PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073367

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073367

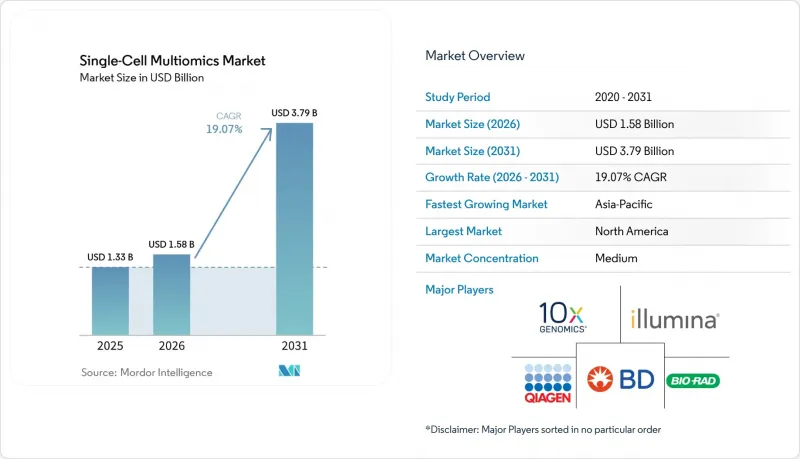

Single-Cell Multiomics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the single-cell multiomics market size in 2026 is estimated at USD 1.58 billion, growing from 2025 value of USD 1.33 billion with 2031 projections showing USD 3.79 billion, growing at 19.07% CAGR over 2026-2031.

This report is Segmented by Product (Instruments & Platforms and More), Technology Platform (Droplet-Based Microfluidics, and More), Omics Modality (Genomics, and More), Application (Oncology, Neurology, and More), Workflow Step (Cell Isolation & Sorting, and More), End User (Academic & Research Institutes, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Single-Cell Multiomics Market Trends and Insights

Technological Advances in Single-Cell Analysis

New chemistries double detected-gene counts while cutting per-cell costs by half, as illustrated by GEM-X upgrades that also capture fragile neutrophils more efficiently. Spatial workflows now fuse DNA, RNA, protein, and morphology in under 24 hours through AVITI24 systems, closing the gap between histology and molecular profiling elementbiosciences.com. Intelligent microfluidics, enhanced by object-detection algorithms, achieve 98% cell-identification precision and elevate throughput.These cumulative gains shorten project timelines, broaden assay menus, and push the single-cell multiomics market deeper into translational research.

Rising Burden of Chronic and Infectious Diseases

Single-cell interrogation uncovers how individual tumor clones or immune subsets drive divergent therapy responses, informing treatment algorithms that improve survival odds. During COVID-19, rapid immune-cell profiling demonstrated the technology's ability to map real-time responses, accelerating vaccine research cycles. Aging populations propel neurology programs that deploy spatial maps to pinpoint Alzheimer's-linked cell states. Tumor-microenvironment atlases now predict immunotherapy outcomes in hepatocellular carcinoma studies showcased at AACR 2024. The need for granular insight into disease heterogeneity sustains multi-year funding streams that expand the single-cell multiomics market footprint.

High Capital and Reagent Costs

Turn-key spatial platforms can list above USD 500,000, and full-stack multiomics reagents still range from USD 50-200 per cell, restricting routine implementation. Academic cores adopt shared-instrument models that lengthen queue times. Contract research organizations offset capital burdens but add scheduling delays, prompting labs to prioritize grant-backed projects. Vendors respond by consolidating assays into single instruments to widen amortization bases. Until unit-economics improve, budget constraints temper the near-term expansion speed of the single-cell multiomics market.

Other drivers and restraints analyzed in the detailed report include:

- Precision-Oncology & Immunology Adoption

- Sequencing-Cost Reductions & Ultra-High-Throughput Platforms

- Bioinformatics-Talent Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Instruments and platforms accounted for 45.78% of the single-cell multiomics market share in 2025, reflecting the indispensable role of precision hardware in assay quality. Broadening assay menus and integration of sequencing and imaging into unified chassis further cement their position. Software and services, though smaller, are growing fastest at 22.86% CAGR as cloud pipelines and AI dashboards become routine. The single-cell multiomics market size for software and services is projected to add USD 0.66 billion between 2026-2031, mirroring lab demand for turnkey analytics. Recurring reagent revenue underpins vendor profitability, funding next-gen platform R&D that widens performance gaps against earlier models.

Continuous hardware innovation-illustrated by platforms that process 20,000 cells per run while capturing transcriptome and protein data-keeps capital budgets directed toward upgrades. On the services front, contract analytics groups scale by offering pay-per-dataset models, allowing small biotech teams to tap advanced pipelines without infrastructure. Synergy between hardware and cloud software fosters ecosystem lock-in, reinforcing the expansion trajectory of the single-cell multiomics market.

Droplet-based workflows captured 57.84% revenue in 2025, benefiting from mature chemistries, abundant reagent kits, and proven scalability. High-throughput labs favor droplet systems for population-scale atlases that demand millions of barcoded cells. Spatial-omics, while newer, is rising at 23.9% CAGR as tumor-microenvironment mapping moves toward the clinic. The single-cell multiomics market size for spatial-omics is expected to triple by 2031, supported by tissue-context biomarkers in oncology.

Hybrid strategies now emerge: instruments inject droplet-partitioned cells onto slides for secondary spatial staining, combining throughput with context. Nanowell and combinatorial indexing platforms remain options where cost or sample type mandates alternative formats. Yet droplet incumbents invest heavily in R&D, extending chemistry lifecycles and defending their hold on the single-cell multiomics market.

Complete Report Scope:

- By Product

- Instruments & Platforms

- Reagents & Consumables

- Software & Services

- By Technology Platform

- Droplet-based Microfluidics

- Nanowell / Combinatorial Indexing

- Spatial-omics Platforms

- By Omics Modality

- Genomics

- Transcriptomics

- Proteomics

- Metabolomics

- By Application

- Oncology

- Neurology

- Cell Biology & Developmental Biology

- Immunology & Infectious Disease

- By Workflow Step

- Cell Isolation & Sorting

- Library Preparation & Barcoding

- Sequencing & Imaging Platforms

- Data Analysis & Visualisation

- By End User

- Academic & Research Institutes

- Biotechnology & Pharmaceutical Companies

- Contract Research Organisations

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America accounted for 40.78% revenue in 2025, underpinned by NIH-funded precision-medicine programs, deep venture capital pools, and early technology adoption. Collaborations between sequencer manufacturers and cloud-compute vendors normalize AI-enabled genomics dashboards, positioning the region at the forefront of integrative workflows. Academic-industry consortia translate bench discoveries into clinical assays at a pace unmatched elsewhere, sustaining premium pricing within the single-cell multiomics market.

Asia Pacific, projected to grow at 20.98% CAGR, benefits from government-backed cell-atlas projects and domestic instrument manufacturing. China's multi-billion-cell initiatives harness large-scale sequencing to chart tissue diversity, while Japanese centers target age-related neurological disorders with single-cell resolution. Price-sensitive sub-markets spur demand for cost-optimized kits, prompting global vendors to localize production. These dynamics expand the regional single-cell multiomics market despite infrastructure disparities across countries.

Europe occupies a technologically sophisticated but regulation-intensive landscape. Horizon grants sustain academic demand, and pharma clusters in Germany and the United Kingdom integrate single-cell assays into drug-discovery pipelines. Yet GDPR compliance hurdles complicate cross-border data exchanges, slowing multi-site oncology studies and nudging enterprises toward privacy-enhancing computation stacks. Despite these frictions, high-value proteomics acquisitions signal investor confidence, anchoring Europe as a stable, if slower-growing, node in the global single-cell multiomics market.

- 10x Genomics Inc.

- Illumina

- Beckton Dickinson

- NanoString Technologies Inc.

- Standard BioTools Inc.

- Mission Bio Inc.

- Vizgen Inc.

- QIAGEN

- Takara Bio

- Bio-Rad Laboratories

- BGI Genomics Co. Ltd.

- Parse Biosciences Inc.

- Singular Genomics Systems Inc.

- Pacific Biosciences (PacBio)

- Roche

- Cellenion SAS

- Olink Proteomics AB

- Dolomite Bio

- Fluent BioSciences

- STRATEC SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing R&D And Technological Advances In Single-Cell Analysis

- 4.2.2 Rising Burden Of Chronic & Infectious Diseases

- 4.2.3 Rapid Adoption Of Multiomics In Precision Oncology & Immunology

- 4.2.4 Sequencing-Cost Reductions & Ultra-High-Throughput Platforms

- 4.2.5 AI-Enabled Analytics Pipelines Streamline Multiomic Workflows

- 4.2.6 Commercialisation Of Spatial Multiomics With In-Situ Resolution

- 4.3 Market Restraints

- 4.3.1 High Capital & Reagent Costs Of Single-Cell Workflows

- 4.3.2 Data-Analysis Complexity & Bioinformatics-Talent Shortage

- 4.3.3 Sample-Prep Biases Causing Loss Of Fragile Cell Populations

- 4.3.4 Heightened Privacy Regulations On Genomic Data Sharing

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Product

- 5.1.1 Instruments & Platforms

- 5.1.2 Reagents & Consumables

- 5.1.3 Software & Services

- 5.2 By Technology Platform

- 5.2.1 Droplet-based Microfluidics

- 5.2.2 Nanowell / Combinatorial Indexing

- 5.2.3 Spatial-omics Platforms

- 5.3 By Omics Modality

- 5.3.1 Genomics

- 5.3.2 Transcriptomics

- 5.3.3 Proteomics

- 5.3.4 Metabolomics

- 5.4 By Application

- 5.4.1 Oncology

- 5.4.2 Neurology

- 5.4.3 Cell Biology & Developmental Biology

- 5.4.4 Immunology & Infectious Disease

- 5.5 By Workflow Step

- 5.5.1 Cell Isolation & Sorting

- 5.5.2 Library Preparation & Barcoding

- 5.5.3 Sequencing & Imaging Platforms

- 5.5.4 Data Analysis & Visualisation

- 5.6 By End User

- 5.6.1 Academic & Research Institutes

- 5.6.2 Biotechnology & Pharmaceutical Companies

- 5.6.3 Contract Research Organisations

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 Australia

- 5.7.3.5 South Korea

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 10x Genomics Inc.

- 6.3.2 Illumina Inc.

- 6.3.3 BD

- 6.3.4 NanoString Technologies Inc.

- 6.3.5 Standard BioTools Inc.

- 6.3.6 Mission Bio Inc.

- 6.3.7 Vizgen Inc.

- 6.3.8 Qiagen N.V.

- 6.3.9 Takara Bio Inc.

- 6.3.10 Bio-Rad Laboratories Inc.

- 6.3.11 BGI Genomics Co. Ltd.

- 6.3.12 Parse Biosciences Inc.

- 6.3.13 Singular Genomics Systems Inc.

- 6.3.14 Pacific Biosciences (PacBio)

- 6.3.15 F. Hoffmann-La Roche Ltd

- 6.3.16 Cellenion SAS

- 6.3.17 Olink Proteomics AB

- 6.3.18 Dolomite Bio

- 6.3.19 Fluent BioSciences

- 6.3.20 STRATEC SE

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment