PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073040

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073040

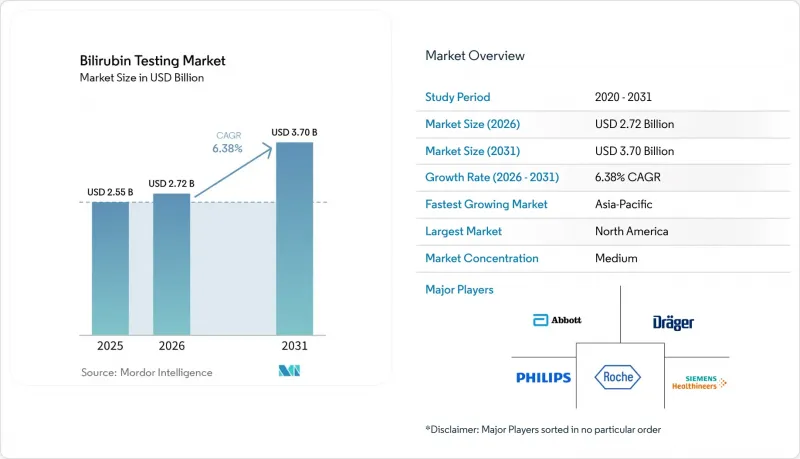

Bilirubin Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the bilirubin testing market size is expected to increase from USD 2.55 billion in 2025 to USD 2.72 billion in 2026 and reach USD 3.70 billion by 2031, growing at a CAGR of 6.38% over 2026-2031.

This report is Segmented by Test Type (Total Bilirubin Tests, and More), Product Type (Reagents, Calibrators, Cartridges, Analyzers), Technology (Lab-Based, Point-Of-Care, Transcutaneous), Application (Neonatal, Liver Function, Hemolytic, Pre-Op), End User (Hospitals, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Bilirubin Testing Market Trends and Insights

Rising Neonatal Jaundice Screening Requirements

Neonatal jaundice, a prevalent condition in newborn care, underscores the importance of bilirubin monitoring, bolstering the market for bilirubin testing. Public health systems are expanding formal screening coverage, transitioning bilirubin testing from an optional procedure to a standard protocol in maternity settings. In January 2026, NSW Health revised its neonatal jaundice management guidelines, introducing universal transcutaneous screening for babies as young as 32 weeks gestation, thereby broadening the screened population in an established care system. Similarly, in 2025, China mandated transcutaneous bilirubin monitoring within 48 hours of birth at grassroots institutions, integrating national guidance into the daily operations of lower-tier facilities. In India, the Mission ANMOL initiative incorporates bilirubin testing into a comprehensive newborn screening framework, bolstering demand in public facilities catering to large infant populations.

Shift Toward Non-Invasive Transcutaneous Bilirubin Monitoring

Due to the desire for quicker screenings with minimal discomfort, the bilirubin testing market is increasingly favoring non-invasive transcutaneous measurements. This shift is particularly significant in high-volume nurseries and intensive care units, where the speed of workflow can influence discharge and treatment decisions. A 2026 study highlighted the Picterus Jaundice Pro smartphone application, which demonstrated a strong correlation with transcutaneous reference measurements across 215 paired readings, underscoring the growing clinical utility of cost-effective optical tools.

While serum confirmation remains essential near treatment thresholds, the market is benefiting from the transcutaneous approach, as it diminishes the need for invasive tests prior to escalation.

Mandatory Serum Confirmation Near Treatment Threshold

The bilirubin testing market faces limitations as non-invasive methods cannot fully replace serum testing near treatment thresholds. Clinical protocols require total serum bilirubin confirmation in such cases, meaning transcutaneous devices reduce but do not eliminate invasive sampling. Neonatal bilirubin testing remains complex due to interlaboratory variations and differences in bilirubin fractions, which impact safe decision-making. This sustains demand for reagents, calibrators, and laboratory assays, even as transcutaneous screening expands. Hospitals must maintain dual workflows for screening and confirmation, slowing full substitution for device manufacturers.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Point-of-Care Bilirubin Testing in NICUs and Community Settings

- Updated Hyperbilirubinemia Screening Guidelines Mandating Universal Testing

- Cost And Service Burden Of Analyzer Calibration And Uptime Maintenance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Total Bilirubin Tests held 61.68% of the bilirubin testing market share, highlighting their critical role in routine diagnostics. This test is essential for managing newborn jaundice and assessing liver function in adults, ensuring its widespread use across various age groups and healthcare settings. The market's reliance on total bilirubin remains strong due to its integration into major care pathways and its role as the primary marker in standardized protocols, making the segment resilient even with the emergence of new technologies.

Direct Bilirubin Tests are projected to grow at a 6.90% CAGR through 2031, driven by increased focus on conjugated hyperbilirubinemia in neonates and comprehensive hepatobiliary assessments in adults. Clinical Pathology Laboratories updated reporting and reference ranges for direct bilirubin in February 2025, reflecting a more refined clinical approach. Indirect bilirubin testing remains significant for hemolytic disease and G6PD-related assessments, particularly in populations with hereditary risks. The market is expected to see more fractionated panels integrated into workflows, increasing testing volumes per specimen despite pricing pressures.

Reagents and Assay Consumables accounted for 58.23% of the bilirubin testing market in 2025, reflecting the recurring nature of chemistry-based testing. This segment benefits from repeat bilirubin orders processed on automated analyzers, providing a stable revenue base. Laboratories often remain within validated reagent ecosystems, ensuring repeat purchases and reducing vendor switching. This dynamic secures the position of reagent suppliers even during slower equipment procurement periods.

Calibrators and Quality Controls are expected to grow at a 7.25% CAGR through 2031, supported by the expansion of bilirubin testing into decentralized care points. As bedside and near-patient testing increases, new locations drive demand for verification materials. Test cartridges and strips remain vital in point-of-care settings, enabling single-use testing without the maintenance demands of central analyzers, creating a balanced product structure within the market.

Complete Report Scope:

- By Test Type

- Total Bilirubin Tests

- Direct Bilirubin Tests

- Indirect Bilirubin Tests

- By Product Type

- Reagents and Assay Consumables

- Calibrators and Quality Controls

- Test Cartridges and Strips

- Dedicated Blood Bilirubin Analyzers

- By Technology

- Laboratory-Based Testing

- Point-of-Care Blood Testing

- Transcutaneous Screening Systems

- By Application

- Neonatal Jaundice Screening and Monitoring

- Liver Function Assessment

- Hemolytic Disorder Assessment

- Pre-Operative and Routine Health Screening

- By End User

- Hospitals and NICUs

- Diagnostic Laboratories

- Maternity and Neonatal Clinics

- Outpatient and Ambulatory Care Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America dominated the bilirubin testing market, holding a 39.55% share. This leadership is driven by structured newborn screening programs, widespread access to automated chemistry platforms, and hospitals' adoption of defined bilirubin care pathways. The U.S. remains the largest market in the region due to the integration of universal newborn bilirubin assessments into pediatric care guidelines and continuous updates to testing platforms by major suppliers. In 2026, Roche and Siemens achieved significant U.S. regulatory milestones for bilirubin-related chemistry capabilities, strengthening the installed base and product updates. Canada supports the market with aligned pediatric screening practices, while Mexico contributes through hospital-based diagnostic demand linked to maternal and newborn care.

Asia-Pacific is projected to grow at a 6.76% CAGR through 2031, making it the fastest-growing region in the bilirubin testing market. China's 2025 neonatal guidelines formalized transcutaneous bilirubin monitoring, driving procurement across lower-tier care sites. India is advancing through public healthcare programs that expand affordable diagnostic access and local validation efforts supporting point-of-care bilirubin use in neonatal wards. Countries like Japan, South Korea, and Australia, with mature NICU infrastructures, continue to grow, with Australia demonstrating in 2026 that broader screening protocols can unlock additional volumes.

Europe maintains a strong position in the bilirubin testing market due to structured neonatal care pathways, stable public reimbursements, and high laboratory quality standards. The region's combined use of transcutaneous and laboratory methods sustains demand for both devices and consumables. In the Middle East and Africa, clinical needs are significant, particularly in areas with high incidences of neonatal jaundice and inherited hemolytic conditions, though infrastructure and service capacity remain challenges. South America shows steady growth, supported by public maternity screenings and general diagnostic demand, despite variations in access and purchasing power across countries.

- Abbott Laboratories

- Beckton Dickinson

- bioMerieux

- Danaher

- DiaSys Diagnostic Systems

- Dragerwerk AG and Co. KGaA

- Elitech Group

- Roche

- HORIBA

- Konica Minolta

- Koninklijke Philips

- Mennen Medical Ltd.

- Mindray Bio-Medical Electronics Co., Ltd.

- Natus Medical

- Nova Biomedical

- QuidelOrtho

- Radiometer Medical ApS

- Randox Laboratories

- Sekisui Diagnostics

- Siemens Healthineers

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Drivers

- 4.1.1 Rising Neonatal Jaundice Screening Requirements

- 4.1.2 Shift Toward Non-Invasive Transcutaneous Bilirubinometry

- 4.1.3 Expansion of Point-of-Care Bilirubin Testing in NICUs and Maternity Units

- 4.1.4 Updated Hyperbilirubinemia Screening Guidelines and Earlier Discharge Monitoring

- 4.1.5 EMR-Integrated Bilirubin Workflows for Closed-Loop Newborn Follow-Up

- 4.1.6 Higher Validation Demand for Skin Tone and Phototherapy Interference

- 4.2 Market Restraints

- 4.2.1 Mandatory Serum Confirmation Near Treatment Thresholds

- 4.2.2 Cost and Service Burden of Analyzer Calibration, Uptime, and Consumables

- 4.2.3 Measurement Variability Under Phototherapy and in Highly Pigmented Skin

- 4.2.4 Limited Utilization Outside High-Birth-Volume Care Settings

- 4.3 Value and Supply-Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VAALUE, USD)

- 5.1 By Test Type

- 5.1.1 Total Bilirubin Tests

- 5.1.2 Direct Bilirubin Tests

- 5.1.3 Indirect Bilirubin Tests

- 5.2 By Product Type

- 5.2.1 Reagents and Assay Consumables

- 5.2.2 Calibrators and Quality Controls

- 5.2.3 Test Cartridges and Strips

- 5.2.4 Dedicated Blood Bilirubin Analyzers

- 5.3 By Technology

- 5.3.1 Laboratory-Based Testing

- 5.3.2 Point-of-Care Blood Testing

- 5.3.3 Transcutaneous Screening Systems

- 5.4 By Application

- 5.4.1 Neonatal Jaundice Screening and Monitoring

- 5.4.2 Liver Function Assessment

- 5.4.3 Hemolytic Disorder Assessment

- 5.4.4 Pre-Operative and Routine Health Screening

- 5.5 By End User

- 5.5.1 Hospitals and NICUs

- 5.5.2 Diagnostic Laboratories

- 5.5.3 Maternity and Neonatal Clinics

- 5.5.4 Outpatient and Ambulatory Care Centers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Beckman Coulter, Inc.

- 6.3.3 bioMerieux SA

- 6.3.4 Danaher Corporation

- 6.3.5 DiaSys Diagnostic Systems GmbH

- 6.3.6 Dragerwerk AG and Co. KGaA

- 6.3.7 ELITechGroup

- 6.3.8 F. Hoffmann-La Roche Ltd

- 6.3.9 HORIBA, Ltd.

- 6.3.10 Konica Minolta, Inc.

- 6.3.11 Koninklijke Philips N.V.

- 6.3.12 Mennen Medical Ltd.

- 6.3.13 Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.14 Natus Medical Incorporated

- 6.3.15 Nova Biomedical Corporation

- 6.3.16 QuidelOrtho Corporation

- 6.3.17 Radiometer Medical ApS

- 6.3.18 Randox Laboratories Ltd.

- 6.3.19 Sekisui Diagnostics, LLC

- 6.3.20 Siemens Healthineers AG

- 6.3.21 Thermo Fisher Scientific Inc.

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment