PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073110

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073110

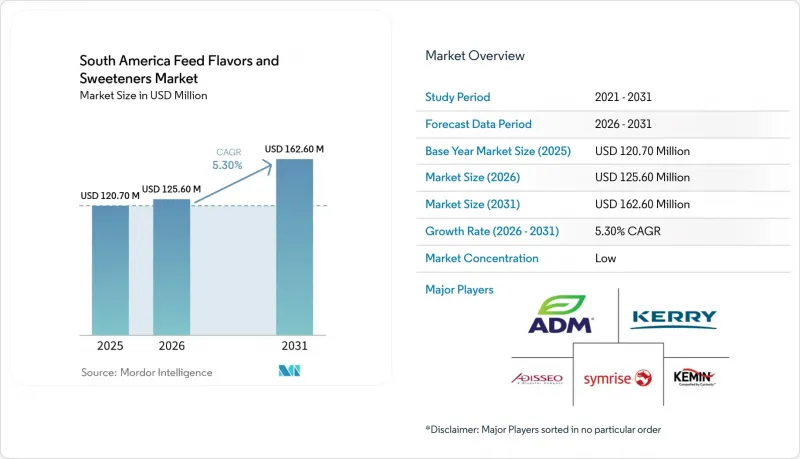

South America Feed Flavors and Sweeteners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the south america feed flavors and sweeteners market size was valued at USD 120.70 million in 2025 and estimated to grow from USD 125.60 million in 2026 to reach USD 162.60 million by 2031, at a CAGR of 5.30% during the forecast period (2026-2031).

This report is Segmented by Sub Type (Flavors and Sweeteners), by Animal Type (Ruminants, Swine, and Other Animal Type), and by Geography (Brazil, Chile, Argentina, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

South America Feed Flavors and Sweeteners Market Trends and Insights

Export-Led Pork Production Growth

Brazil's role as one of the world's largest meat exporter and a leading pork exporter creates a strong volume base for the South America feed flavors and sweeteners market. According to the Brazilian Association of Animal Protein (ABPA), Brazil's pork exports reached 1.5 million metric tons in 2025, up 11.6% from 2024, and export revenue rose to USD 3.619 billion. At that scale, stable feed intake is commercially important, so flavors and sweeteners remain part of the routine formulation toolkit for integrated producers and contract growers. Brazil's push into demanding export markets also raises attention to approved additives and residue-compliant formulations, which support sensory additive adoption over older intake-support tools.

Commercial Feed Volume Expansion Across Brazil and the Broader Region

South America produced 204.446 million metric tons of compound feed in 2025, up 2.8% year over year, and Brazil alone accounted for 89.904 million metric tons according to Alltech Agri Food Statistics. This wider production base expands the addressable market for South America feed flavors and sweeteners, as most inclusions occur at the feed mill level. Higher throughput at larger mills also improves the economics of precision palatability systems, since fixed application and service costs are spread across more tonnage. Brazil and the Southern Cone carried much of that stability, even as smaller subregional markets saw localized disruption. That makes regional distribution coverage and local technical support important competitive tools in the South America feed flavors and sweeteners market.

Fragmented Feed-Mill Base Slows Premium Additive Penetration

The South America feed flavors and sweeteners market still operates through a widely dispersed feed manufacturing base outside the largest integrated protein companies. Smaller and mid-sized mills are often more price-sensitive and less able to run structured validation trials for premium sensory systems. That reduces the practical addressable market for high-specification products even when headline feed volume is large. Suppliers also face higher technical service costs per ton when accounts are scattered across many smaller customers. The result is slower premium penetration across parts of the South America feed flavors and sweeteners market, especially outside Brazil's production clusters.

Other drivers and restraints analyzed in the detailed report include:

- Higher Use of Sweeteners in Piglet and Young-Animal Diets

- Reformulation Toward Alternative Protein Sources Increases Demand for Palatability Solutions

- Ministry of Agriculture, Livestock and Supply (MAPA) Registration and Compliance Complexity for Sensory Additives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flavors hold the largest segment, captured 82.1% of the South America feed flavors and sweeteners market share in 2025, confirming their widespread use across swine, and ruminant diets in the region. Their leading position reflects the broad set of problems they address, including masking bitter raw materials, improving first-feed acceptance, and supporting intake in high-performance production systems. Flavors also fit well into both large integrated feed programs and more standardized premix-based formulations, which supports repeat demand in the South America feed flavors and sweeteners market. This breadth makes the flavor category structurally harder to displace, even as adjacent solution types improve.

Sweeteners remain the fastest-growing segment, projected to expand at a 4.3% CAGR through 2026 to 2031. The strongest pull comes from piglet weaning diets, where intake support directly affects early growth and feed conversion. ADM's SUCRAM and Adisseo's Optisweet demonstrate the way suppliers have developed technical solutions tailored to specific use cases, rather than positioning sweeteners solely as general flavor enhancers. This approach provides sweeteners with a more defined growth trajectory within the South America feed flavors and sweeteners market, despite flavors maintaining a higher overall market value.

Complete Report Scope:

- By Type

- Flavors

- Sweeteners

- By Animal Type

- Ruminants

- Beef Cattle

- Dairy Cattle

- Other Ruminants

- Swine

- Other Animal Type

- Ruminants

- By Geography

- Brazil

- Argentina

- Chile

- Rest of South America

List of Companies Covered in this Report:

- ADM

- Kerry Group plc

- Symrise AG

- BlueStar Adisseo Company

- Kemin Industries, Inc.

- dsm-firmenich AG

- Alltech

- Lucta, S.A.

- Prinova Group LLC

- Novonesis

- Cargill, Incorporated

- Phytobiotics Futterzusatzstoffe GmbH

- Norel, S.A.

- Orffa (Marubeni Corporation)

- BioAromas do Brasil

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Key Industry Trends

- 4.1 Animal Headcount Analysis

- 4.1.1 Ruminants

- 4.1.2 Swine

- 4.2 Feed Production Analysis

- 4.2.1 Ruminants

- 4.2.2 Swine

- 4.3 Regulatory Framework

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Export-led pork production growth

- 4.5.2 Commercial feed volume expansion across Brazil and the broader region

- 4.5.3 Higher use of sweeteners in piglet and young-animal diets

- 4.5.4 Increasing focus on feed efficiency and animal nutrition outcomes

- 4.5.5 Reformulation toward plant-protein and alternative raw materials increases masking needs

- 4.5.6 Antimicrobial phaseout raises demand for intake-preserving sensory reformulation

- 4.6 Market Restraints

- 4.6.1 Fragmented feed-mill base slows premium additive penetration

- 4.6.2 Ministry of Agriculture, Livestock and Supply (MAPA) registration and compliance complexity for sensory additives

- 4.6.3 Currency volatility raises the cost of imported micro-ingredients

- 4.6.4 Disease outbreaks and export restrictions disrupt additive purchasing patterns

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Type

- 5.1.1 Flavors

- 5.1.2 Sweeteners

- 5.2 By Animal Type

- 5.2.1 Ruminants

- 5.2.1.1 Beef Cattle

- 5.2.1.2 Dairy Cattle

- 5.2.1.3 Other Ruminants

- 5.2.2 Swine

- 5.2.3 Other Animal Type

- 5.2.1 Ruminants

- 5.3 By Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Chile

- 5.3.4 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market-Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 ADM

- 6.4.2 Kerry Group plc

- 6.4.3 Symrise AG

- 6.4.4 BlueStar Adisseo Company

- 6.4.5 Kemin Industries, Inc.

- 6.4.6 dsm-firmenich AG

- 6.4.7 Alltech

- 6.4.8 Lucta, S.A.

- 6.4.9 Prinova Group LLC

- 6.4.10 Novonesis

- 6.4.11 Cargill, Incorporated

- 6.4.12 Phytobiotics Futterzusatzstoffe GmbH

- 6.4.13 Norel, S.A.

- 6.4.14 Orffa (Marubeni Corporation)

- 6.4.15 BioAromas do Brasil

7 Market Opportunities and Future Outlook