PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072981

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072981

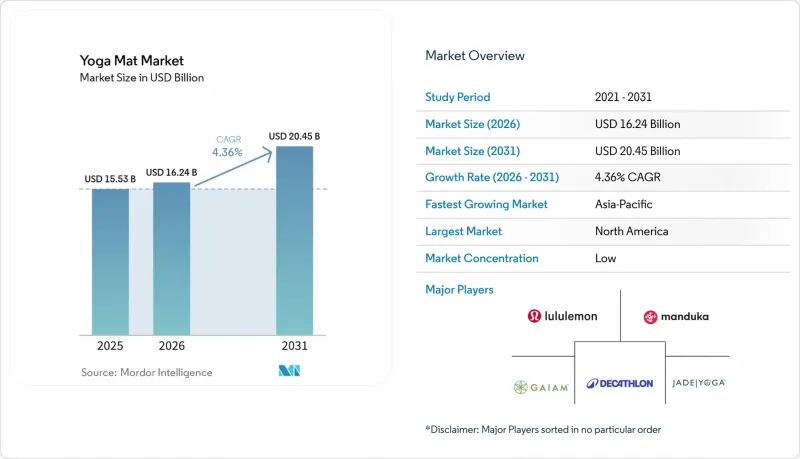

Yoga Mat - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the yoga mat market size was valued at USD 15.53 billion in 2025 and is estimated to grow from USD 16.24 billion in 2026 to reach USD 20.45 billion by 2031, at a CAGR of 4.36% during the forecast period 2026 to 2031.

This report is Segmented by Material Type (Rubber, Cotton, PVC, TPE, Others), Category (Conventional, Organic/Natural), Price Tier (Mass, Premium), End Use (Individual, Commercial), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Yoga Mat Market Trends and Insights

Rising Global Yoga And Wellness Participation

The continued expansion of yoga participation beyond traditionally mature markets is strengthening the long-term demand foundation of the yoga mat market. With more than 300 million yoga practitioners worldwide in 2025 and approximately 38.4 million practitioners in the United States, the market benefits from a substantial and growing installed user base that supports both new product adoption and recurring replacement demand . This expanding consumer pool contributes not only to first-time purchases but also to higher replacement rates as users upgrade from entry-level mats, replace worn products, and adopt specialized mats tailored to different practice styles and fitness routines. These dynamics create a balanced demand structure across multiple price segments and help sustain market resilience during periods of economic uncertainty. As yoga remains a relatively accessible and low-cost wellness activity, the requirement for a dedicated mat as a core piece of equipment continues to provide a stable and recurring source of demand for manufacturers and retailers.

Increasing Demand For Eco-Friendly Yoga Products

Sustainability has evolved from a niche consideration into a key purchasing criterion, significantly influencing product development, sourcing strategies, and brand positioning across the yoga mat market. Consumers are increasingly evaluating products based on material provenance, chemical safety standards, renewable content, and third-party certifications, particularly within premium segments where transparency and brand credibility play an important role in purchase decisions. The launch of innovative products such as the Mushroom Mat by JadeYoga in 2025 highlights how manufacturers are integrating sustainability directly into product differentiation strategies rather than treating it solely as a marketing claim. This trend is accelerating demand for eco-friendly materials including natural rubber, jute, cork, and other renewable alternatives, while simultaneously increasing scrutiny of conventional materials with respect to safety, environmental impact, and product longevity. As a result, sustainability is becoming a competitive factor across the value chain, influencing both consumer preference and brand positioning. The growing emphasis on environmentally responsible materials, cleaner manufacturing processes, and certification compliance is also supporting premiumization within the market, enabling higher average selling prices and strengthening value growth in eco-conscious product categories.

Intense Price Competition From Low-Cost Manufacturers

The yoga mat market continues to face significant pricing pressure due to intense competition within the entry-level and mass-market segments, where products are often differentiated primarily by price and distribution reach. The abundance of low-cost alternatives creates a highly competitive environment that can limit pricing power across the category and intensify margin pressures for manufacturers. Chinese manufacturers benefit from integrated supply chains, efficient export infrastructure, and large-scale production capabilities, enabling cost-efficient manufacturing and strong price competitiveness in global markets . This challenge is particularly pronounced for mid-tier brands, which often struggle to compete effectively against budget-focused suppliers while lacking the brand equity, performance differentiation, or sustainability credentials required to command premium pricing. As basic yoga mats are increasingly perceived as commoditized products, competitive dynamics shift toward price-based purchasing decisions, reducing profitability and limiting the resources available for product innovation, marketing, and brand development. In response, many manufacturers are expanding direct-to-consumer (DTC) sales channels to improve margin retention and strengthen customer relationships. However, while DTC strategies can enhance gross margins, they also increase exposure to customer acquisition costs, digital marketing expenses, and customer retention challenges. As a result, profitability becomes increasingly dependent on repeat purchases, brand loyalty, and lifetime customer value.

Other drivers and restraints analyzed in the detailed report include:

- Product Innovation In Materials And Performance

- Growing Corporate Wellness And Mindfulness Fitness

- Availability of Substitute Fitness Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PVC accounted for 38.9% of total segment revenue in 2025, maintaining its position as the leading material category due to its durability, cost efficiency, and widespread availability across mass retail and e-commerce channels. However, rubber-based mats are projected to record the fastest growth rate, with a CAGR of 4.8% through 2031, reflecting increasing consumer preference for premium products that offer superior grip, cushioning, durability, and environmental credentials.

The growing adoption of rubber materials underscores a broader premiumization trend across the yoga mat market, where purchasing decisions are increasingly influenced by performance characteristics and sustainability considerations rather than price alone. Meanwhile, thermoplastic elastomer (TPE) continues to occupy a strategic middle-market position by providing a lightweight, perceived eco-friendlier alternative to conventional PVC while remaining more cost-effective than natural rubber-based products. Material selection has become an increasingly important competitive differentiator, extending beyond product feel and weight to influence brand perception, certification eligibility, retailer acceptance, regulatory compliance, and end-user positioning.

Conventional yoga mats accounted for 58.5% of total market share in 2025, maintaining a dominant position due to their affordability, broad retail availability, and suitability for a wide range of end users, including first-time practitioners, fitness centers, and yoga studios. Their accessibility and cost-effectiveness continue to support strong demand across both consumer and commercial channels.

In contrast, the organic and natural yoga mat segment is projected to expand at a CAGR of 6.8% through 2031, making it one of the fastest-growing categories within the broader market. Growth in this segment is being driven by increasing consumer awareness of material safety, environmental sustainability, responsible sourcing practices, and overall product transparency. As wellness-oriented consumers become more selective about the products they use, demand is shifting toward mats that offer both functional performance and stronger sustainability credentials. The category is also benefiting from ongoing product innovation that enhances the appeal of natural materials without compromising performance standards. New product developments have demonstrated that sustainability-focused materials can deliver competitive levels of grip, durability, and comfort while supporting environmentally responsible brand positioning.

Complete Report Scope:

- By Material Type

- Rubber

- Cotton

- Polyvinyl Chloride (PVC)

- Thermoplastic Elastomer (TPE)

- Others (Ethylene Vinyl Acetate/ Cork/Jute)

- By Category

- Conventional

- Organic/Natural

- By Price Tier

- Mass

- Premium

- By End Use

- Individual

- Commercial

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Netherlands

- Italy

- Sweden

- Norway

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Vietnam

- Indonesia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- South Africa

- Saudi Arabia

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Geography Analysis

North America accounted for 34.9% of global market revenue in 2025, maintaining its position as the largest regional market. The region benefits from high consumer spending on health and wellness, a well-established specialty retail ecosystem, strong e-commerce penetration, and a large base of active yoga practitioners. These factors support robust demand for both replacement purchases and premium product upgrades. The United States remains the primary growth engine within the region, driven by strong consumer preference for branded, performance-oriented, and certified products, while Canada and Mexico contribute additional demand across both consumer and institutional channels.

Europe represents one of the highest-value regional markets, characterized by strong consumer emphasis on product quality, material transparency, sustainability, and regulatory compliance. Markets such as Germany, the United Kingdom, France, the Netherlands, Italy, Spain, and the Nordic countries demonstrate heightened demand for products with verified environmental and safety credentials. This environment creates favorable conditions for materials such as natural rubber, TPE, cork, and other sustainable alternatives that align with increasingly stringent consumer and retailer expectations. As a result, Europe continues to support premium pricing strategies and offers stronger competitive positioning for brands that can demonstrate product differentiation through quality, certification, and responsible sourcing practices.

Asia-Pacific is projected to be the fastest-growing regional market, with a CAGR of 8.1% through 2031. Growth is being driven by increasing urbanization, rising health and wellness awareness, expanding middle-class populations, improving retail accessibility, and supportive initiatives promoting physical activity across several major economies. The region also benefits from a well-developed manufacturing ecosystem that supports both domestic consumption and global supply chains. China remains a critical market due to its combination of large-scale production capabilities and expanding wellness consumer base, while India serves as both a high-growth consumption market and an important source of natural rubber and fiber-based raw materials. Meanwhile, Japan and South Korea continue to drive demand for premium, performance-focused products, and Southeast Asian markets are gaining importance as both consumer markets and manufacturing hubs.

Although South America and the Middle East & Africa currently represent a smaller share of global demand, both regions offer attractive long-term growth opportunities. Countries including Brazil, Argentina, the United Arab Emirates, Saudi Arabia, and South Africa are experiencing increasing wellness adoption, expanding fitness infrastructure, and growing hospitality investments. These trends are supporting the development of niche premium segments and creating opportunities for market participants seeking expansion beyond established regional markets.

- Ecoyoga Ltd.

- Manduka Europe

- JadeYoga

- Lululemon Athletica

- Alo, LLC

- Hugger Mugger

- Prosource Fit

- Yaazh Naturals Private Limited

- Aurorae LLC

- PrAna

- Liforme Ltd.

- Barefoot Yoga Co.

- TriMax Sports Inc.

- Body-Solid, Inc.

- Gaiam

- Yoga Direct

- Suga

- Khataland

- Decathlon Sports

- Nike, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global yoga and wellness participation

- 4.2.2 Expanding home fitness and exercise trends

- 4.2.3 Increasing demand for eco-friendly yoga products

- 4.2.4 Product innovation in materials and performance

- 4.2.5 Growing corporate wellness and mindfulness programs

- 4.2.6 Strong influence of social media fitness

- 4.3 Market Restraints

- 4.3.1 Intense price competition from low-cost manufacturers

- 4.3.2 Limited product differentiation across mainstream brands

- 4.3.3 Fluctuating demand from seasonal fitness trends

- 4.3.4 Availability of substitute fitness equipment products

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers/Consumers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Rubber

- 5.1.2 Cotton

- 5.1.3 Polyvinyl Chloride (PVC)

- 5.1.4 Thermoplastic Elastomer (TPE)

- 5.1.5 Others (Ethylene Vinyl Acetate/ Cork/Jute)

- 5.2 By Category

- 5.2.1 Conventional

- 5.2.2 Organic/Natural

- 5.3 By Price Tier

- 5.3.1 Mass

- 5.3.2 Premium

- 5.4 By End Use

- 5.4.1 Individual

- 5.4.2 Commercial

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Italy

- 5.5.2.6 Netherlands

- 5.5.2.7 Italy

- 5.5.2.8 Sweden

- 5.5.2.9 Norway

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Vietnam

- 5.5.3.7 Indonesia

- 5.5.3.8 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ecoyoga Ltd.

- 6.4.2 Manduka Europe

- 6.4.3 JadeYoga

- 6.4.4 Lululemon Athletica

- 6.4.5 Alo, LLC

- 6.4.6 Hugger Mugger

- 6.4.7 Prosource Fit

- 6.4.8 Yaazh Naturals Private Limited

- 6.4.9 Aurorae LLC

- 6.4.10 PrAna

- 6.4.11 Liforme Ltd.

- 6.4.12 Barefoot Yoga Co.

- 6.4.13 TriMax Sports Inc.

- 6.4.14 Body-Solid, Inc.

- 6.4.15 Gaiam

- 6.4.16 Yoga Direct

- 6.4.17 Suga

- 6.4.18 Khataland

- 6.4.19 Decathlon Sports

- 6.4.20 Nike, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK