PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073275

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073275

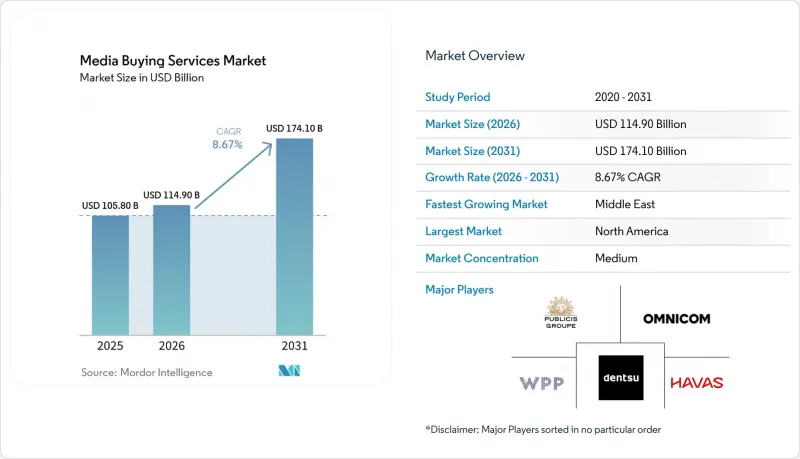

Media Buying Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the media buying services market size is projected to expand from USD 105.8 billion in 2025 and USD 114.9 billion in 2026 to USD 174.1 billion by 2031, registering a CAGR of 8.67% between 2026 to 2031.

This report is Segmented by Service Type (Media Strategy and Planning, Media Buying and Negotiation, Programmatic and Performance Buying, and More), Media Channel (Social Media Advertising, Display Advertising, and More), Organization Size (Large Enterprises, and More), End-User Industry (Retail and E-Commerce, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Media Buying Services Market Trends and Insights

Programmatic And AI-Driven Buying Becomes Core Agency Workflow

Programmatic advertising has moved from a specialist capability to a default execution layer across digital media. In Germany, BVDW projected that programmatic buying would account for 80% of the country's online display and video market in 2026, reaching EUR 6.5 billion, which equals USD 7.0 billion at the 2025 IRS average exchange rate. That shift changes agency selection criteria, because inventory access matters less when most buyers can reach the same pipes, and optimization logic matters more. The media buying services market is therefore placing more value on identity infrastructure, data models, and workflow automation than on manual execution alone. Agencies that cannot show a differentiated AI layer on top of standard platform access are facing stronger pressure on pricing and retention.

Budget Migration Toward Connected TV, Retail Media, And Digital Video

Connected TV and retail media are taking a larger share of new ad budgets, and that is changing where agencies create value. Dentsu projected global connected TV growth of 11.5% in 2026 and global retail media growth of 12.3% in the same year, which confirms that both channels are attracting outsized investment compared with the wider ad market. Retail media is gaining traction because it turns purchase intent data into an addressable and privacy-safe input for campaign planning. Agencies that can combine retail media signals with connected TV activation are building a tighter loop between exposure and purchase. That convergence is already shaping infrastructure choices, as shown by Stagwell's April 2026 integration with FreeWheel to create a unified connected TV activation layer.

Privacy Regulation And Signal Loss Reduce Targeting Precision

Privacy regulation has become a structural limit on addressable media rather than a narrow compliance issue. Cookie deprecation in major browsers and Apple's App Tracking Transparency framework have reduced the volume of deterministic identifiers available for planning and optimization. That loss of signal has made audience reach planning less efficient across the open web and more fragmented across identity systems. In the media buying services market, the burden falls harder on smaller agencies that do not have legal, data, and engineering support built into their operating model. The result is a tougher planning environment where campaign precision depends more on first-party assets and publisher relationships than it did a few years ago.

Other drivers and restraints analyzed in the detailed report include:

- Demand For Omnichannel Measurement And ROAS Accountability

- First-Party Data Activation And Privacy-Safe Audience Planning

- Ad Fraud, Brand Safety, And Viewability Risks Persist

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Media buying and negotiation retained 35.76% of service revenue in 2025, which kept this function at the center of the media buying services market size. That position remained durable because premium inventory in connected TV, sports, live news, and other high-value environments still relies heavily on direct deal structures. Buyers continue to value negotiated access, pricing discipline, and adjacency control in these environments. Those conditions keep human broker relationships relevant even as more execution shifts into software. This part of the media buying services market stayed resilient because clients still need certainty around premium placements and commercial terms.

Programmatic and performance buying is projected to record a 9.46% CAGR from 2026 to 2031, which makes it the fastest-growing service category in the media buying services market. Growth is tied to budget movement into open-web programmatic, private marketplaces, curated deals, and real-time optimization models. PubMatic said its AgenticOS platform had executed more than 30 fully autonomous end-to-end campaigns by Q1 2026, which showed how quickly workflow automation is moving into live buying operations. As transactional buying becomes more automated, agencies are placing more emphasis on strategy, analytics, and commerce activation as the fee-bearing layers of the media buying services market.

Search advertising held 31.44% of channel revenue in 2025, which preserved its lead within the media buying services market. Search keeps that position because it captures clear lower-funnel intent and supports direct brand-to-outcome attribution across many verticals. Advertisers still rely on search to anchor performance budgets, especially when return visibility matters more than broad awareness. That stability creates consistent demand for agencies that can manage bidding, keywords, budget pacing, and cross-channel allocation. The media buying services market still leans on search because it combines spend discipline with measurable outcomes.

Connected TV and OTT video are projected to expand at a 10.14% CAGR through 2031, which makes it the fastest-growing media channel in the media buying services market. Growth is being pushed by ad-supported streaming, changing viewing habits, and the addition of commerce data into video planning. In Japan, internet advertising media expenditure grew 11.8% in 2025, driven mainly by SNS vertical video, which aligned with the broader move toward video-led discovery and activation. Display, digital video, digital audio, digital out-of-home, and retail media networks remain important, but the sharpest change is happening where video inventory, audience data, and quality controls now meet.

Complete Report Scope:

- By Service Type

- Media Strategy and Planning

- Media Buying and Negotiation

- Programmatic and Performance Buying

- Campaign Management and Optimization

- Measurement and Analytics

- Others (Retail Media and Commerce Activation, Influencer and Creator Media Amplification, Media Consulting and In-Housing Support)

- By Media Channel

- Search Advertising

- Social Media Advertising

- Display Advertising

- Digital Video

- Connected TV and Over-the-Top Video

- Others (Retail Media Networks, Digital Audio and Podcasts, Radio, Print, OOH and DOOH)

- By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By End-User Industry

- Retail and E-commerce

- Media and Entertainment

- BFSI

- IT and Telecom

- Travel and Hospitality

- Healthcare

- Others (Automotive, Education, and Public sector)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America remained the largest regional base in the media buying services market in 2025, accounting for approximately 41.48% of global market revenue. The United States drives most regional revenue because it combines concentrated advertiser spending with mature programmatic infrastructure. The region also hosts many of the largest holding company networks and buying technology partners, which keeps scale advantages high. Canada remains a solid secondary market with strong digital adoption, while Mexico is still earlier in maturity but is moving forward through mobile-first buying patterns. This concentration keeps the media buying services market highly competitive in North America, even as data use, conduct, and platform dependence draw more attention.

Europe represented the second-largest geography in the media buying services market. Germany's online display and video advertising market is forecast to reach EUR 8.2 billion, which equals USD 8.9 billion in 2026, and programmatic is expected to account for 80% of transactions. France's advertising market reached EUR 19.8 billion, which equals USD 21.4 billion in 2025. Digital grew 11% in that year, and digital is forecast to grow another 7.5% in 2026. Consent-driven data rules and a stronger premium publisher base continue to push European buyers toward programmatic guaranteed and curated private marketplace deals over open-auction buying. Asia-Pacific is the fastest-growing large regional cluster in the media buying services market. Japan's total advertising spend crossed JPY 8,062.3 billion, which equals USD 53.4 billion in 2025, and internet advertising surpassed 50% of total ad investment for the first time. Hakuhodo DY ONE began programmatic TV buying through NTV's AdRM-Exchange in July 2025 and added a unique-reach maximization bidding function in October 2025, demonstrating how broadcast inventory is being integrated into programmatic workflows across the region.

South America remains smaller than North America and Europe, but its digital buying base is still expanding through mobile-led advertising activity. The Middle East and Africa also remain smaller in absolute scale; however, the Middle East is projected to be the fastest-growing regional segment during 2026-2031, registering a CAGR of 8.86%. Growth is being supported by increasing digital advertising investments, rapid connected TV adoption, expanding retail media ecosystems, and government-backed digital transformation initiatives in countries such as Saudi Arabia and the United Arab Emirates. The media buying services market is widening fastest where local execution expertise can connect global tools with country-specific media systems.

- WPP plc

- Omnicom Group Inc.

- Publicis Groupe S.A.

- Dentsu Group Inc.

- The Interpublic Group of Companies, Inc.

- Havas Group

- Hakuhodo DY Holdings Inc.

- Stagwell Inc.

- S4 Capital plc

- Accenture plc

- MiQ Digital Ltd.

- Horizon Media, Inc.

- PMG Worldwide LLC

- Tinuiti, Inc.

- The Trade Desk, Inc.

- Brandtech Group

- MiQ Digital

- Assembly Global

- Microsoft Corporation

- Criteo S.A.

- Adform A/S

- Viant Technology Inc.

- LiveRamp Holdings

- FreeWheel

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Programmatic and AI-Driven Buying Becomes Core Agency Workflow

- 4.2.2 Budget Migration Toward Connected TV, Retail Media, and Digital Video

- 4.2.3 Demand for Omnichannel Measurement and ROAS Accountability

- 4.2.4 First-Party Data Activation and Privacy-Safe Audience Planning

- 4.2.5 Curated Marketplaces and Supply Path Optimization Favor Specialist Buying Partners

- 4.2.6 Agentic AI Expands Outsourced Buying Among Mid-Market Brands

- 4.3 Market Restraints

- 4.3.1 Privacy Regulation and Signal Loss Reduce Targeting Precision

- 4.3.2 Ad Fraud, Brand Safety, and Viewability Risks Persist

- 4.3.3 Walled-Garden Measurement Gaps Limit Cross-Platform Optimization

- 4.3.4 Margin Compression from In-Housing and Platform Automation

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Media Strategy and Planning

- 5.1.2 Media Buying and Negotiation

- 5.1.3 Programmatic and Performance Buying

- 5.1.4 Campaign Management and Optimization

- 5.1.5 Measurement and Analytics

- 5.1.6 Others (Retail Media and Commerce Activation, Influencer and Creator Media Amplification, Media Consulting and In-Housing Support)

- 5.2 By Media Channel

- 5.2.1 Search Advertising

- 5.2.2 Social Media Advertising

- 5.2.3 Display Advertising

- 5.2.4 Digital Video

- 5.2.5 Connected TV and Over-the-Top Video

- 5.2.6 Others (Retail Media Networks, Digital Audio and Podcasts, Radio, Print, OOH and DOOH)

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 Retail and E-commerce

- 5.4.2 Media and Entertainment

- 5.4.3 BFSI

- 5.4.4 IT and Telecom

- 5.4.5 Travel and Hospitality

- 5.4.6 Healthcare

- 5.4.7 Others (Automotive, Education, and Public sector)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Qatar

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 WPP plc

- 6.4.2 Omnicom Group Inc.

- 6.4.3 Publicis Groupe S.A.

- 6.4.4 Dentsu Group Inc.

- 6.4.5 The Interpublic Group of Companies, Inc.

- 6.4.6 Havas Group

- 6.4.7 Hakuhodo DY Holdings Inc.

- 6.4.8 Stagwell Inc.

- 6.4.9 S4 Capital plc

- 6.4.10 Accenture plc

- 6.4.11 MiQ Digital Ltd.

- 6.4.12 Horizon Media, Inc.

- 6.4.13 PMG Worldwide LLC

- 6.4.14 Tinuiti, Inc.

- 6.4.15 The Trade Desk, Inc.

- 6.4.16 Brandtech Group

- 6.4.17 MiQ Digital

- 6.4.18 Assembly Global

- 6.4.19 Microsoft Corporation

- 6.4.20 Criteo S.A.

- 6.4.21 Adform A/S

- 6.4.22 Viant Technology Inc.

- 6.4.23 LiveRamp Holdings

- 6.4.24 FreeWheel

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment