PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072895

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072895

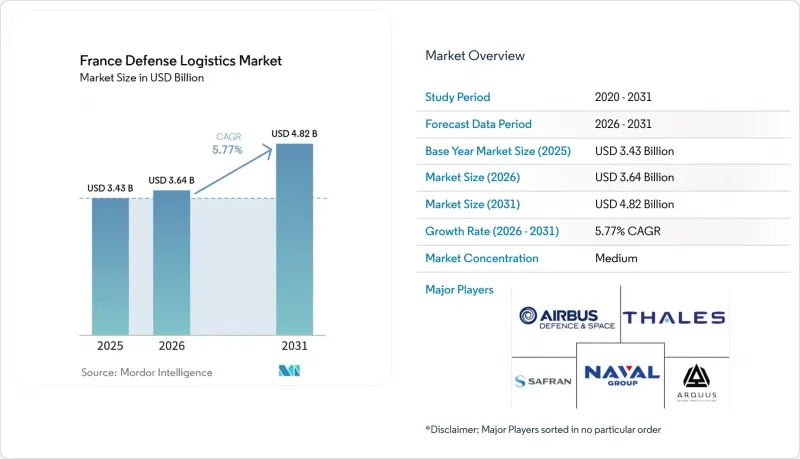

France Defense Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the france defense logistics market size is expected to grow from USD 3.43 billion in 2025 to USD 3.64 billion in 2026 and is forecast to reach USD 4.82 billion by 2031 at 5.77% CAGR over 2026-2031.

This report is Segmented by Service Type (Armament, Military Troops Movement Support, Technical Support & Maintenance, and More), by Logistics Function (Transportation, Warehousing & Distribution, and More), by End User (Army, Air Force, and More), and by Region (Ile-De-France, Auvergne-Rhone-Alpes, Provence-Alpes-Cote D'Azur, Occitanie, and More). The Market Forecasts are Provided in Terms of Value (USD).

France Defense Logistics Market Trends and Insights

Modernization of Strategic Air- and Sea-Lift Fleets

The France defense logistics market is seeing larger service volumes as France renews its strategic lift and support fleets. The French Air and Space Force is moving toward 286 Rafale combat aircraft, and Sabena technics secured a 10-year CAROLUS support contract in December 2025 for the Franco-German C-130J and KC-130J fleet. AFI KLM Engineering and Maintenance also signed a 10-year integrated support contract in December 2025 for France's 4 AWACS aircraft. Longer contract terms are pushing suppliers to hold deeper parts inventories and place support teams closer to operations, shifting more value toward domestic logistics specialists. A400M predictive maintenance results have already shown a 9% increase in available flight hours and a 7% decrease in maintenance hours, which support the wider use of data-linked supply chains in the France defense logistics market.

Outsourcing of SIMMAD and MCO Service Contracts

The France defense logistics market is expanding as military aviation support moves further toward outsourced and bundled service models. France's LPM 2024-2030 allocates EUR 49 billion (USD 56.5 billion) to aeronautical MCO, which is 40% above the prior plan, and directs annual payments of EUR 3 billion (USD 3.5 billion) toward spare parts and outsourced services. DMAe has stated that it will move from verticalized contracts to broader global support contracts from 2028, combining supply chain management, continuing airworthiness, and round-the-clock technical support within fewer commercial relationships. That change raises entry barriers for smaller providers, but it also creates larger contract scopes for companies that can manage full logistics performance. The Cour des comptes also pointed to room for competitiveness gains in current contract structures, suggesting tighter benchmarks and greater risk sharing in future awards.

Budgetary Pressure from Social-Spending Trade-Offs

The France defense logistics market still faces timing pressure between approved budgets and actual contract flow. Politico reported that France did not sign contracts at the pace implied by its war-economy messaging after the start of the Ukraine war, leaving some DTIB companies waiting after they had already invested to increase output. For logistics providers, that gap can delay warehouse, transport, and distribution orders even when top-line defense plans look strong. The effect is strongest on medium-sized subcontractors, because they carry working capital pressure more directly than large primes. France's public debt level above 110% of GDP also keeps supplementary defense disbursements politically sensitive, which can delay realized demand into the forecast period.

Other drivers and restraints analyzed in the detailed report include:

- NATO Readiness Stockpile Mandates

- Predictive-Maintenance Rollout (Plan SICS-SC2)

- Global Raw-Material and Component Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Armament services held 39.77% of the France defense logistics market share in 2025, because ammunition handling, storage, transport, and distribution now sit closer to the center of defense readiness planning. France's munitions buildup and the planned France Munitions procurement platform support sustained demand for ordnance logistics through 2031. Military troops movement, support, technical support, and maintenance form the next tier, supported by logistics fleet renewal and broader integrated MCO activity. Fire-fighting protection and other services remain smaller because they are more closely linked to base support and fixed-site requirements than to field-deployment intensity.

Medical aid and health services are projected to grow at 8.61% CAGR from 2026 to 2031, making it the fastest-growing service line in the France defense logistics market. The Service de sante des armees and the General Directorate for Health signed a joint emergency preparedness charter in October 2025, which formalized civil-military coordination for mass-casualty scenarios. ORION 26 tested medical logistics for up to 250 patients per day over 60 days of sustained operations, underscoring the need for cold-chain drugs, pre-positioned surgical kits, and coordinated evacuation. That leaves the France defense logistics industry with a service niche where demand is rising quickly, but specialist capacity still looks limited.

Complete Report Scope:

- By Service Type

- Armament

- Military Troops Movement Support

- Technical Support & Maintenance

- Medical Aid & Health Services

- Fire-fighting Protection

- Other Services

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing & Distribution

- Value-added Services (Labelling, Kitting, Consulting)

- Transportation

- By End User

- Army

- Navy

- Air Force

- Others

- By Region

- Ile-de-France

- Auvergne-Rhone-Alpes

- Provence-Alpes-Cote d'Azur

- Hauts-de-France

- Nouvelle-Aquitaine

- Occitanie

- Grand Est

- Brittany

- Others

List of Companies Covered in this Report:

- Airbus Defence and Space

- Thales Group

- Safran

- Naval Group

- Arquus

- Dassault Aviation

- MBDA

- CMA CGM Group

- GEODIS

- Daher

- Sabena technics

- KNDS

- SPIE

- Kuehne+Nagel

- DHL Supply Chain

- DSV (Incl. DB Schenker)

- Turgis Gaillard

- MROD

- Alstef Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview & Role of Logistics in Modern Warfare

- 4.2 Defense Spending Trends

- 4.3 Market Drivers

- 4.3.1 Modernization of Strategic Air- and Sea-Lift Fleets

- 4.3.2 Outsourcing of SIMMAD and MCO Service Contracts

- 4.3.3 NATO Readiness Stockpile Mandates

- 4.3.4 Predictive-Maintenance Rollout (Plan SICS-SC2)

- 4.3.5 Climate-Resilient Logistics Infrastructure Upgrades

- 4.3.6 Dual-Use Hubs for Space and Drone Operations Near Toulouse

- 4.4 Market Restraints

- 4.4.1 Budgetary Pressure from Social-Spending Trade-Offs

- 4.4.2 Global Raw-Material and Component Shortages

- 4.4.3 EU Carbon-Emission Caps on Military Transport

- 4.4.4 Ageing Workforce in Logistics Corps

- 4.5 Regulatory Framework

- 4.6 Value Chain and Distribution Channel Architecture Analysis

- 4.7 Technology Innovations Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Rivalry Among Competitors

- 4.9 Evolution of Defense Logistics Requirements

- 4.10 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Service Type

- 5.1.1 Armament

- 5.1.2 Military Troops Movement Support

- 5.1.3 Technical Support & Maintenance

- 5.1.4 Medical Aid & Health Services

- 5.1.5 Fire-fighting Protection

- 5.1.6 Other Services

- 5.2 By Logistics Function

- 5.2.1 Transportation

- 5.2.1.1 Road

- 5.2.1.2 Air

- 5.2.1.3 Sea and Inland Waterways

- 5.2.1.4 Rail

- 5.2.2 Warehousing & Distribution

- 5.2.3 Value-added Services (Labelling, Kitting, Consulting)

- 5.2.1 Transportation

- 5.3 By End User

- 5.3.1 Army

- 5.3.2 Navy

- 5.3.3 Air Force

- 5.3.4 Others

- 5.4 By Region

- 5.4.1 Ile-de-France

- 5.4.2 Auvergne-Rhone-Alpes

- 5.4.3 Provence-Alpes-Cote d'Azur

- 5.4.4 Hauts-de-France

- 5.4.5 Nouvelle-Aquitaine

- 5.4.6 Occitanie

- 5.4.7 Grand Est

- 5.4.8 Brittany

- 5.4.9 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Airbus Defence and Space

- 6.4.2 Thales Group

- 6.4.3 Safran

- 6.4.4 Naval Group

- 6.4.5 Arquus

- 6.4.6 Dassault Aviation

- 6.4.7 MBDA

- 6.4.8 CMA CGM Group

- 6.4.9 GEODIS

- 6.4.10 Daher

- 6.4.11 Sabena technics

- 6.4.12 KNDS

- 6.4.13 SPIE

- 6.4.14 Kuehne+Nagel

- 6.4.15 DHL Supply Chain

- 6.4.16 DSV (Incl. DB Schenker)

- 6.4.17 Turgis Gaillard

- 6.4.18 MROD

- 6.4.19 Alstef Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment