultivation Mechanism

- 5.2.1 Open Field

- 5.2.2 Protected Cultivation

- 5.3 By Crop Type

- 5.3.1 Row Crops

- 5.3.1.1 Fiber Crops

- 5.3.1.1.1 Cotton

- 5.3.1.1.2 Other Fiber Crops

- 5.3.1.2 Forage Crops

- 5.3.1.2.1 Alfalfa

- 5.3.1.2.2 Forage Corn

- 5.3.1.2.3 Forage Sorghum

- 5.3.1.2.4 Other Forage Crops

- 5.3.1.3 Grains and Cereals

- 5.3.1.3.1 Corn

- 5.3.1.3.2 Rice

- 5.3.1.3.3 Sorghum

- 5.3.1.3.4 Wheat

- 5.3.1.3.5 Other Grains and Cereals

- 5.3.1.4 Oilseeds

- 5.3.1.4.1 Canola, Rapeseed and Mustard

- 5.3.1.4.2 Soybean

- 5.3.1.4.3 Sunflower

- 5.3.1.4.4 Other Oilseeds

- 5.3.1.5 Pulses

- 5.3.1.1 Fiber Crops

- 5.3.2 Vegetables

- 5.3.2.1 Brassicas

- 5.3.2.1.1 Cabbage

- 5.3.2.1.2 Cauliflower and Broccoli

- 5.3.2.1.3 Other Brassicas

- 5.3.2.2 Cucurbits

- 5.3.2.2.1 Cucumber and Gherkin

- 5.3.2.2.2 Pumpkin and Squash

- 5.3.2.2.3 Other Cucurbits

- 5.3.2.3 Roots and Bulbs

- 5.3.2.3.1 Garlic

- 5.3.2.3.2 Onion

- 5.3.2.3.3 Potato

- 5.3.2.3.4 Other Roots and Bulbs

- 5.3.2.4 Solanaceae

- 5.3.2.4.1 Chilli

- 5.3.2.4.2 Eggplant

- 5.3.2.4.3 Tomato

- 5.3.2.4.4 Other Solanaceae

- 5.3.2.5 Unclassified Vegetables

- 5.3.2.5.1 Asparagus

- 5.3.2.5.2 Lettuce

- 5.3.2.5.3 Okra

- 5.3.2.5.4 Peas

- 5.3.2.5.5 Spinach

- 5.3.2.5.6 Carrot

- 5.3.2.5.7 Other Unclassified Vegetables

- 5.3.2.1 Brassicas

- 5.3.1 Row Crops

- 5.4 By Geography

- 5.4.1 Canada

- 5.4.2 Mexico

- 5.4.3 United States

- 5.4.4 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 Corteva Agriscience

- 6.4.2 Bayer AG

- 6.4.3 Land O'Lakes, Inc.

- 6.4.4 Syngenta Group

- 6.4.5 BASF SE

- 6.4.6 KWS SAAT SE & Co. KGaA

- 6.4.7 Sakata Seed Corporation

- 6.4.8 Groupe Limagrain Holding S.A.

- 6.4.9 FMC Corporation

- 6.4.10 DLF A/S

- 6.4.11 Rijk Zwaan Zaadteelt en Zaadhandel B.V.

- 6.4.12 Enza Zaden Holding B.V.

- 6.4.13 Beck's Superior Hybrids, Inc.

- 6.4.14 Stine Seed Company

- 6.4.15 GROWMARK, Inc.

7 Key Strategic Questions for Seeds CEOs