PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073351

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073351

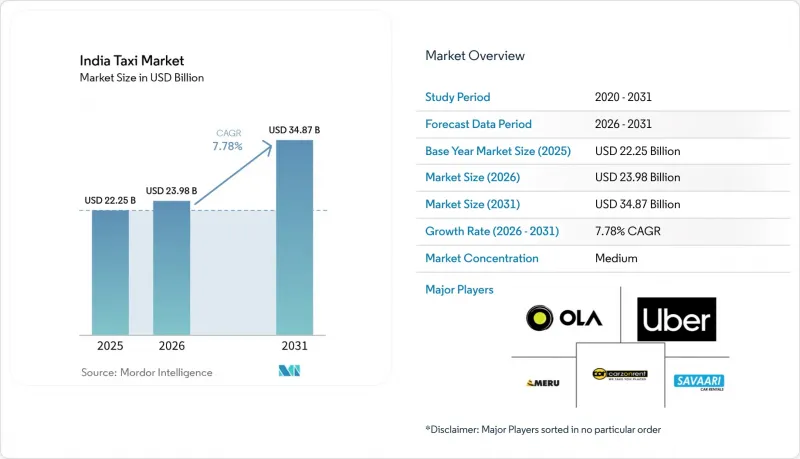

India Taxi - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, india taxi market size in 2026 is estimated at USD 23.98 billion, growing from 2025 value of USD 22.25 billion with 2031 projections showing USD 34.87 billion, growing at 7.78% CAGR over 2026-2031.

This report is Segmented by Booking Type (Online Booking and Offline Booking), Service Type (Ride-Hailing, Ride-Sharing/Car-Pooling, and More), Vehicle Type (Passenger Cars and More), Propulsion Type (ICE, Electric, and Hybrid), Trip Purpose (Intra-City Point-To-Point and More), and Customer Segment (Individual Consumers, Corporate/Institutional). The Market Forecasts are Provided in Terms of Value (USD).

India Taxi Market Trends and Insights

Smartphone Penetration & UPI-Enabled Digital Payments

UPI transaction volume grew exponentially in 2024, almost double the previous year's annual rise, which signals a permanent behavioral change in how riders pay for taxis. Millions of smartphone users already access ride apps, lowering cash dependence and enlarging target customer pools in tier-2 and tier-3 cities. Public transport systems mirror the adoption curve, as shown by Bangalore Metropolitan Transport Corporation collecting almost two-fifth of ticket revenue digitally in March 2025. Platforms adapt by piloting cash-only auto-rickshaw services that still employ in-app matching, confirming that digital contact does not always equal digital settlement. Biometric authentication and credit-linked UPI innovations further tighten security, encouraging corporate accounts to centralize travel spend under a single dashboard. As a result, the Indian taxi market leverages smoother booking funnels and better repeat ride conversion.

Urban Congestion & Less than 2% Private Car Ownership

Private car penetration remains minimal, and urban cores face daily congestion that stifles productivity. Tier-2 and tier-3 cities already generate three-fifths of GDP, see population densities soar, underpinning long-run dependence on shared mobility in the India taxi market. The UDAN regional airport scheme activated 625 routes serving multiple passengers, creating immediate last-mile taxi needs. Asset-light corporate mobility providers such as Ecos Mobility run 12,000 vehicles for 1,100 enterprises, validating subscription fleets as congestion countermeasures. Flexible work setups widen travel peaks across the day, so dynamic fleet allocation helps operators lift utilization while smoothing traffic loads

Commission & Surge-Price Caps

Regulatory ceilings restrict commissions to one-fifth of fare and limit surge multipliers to 2X, trimming peak-hour revenue potential. Driver associations claim that take rates nearly half persist in practice, leading to protests across Delhi in 2025 that disrupted service availability. Maharashtra now enforces minimal cancellation penalties on drivers and less than one-tenth on riders, applying Regional Transport Authority audits to contain side payments. With lower elasticity to pass through fuel spikes, operators pivot toward fixed-fee subscriptions that comply with caps yet stabilize driver income. Such shifts may blunt near-term margin expansion but could lift retention and support long-term growth in the India taxi market over time.

Other drivers and restraints analyzed in the detailed report include:

- Government EV Push (FAME-II and State Policies)

- Airport Traffic Boom Powering Pre-Scheduled Rides

- Rider Safety Issues & Driver Attrition

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Online reservations accounted for 70.84% of the Indian taxi market in 2025 and are projected to expand at a 7.80% CAGR through 2031. Offline hail retains almost three-tenth, but its share keeps falling as smartphone literacy spreads in tier-2 corridors. The Taxi market in india size associated with online booking is poised to widen yearly because payments over UPI remain fee-free for riders and drivers.

The Open Network for Digital Commerce partnership lets platforms like Namma Yatri migrate toward subscription models that directly leave fare collections to riders and drivers, cutting aggregator commissions while preserving app visibility. Cooperatives under the new Sahkar Taxi program further shrink the middle-layer margin, though they still rely on app interfaces classified as digital booking in market definitions. Regulatory guidance is yet to harmonize data-sharing protocols, but the trajectory toward universal digital engagement appears locked in.

Ride-hailing produced 65.10% of the Indian taxi market revenue in 2025, while ride-sharing and car-pooling are expected to clock an 7.98% CAGR to 2031. Price-sensitive commuters choose shared trips during peak pricing windows because caps narrow the differential to solo rides.

State rules in Maharashtra formalize car-pool safety norms that boost female ridership confidence, helping share platforms retain loyalty. Corporate leasing and subscription fleets supply predictable monthly spend for employers that need last-mile shuttles in hybrid work models. As congestion continues, public policy encourages higher occupancy per vehicle, positioning ride-sharing to edge ride-hailing growth in the Indian taxi market.

Complete Report Scope:

- By Booking Type

- Online Booking

- Offline Booking

- By Service Type

- Ride-Hailing

- Ride-Sharing / Car-Pooling

- Subscription & Corporate Leasing

- By Vehicle Type

- Passenger Cars

- Two-Wheelers

- Three-Wheeler Auto-Rickshaws

- Vans & MPVs

- By Propulsion Type

- ICE (Petrol/Diesel/CNG)

- Electric

- Hybrid

- By Trip Purpose

- Intra-city Point-to-Point

- Airport Transfers

- Outstation / Inter-city

- Corporate Mobility

- By Customer Segment

- Individual Consumers

- Corporate / Institutional

List of Companies Covered in this Report:

- ANI Technologies Pvt Ltd (Ola Cabs)

- Uber Technologies Inc.

- Rapido

- Meru Mobility Tech Pvt Ltd

- BlUSmart Mobility Pvt Ltd

- Carzonrent India Pvt Ltd

- NTL FastTrack Taxi

- Savaari Car Rentals

- inDrive

- Spice Cabs

- Mega Cabs

- BlaBlaCar

- Evera Cabs

- Jugnoo

- Zoomcar India Pvt Ltd

- TaxiForSure

- Bounce Infinity

- Yulu Bikes

- Sahkar Taxi (Co-operative)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smartphone Penetration & UPI-Enabled Digital Payments

- 4.2.2 Urban Congestion & Less than 2 % Private Car Ownership

- 4.2.3 Government EV Push (Fame-Ii, State EV Policies)

- 4.2.4 Airport Traffic Boom Powering Pre-Scheduled Rides

- 4.2.5 Cooperative/Tier-III Fleet Model Expansion

- 4.2.6 AI-Based Mobility-As-A-Service (Maas) Integrations

- 4.3 Market Restraints

- 4.3.1 Commission & Surge-Price Caps (MV Aggregator Rules 2020)

- 4.3.2 High EV Total-Cost-of-Ownership & Financing Gaps

- 4.3.3 Rider-Safety Issues & Driver Attrition

- 4.3.4 Regulatory Fragmentation Across Indian States

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Booking Type

- 5.1.1 Online Booking

- 5.1.2 Offline Booking

- 5.2 By Service Type

- 5.2.1 Ride-Hailing

- 5.2.2 Ride-Sharing / Car-Pooling

- 5.2.3 Subscription & Corporate Leasing

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Two-Wheelers

- 5.3.3 Three-Wheeler Auto-Rickshaws

- 5.3.4 Vans & MPVs

- 5.4 By Propulsion Type

- 5.4.1 ICE (Petrol/Diesel/CNG)

- 5.4.2 Electric

- 5.4.3 Hybrid

- 5.5 By Trip Purpose

- 5.5.1 Intra-city Point-to-Point

- 5.5.2 Airport Transfers

- 5.5.3 Outstation / Inter-city

- 5.5.4 Corporate Mobility

- 5.6 By Customer Segment

- 5.6.1 Individual Consumers

- 5.6.2 Corporate / Institutional

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 ANI Technologies Pvt Ltd (Ola Cabs)

- 6.4.2 Uber Technologies Inc.

- 6.4.3 Rapido

- 6.4.4 Meru Mobility Tech Pvt Ltd

- 6.4.5 BluSmart Mobility Pvt Ltd

- 6.4.6 Carzonrent India Pvt Ltd

- 6.4.7 NTL FastTrack Taxi

- 6.4.8 Savaari Car Rentals

- 6.4.9 inDrive

- 6.4.10 Spice Cabs

- 6.4.11 Mega Cabs

- 6.4.12 BlaBlaCar

- 6.4.13 Evera Cabs

- 6.4.14 Jugnoo

- 6.4.15 Zoomcar India Pvt Ltd

- 6.4.16 TaxiForSure

- 6.4.17 Bounce Infinity

- 6.4.18 Yulu Bikes

- 6.4.19 Sahkar Taxi (Co-operative)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment