PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073372

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073372

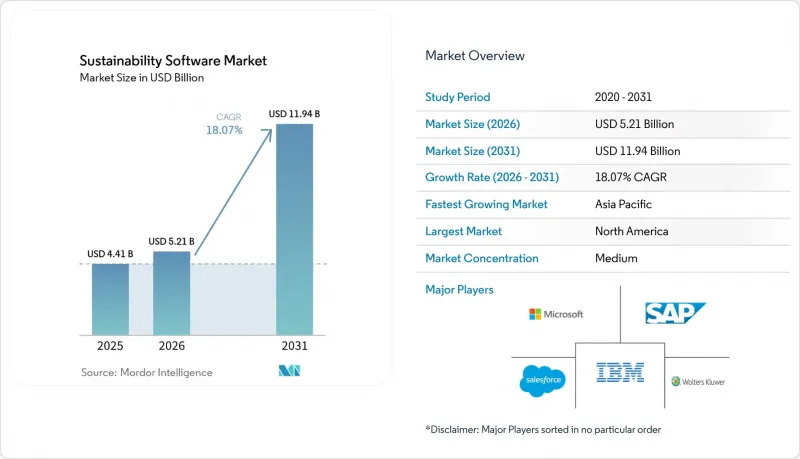

Sustainability Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the sustainability software market size was valued at USD 4.41 billion in 2025 and estimated to grow from USD 5.21 billion in 2026 to reach USD 11.94 billion by 2031, at a CAGR of 18.07% during the forecast period (2026-2031).

This report is Segmented by Deployment Mode (Cloud, On-Premise, and Hybrid), Software Category (Carbon Management Software, Sustainability Reporting and Management (ESG), and More), End-User Enterprise Size (Large Enterprises, and More), End-User Industry (Government and Public Sector, BFSI, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Sustainability Software Market Trends and Insights

ESG-Disclosure Regulations Tightening Worldwide

Binding rules elevate the sustainability software market from optional analytics to mandatory infrastructure. SEC and EU mandates now attach material penalties to inaccurate or missing carbon data, driving enterprise-wide roll-outs ahead of phased submission deadlines. Continuous platform demand is expected through 2028 as successive filing tiers take effect

Corporate Net-Zero Commitments Boost Carbon Accounting Demand

Ambitious targets require granular tracking of Scope 1-3 emissions through carbon management software. Microsoft's pledge to reach carbon negativity by 2030, backed by more than 34 GW of contracted renewable power, illustrates how software enables project oversight and removal verification . As investors link ESG outcomes to capital access, robust data systems become essential for executive accountability.

Shortage of Skilled Sustainability Data Analysts

Demand for ESG talent exceeds supply as 71% of manufacturers plan departmental expansion yet struggle to recruit carbon-accounting specialists. Reliance on consultants raises project costs and slows internal capability building, particularly among mid-market firms.

Other drivers and restraints analyzed in the detailed report include:

- Cost Savings From Energy and Resource Optimisation Analytics

- AI-Driven Scope-3 Data Capture and Automation

- High Upfront Cost of Enterprise-Grade Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The sustainability software market saw cloud deployment hold a dominant 59.78% sustainability software market share in 2025, while hybrid configurations are forecast to post a 19.02% CAGR through 2031. Hybrid models blend cloud analytics with on-premise edge processing, letting firms comply with data-residency laws yet maintain AI-heavy forecasting capabilities. Energy producers and manufacturers integrate platforms like Schneider Electric's hybrid suite to synchronise plant-floor sensors with cloud dashboards, capturing immediate efficiency gains . Hybrid adoption therefore satisfies both compliance and operational imperatives, positioning it as the next driver of sustainability software market expansion.

Hybrid architectures also future-proof investments because enterprises can shift processing loads between environments as regulations evolve. Cyber-security postures improve when sensitive operational data never leaves controlled premises, yet aggregated insights still reside in secure clouds for enterprise-level reporting. This flexibility is forecast to accelerate penetration in highly regulated sectors such as power utilities and pharmaceuticals, reinforcing the sustainability software market's resilience to changing policy landscapes.

Sustainability reporting and management (ESG) captured 39.45% of revenue in 2025, but supply-chain sustainability applications are on track for a 19.25% CAGR to 2031, reflecting urgent Scope 3 challenges. Automated freight-emission modules, enabled by Blue Yonder's Pledge acquisition, give logistics managers real-time CO2e dashboards and instant compliance formatting. Such capabilities extend platform value beyond corporate reporting into day-to-day procurement and transport optimisation, widening the sustainability software market addressable base.

Growth also stems from multinational suppliers needing to present standardised data to many customers. AI bots request, validate and normalise figures across thousands of vendors, reducing duplicative manual outreach. As adoption spreads downstream, supply-chain tools are poised to surpass core ESG modules in incremental revenue contribution, underscoring a structural shift in the sustainability software market.

Complete Report Scope:

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Software Category

- Carbon Management Software

- Sustainability Reporting and Management (ESG)

- Energy and Resource Optimisation

- Compliance and Risk Management

- Supply-Chain Sustainability

- Environment, Health and Safety (EHS)

- By End-user Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-User Industry

- Government and Public Sector

- BFSI

- IT and Telecom

- Manufacturing and Industrial

- Healthcare and Life Sciences

- Energy and Utilities

- Consumer Goods and Retail

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America held 41.62% sustainability software market share in 2025 as the SEC disclosure rule, plus strengthened federal procurement guidelines, compelled fast adoption. Enterprises rushed to instrument assets and align financial statements with mandated carbon data, while abundant venture funding supported start-ups building vertical AI models. Mature consulting ecosystems further eased implementation.

Asia-Pacific is projected to register an 18.31% CAGR to 2031, the highest regional pace. China will require over 300 publicly listed firms to publish sustainability reports by 2026, and Singapore's exchanges demand climate reporting for most issuers . Rapid industrialisation produces immediate efficiency gains when software recommends equipment retrofits, bolstering ROI arguments across manufacturing corridors from Shenzhen to Chennai.

Europe continues strong regulatory-driven uptake through the Corporate Sustainability Reporting Directive covering more than 51,000 entities. European Sustainability Reporting Standards call for granular double-materiality assessments, driving demand for automated data tagging and audit trails. German multinationals integrating hybrid software with industrial controls showcase regional expertise that influences global best practice.

- Microsoft Corporation

- SAP SE

- IBM Corporation

- Salesforce, Inc.

- Wolters Kluwer N.V.

- Nasdaq, Inc.

- Diligent Corporation

- Benchmark Digital Partners LLC (Benchmark ESG)

- Schneider Electric SE

- Greenly SAS

- Workiva Inc.

- Persefoni Inc.

- EcoVadis SAS

- Sphera Solutions, Inc.

- Enablon (Schneider Electric subsidiary)

- VelocityEHS

- Cority Software Inc.

- Plan A Earth GmbH

- Carbmee GmbH

- Siemens AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 ESG-disclosure regulations tightening worldwide

- 4.2.2 Corporate net-zero commitments boost carbon accounting demand

- 4.2.3 Cost-savings from energy and resource optimisation analytics

- 4.2.4 Investor and stakeholder pressure for transparent ESG data

- 4.2.5 AI-driven Scope-3 data capture and automation

- 4.2.6 Convergence of ESG and financial reporting platforms

- 4.3 Market Restraints

- 4.3.1 Shortage of skilled sustainability data analysts

- 4.3.2 High upfront cost of enterprise-grade platforms

- 4.3.3 Data-sovereignty hurdles for cross-border cloud deployment

- 4.3.4 ESG backlash in certain US states dampening adoption

- 4.4 Value / Supply-Chain Analysis

- 4.5 Evaluation of Critical Regulatory Framework

- 4.6 Impact Assessment of Key Stakeholders

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macro-economic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud

- 5.1.2 On-Premises

- 5.1.3 Hybrid

- 5.2 By Software Category

- 5.2.1 Carbon Management Software

- 5.2.2 Sustainability Reporting and Management (ESG)

- 5.2.3 Energy and Resource Optimisation

- 5.2.4 Compliance and Risk Management

- 5.2.5 Supply-Chain Sustainability

- 5.2.6 Environment, Health and Safety (EHS)

- 5.3 By End-user Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 Government and Public Sector

- 5.4.2 BFSI

- 5.4.3 IT and Telecom

- 5.4.4 Manufacturing and Industrial

- 5.4.5 Healthcare and Life Sciences

- 5.4.6 Energy and Utilities

- 5.4.7 Consumer Goods and Retail

- 5.4.8 Other Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 SAP SE

- 6.4.3 IBM Corporation

- 6.4.4 Salesforce, Inc.

- 6.4.5 Wolters Kluwer N.V.

- 6.4.6 Nasdaq, Inc.

- 6.4.7 Diligent Corporation

- 6.4.8 Benchmark Digital Partners LLC (Benchmark ESG)

- 6.4.9 Schneider Electric SE

- 6.4.10 Greenly SAS

- 6.4.11 Workiva Inc.

- 6.4.12 Persefoni Inc.

- 6.4.13 EcoVadis SAS

- 6.4.14 Sphera Solutions, Inc.

- 6.4.15 Enablon (Schneider Electric subsidiary)

- 6.4.16 VelocityEHS

- 6.4.17 Cority Software Inc.

- 6.4.18 Plan A Earth GmbH

- 6.4.19 Carbmee GmbH

- 6.4.20 Siemens AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-need Assessment