PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073043

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073043

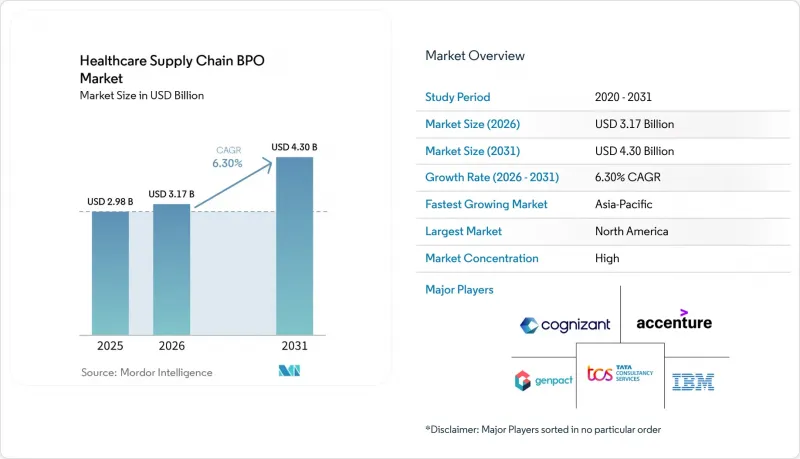

Healthcare Supply Chain BPO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the healthcare supply chain BPO market size was valued at USD 2.98 billion in 2025 and is estimated to grow from USD 3.17 billion in 2026 to reach USD 4.30 billion by 2031, at a CAGR of 6.30% during the forecast period (2026-2031).

This report is Segmented by Type, Product (Inventory Management, Procurement, Logistics, Supplier Management, Order Management), Services, Technology (Cloud-Based, AI, Blockchain, RPA, IoT), Component, Application (Hospitals, Pharma, Medical Devices), Process, Deployment, End User, and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts in Value (USD).

Global Healthcare Supply Chain BPO Market Trends and Insights

Expanding Clinical Pipelines For RNA-Targeted Medicines

As of mid-2026, over 200 organizations contributed to the global oligonucleotide clinical pipeline, providing the oligonucleotide CDMO market with a diverse and active customer base, reducing reliance on a select few sponsors. Every IND-stage and late-stage program requires GMP material prior to approval and commercialization. The pipeline is increasingly leaning towards larger cardiometabolic opportunities, altering expected batch sizes and intensifying the pressure on commercial supply planning, a shift from the previous focus on rare diseases. Legacy synthesis footprints weren't designed to handle demands scaling from kilograms to tonnes across an expanding array of chronic indications.

Outsourcing Shift For Complex Oligonucleotide Synthesis And Fill-Finish

The oligonucleotide CDMO market is witnessing a pronounced outsourcing trend, as many innovators find it challenging to manage complex oligonucleotide synthesis to commercial standards internally. Manufacturing GalNAc-conjugated siRNA demands meticulous coordination across assembly, deprotection, conjugation, purification, and impurity profiling, with each step introducing distinct technical challenges under ICH standards. By the first half of 2025, WuXi AppTec's TIDES platform was servicing 69 molecules for both API and drug product services, a figure that has more than doubled in just two years. The fill-finish phase is gaining prominence as products transition to subcutaneous and prefilled formats, necessitating sterile capacities beyond mere API synthesis.

High Process Complexity And Yield Sensitivity In Long-Chain Oligonucleotides

The oligonucleotide CDMO market faces a significant technical challenge due to the stepwise synthesis process, where one nucleotide is added at a time. This method results in compounded efficiency losses for longer sequences. For example, a 20-mer ASO undergoes at least 20 coupling cycles, and even with high per-step efficiency, the final yield can drop noticeably. The challenge becomes more pronounced with modifications like phosphorothioate backbones, 2'-fluoro substitutions, or GalNAc ligands, which introduce additional side reactions and analytical complexities. Providers transitioning from peptides or small molecules often underestimate timelines, impurity management, and batch failure risks, leading to slower capacity ramp-up despite strong demand. Consequently, commercial supply remains concentrated among experienced companies with extensive operational histories.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand For Precision Medicine And Rare-Disease Programs

- Scale-Up Pressure From Dual-Route Manufacturing, Clinical And GMP

- Stringent Purity, Impurity, And Potency Control Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Transactional BPO accounted for 41.68% of the segment, making it the largest contract model by current value. Comprehensive BPO is projected to grow at an 8.90% CAGR through 2031, emerging as the fastest-growing type in the healthcare supply chain BPO market. Many hospitals, regional providers, and distributors start outsourcing with limited scopes like order processing and invoice support, concentrating volume in standardized workflows.

Comprehensive BPO is expanding as buyers seek single partners to manage procurement, logistics, inventory, and analytics. This model gains traction as healthcare organizations grow confident in setting service outcomes and holding vendors accountable. Process-Specific BPO remains a middle-ground option for targeted outsourcing without a full operational shift. Over time, the market is expected to see more contracts adopting end-to-end structures for tighter control across supply chain functions.

Order Management held 36.23% of the product segment in 2025, making it the largest by value. Procurement Services is projected to grow at a 9.25% CAGR through 2031, becoming the fastest-growing product area. Hospitals and healthcare networks rely on Order Management for processing large order volumes across thousands of SKUs, as these workflows are repetitive and easier to standardize.

Procurement Services are growing as clients demand support in sourcing, supplier risk assessment, contract compliance, and spend analysis. This shift moves demand toward higher-value operational support. Logistics and Supplier Management are also benefiting as organizations diversify suppliers and enhance network resilience, driving a gradual shift from transaction-heavy to strategic functions.

Consulting Services held 36.74% of the segment in 2025, making it the largest services category by revenue. Implementation Services is projected to grow at an 8.55% CAGR through 2031, becoming the fastest-growing service type. Consulting remains strong as most outsourcing programs begin with assessment, design, process mapping, and operating model planning.

Implementation is growing as more organizations move from planning to execution, requiring setup, integration, testing, and change management. Support and Maintenance Services are also gaining importance as buyers prefer continuity post-deployment. This full life cycle approach is evident in partnerships like TraceLink and Genpact, combining digital supply chain technology with managed services.

Complete Report Scope:

- By Type

- Transactional BPO

- Process-Specific BPO

- Comprehensive BPO

- By Product

- Inventory Management

- Procurement Services

- Logistics Management

- Supplier Management

- Order Management

- By Services

- Consulting Services

- Implementation Services

- Support and Maintenance Services

- By Technology

- Cloud-Based Solutions

- Artificial Intelligence

- Blockchain

- Robotic Process Automation

- Internet of Things

- By Component

- Software

- Hardware

- Services

- By Application

- Hospitals and Clinics

- Pharmaceutical Companies

- Medical Device Manufacturers

- By Process

- Order Fulfillment

- Demand Planning

- Supplier Relationship Management

- By Deployment

- On-Premise

- Cloud-Based

- Hybrid

- By End User

- Healthcare Providers

- Pharmaceutical Companies

- Medical Device Manufacturers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

In 2025, North America held a 39.55% share of the oligonucleotide CDMO market, driven by a strong presence of RNA-targeted drug developers and mature GMP sites in the U.S. and Canada. Companies like Alnylam, Ionis, Arrowhead, and Wave Life Sciences, along with manufacturing leaders such as Agilent and Thermo Fisher Scientific, anchor the region's market. Agilent's 2026 launch of Agilent Advanced Therapeutics integrated BIOVECTRA in Canada and Nucleic Acid Solutions in Colorado, enhancing North America's CDMO capabilities. Familiarity with FDA regulations and established GMP track records further strengthen the region's position, though its lead may narrow as global capacity expands and delivery time advantages diminish.

Europe remains a key technical hub in the oligonucleotide CDMO market, led by Germany and Switzerland, with a focus on high-purity API manufacturing and sustained capital investments. BioSpring is investing over EUR 100 million (USD 108 million) in a new nucleic acid API facility in Offenbach, set for completion by late 2027. Bachem allocated CHF 332.6 million in 2025 to expand its network, initiated commercial production in 2026, and plans an additional CHF 400 million in CapEx for 2026. Lonza projects 11-12% sales growth for 2026 and continues to enhance its synthesis and antibody-oligonucleotide conjugate capabilities in the Netherlands. Europe's strength lies in its technical expertise, regulatory rigor, and ability to meet stringent quality demands.

Asia-Pacific is the fastest-growing region in the oligonucleotide CDMO market, with a 24.56% CAGR through 2031, driven by capacity expansions in China, South Korea, and Japan. Asymchem's TJ4 facility in Tianjin offers 180 mol per year of oligonucleotide capacity, supported by advanced processing tools and an integrated drug product facility. WuXi AppTec's API sites in Changzhou and Taixing passed FDA inspections in 2025, ensuring continued U.S. supply. Japan's Nippon Shokubai is expanding its GMP-compliant nucleic acid API capacity tenfold. South America and the Middle East & Africa remain emerging markets, primarily relying on imports from North America, Europe, and Asia-Pacific hubs.

- Accenture

- Capgemini

- Cardinal Health

- Cognizant

- Conduent Incorporated

- Coupa Software Incorporated

- EXLService Holdings, Inc.

- Firstsource Solutions Limited

- GeBBS Healthcare Solutions, Inc.

- Genpact

- Global Healthcare Exchange, LLC

- HCL Technologies Limited

- IBM

- Infosys

- JAGGAER, LLC

- Mckesson

- NTT DATA Group Corporation

- Premier, Inc.

- Sutherland Global Services, Inc.

- Tata Consultancy Services

- Tech Mahindra Limited

- Vizient

- Wipro

- WNS (Holdings) Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Outsourcing Pressure From Healthcare Procurement Complexity

- 4.2.2 Demand for Inventory Visibility Across Multi-Tier Supplier Networks

- 4.2.3 Shift Toward Cloud-Enabled Process Orchestration and Analytics

- 4.2.4 Regulatory Traceability Requirements for Pharmaceuticals and Medical Devices

- 4.2.5 Provider Need to Reduce Working Capital Locked in Supply Chains

- 4.2.6 Cross-Border Supply Chain Resilience and Nearshoring Programs

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Contractual Risk Concerns in Outsourced Operations

- 4.3.2 Integration Friction With Legacy ERP, EDI, and Warehouse Systems

- 4.3.3 Limited Process Standardization Across Provider and Supplier Networks

- 4.3.4 Talent Dependence for Domain-Specific Healthcare Supply Chain Workflows

- 4.4 Value and Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Type

- 5.1.1 Transactional BPO

- 5.1.2 Process-Specific BPO

- 5.1.3 Comprehensive BPO

- 5.2 By Product

- 5.2.1 Inventory Management

- 5.2.2 Procurement Services

- 5.2.3 Logistics Management

- 5.2.4 Supplier Management

- 5.2.5 Order Management

- 5.3 By Services

- 5.3.1 Consulting Services

- 5.3.2 Implementation Services

- 5.3.3 Support and Maintenance Services

- 5.4 By Technology

- 5.4.1 Cloud-Based Solutions

- 5.4.2 Artificial Intelligence

- 5.4.3 Blockchain

- 5.4.4 Robotic Process Automation

- 5.4.5 Internet of Things

- 5.5 By Component

- 5.5.1 Software

- 5.5.2 Hardware

- 5.5.3 Services

- 5.6 By Application

- 5.6.1 Hospitals and Clinics

- 5.6.2 Pharmaceutical Companies

- 5.6.3 Medical Device Manufacturers

- 5.7 By Process

- 5.7.1 Order Fulfillment

- 5.7.2 Demand Planning

- 5.7.3 Supplier Relationship Management

- 5.8 By Deployment

- 5.8.1 On-Premise

- 5.8.2 Cloud-Based

- 5.8.3 Hybrid

- 5.9 By End User

- 5.9.1 Healthcare Providers

- 5.9.2 Pharmaceutical Companies

- 5.9.3 Medical Device Manufacturers

- 5.10 By Geography

- 5.10.1 North America

- 5.10.1.1 United States

- 5.10.1.2 Canada

- 5.10.1.3 Mexico

- 5.10.2 Europe

- 5.10.2.1 Germany

- 5.10.2.2 United Kingdom

- 5.10.2.3 France

- 5.10.2.4 Italy

- 5.10.2.5 Spain

- 5.10.2.6 Rest of Europe

- 5.10.3 Asia-Pacific

- 5.10.3.1 China

- 5.10.3.2 India

- 5.10.3.3 Japan

- 5.10.3.4 Australia

- 5.10.3.5 South Korea

- 5.10.3.6 Rest of Asia-Pacific

- 5.10.4 Middle East and Africa

- 5.10.4.1 GCC

- 5.10.4.2 South Africa

- 5.10.4.3 Rest of Middle East and Africa

- 5.10.5 South America

- 5.10.5.1 Brazil

- 5.10.5.2 Argentina

- 5.10.5.3 Rest of South America

- 5.10.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Accenture plc

- 6.3.2 Capgemini SE

- 6.3.3 Cardinal Health, Inc.

- 6.3.4 Cognizant Technology Solutions Corporation

- 6.3.5 Conduent Incorporated

- 6.3.6 Coupa Software Incorporated

- 6.3.7 EXLService Holdings, Inc.

- 6.3.8 Firstsource Solutions Limited

- 6.3.9 GeBBS Healthcare Solutions, Inc.

- 6.3.10 Genpact Limited

- 6.3.11 Global Healthcare Exchange, LLC

- 6.3.12 HCL Technologies Limited

- 6.3.13 IBM Corporation

- 6.3.14 Infosys Limited

- 6.3.15 JAGGAER, LLC

- 6.3.16 McKesson Corporation

- 6.3.17 NTT DATA Group Corporation

- 6.3.18 Premier, Inc.

- 6.3.19 Sutherland Global Services, Inc.

- 6.3.20 Tata Consultancy Services Limited

- 6.3.21 Tech Mahindra Limited

- 6.3.22 Vizient, Inc.

- 6.3.23 Wipro Limited

- 6.3.24 WNS (Holdings) Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment