PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073388

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073388

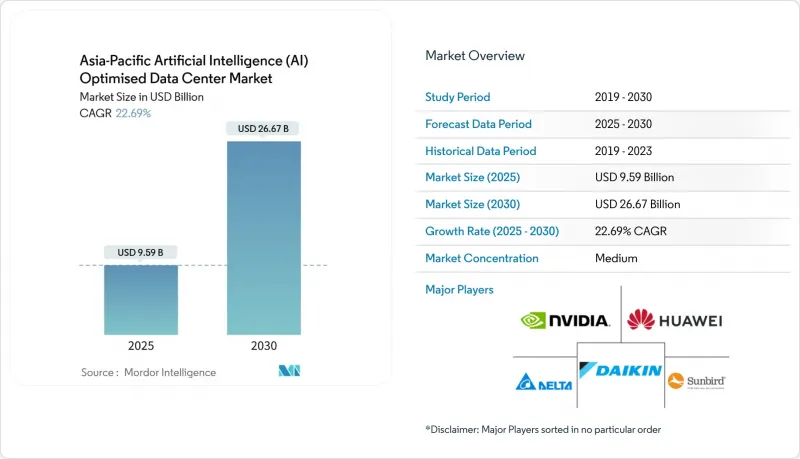

Asia-Pacific Artificial Intelligence (AI) Optimised Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

According to Mordor Intelligence, the asia-Pacific artificial intelligence data center market is valued at USD 9.59 billion in 2025 and, at a 22.69% CAGR, is forecast to reach USD 26.67 billion by 2030, underscoring the strongest five-year expansion yet seen in regional digital infrastructure spending.

This report is Segmented by Data Center Type (Cloud Service Providers, Colocation Data Centers, and More), Component (Hardware, Software Technology, and Services), Tier Standard (Tier III and Tier IV), End-User Industry (IT and IT Services, Internet and Digital Media, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Artificial Intelligence (AI) Optimised Data Center Market Trends and Insights

Government-backed AI compute subsidies drive infrastructure acceleration

South Korea's USD 7 billion AI program, aimed at strengthening the artificial intelligence-optimised data center ecosysyem, 400% above prior infrastructure budgets, directs 60% of funds to domestic capacity additions, compressing build timelines to less than 18 months. China's requirement that 80% of AI-training workloads remain onshore by 2026 has produced the region's highest colocation pre-lease rates and propelled GPU inventory stockpiling to hedge export-control risk. Across ASEAN, similar mandates lift sovereign-cloud premiums by 25-30%, especially in Singapore, where certified facilities already command the lowest vacancy in Asia.

Hyperscale cloud build-outs reshape Southeast Asian infrastructure

Google's USD 3 billion plan for Thailand and Malaysia confirms the power-grid advantage these markets hold over legacy hubs, while Microsoft's USD 1.7 billion Indonesian sovereign-cloud region positions the company ahead of Jakarta's 2025 data-localization deadline. Each hyperscaler requires parcel-level transformer blocks of 100 MW or more, incentivizing industrial-park locations that can bypass urban grid queues.

Power-infrastructure shortages constrain Tier-2 city expansion

In Pune, Hyderabad, and Chennai, grid allocations trail data-center demand by up to 40%, pushing connection waits beyond 18 months and forcing developers into higher-cost renewable PPA structures. Although green power softens emissions profiles, added capex inflates project IRR hurdles by as much as 300 basis points.

Other drivers and restraints analyzed in the detailed report include:

- AI-led retrofit of brownfield facilities to liquid cooling

- Surging generative-AI inference traffic at telecom edge nodes

- ASIC/GPU export controls impact supply lead-times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Colocation facilities captured 28.35% of spend yet will expand at 24.23% CAGR, eclipsing hyperscale's growth as sovereign-AI rules make domestic rack control mandatory for banks, insurers, and government ministries. Hyperscalers retain a 55.82% lead, but their Asia-Pacific artificial intelligence data center market share has plateaued as on-prem and edge nodes proliferate. Colocation operators that pre-provision liquid cooling and 20+ MW transformer blocks win outsized pre-leases, particularly in Singapore and Kuala Lumpur where land caps limit greenfield scale. Enterprise and edge deployments, favored by Japanese keiretsu, absorb export-control risk by retaining physical GPU custody. The Asia-Pacific artificial intelligence data center market size tied to enterprise on-prem nodes will cross USD 3 billion by 2030, reflecting a sustained diversification away from public cloud. Over the forecast horizon, hyperscaler build-outs are expected to consolidate around five power-rich corridors, cementing their role in training workloads while offloading latency-critical inference to edge colo pods.

Across 2025-2030, hyperscaler expansion pledges, Microsoft's USD 2.9 billion in Japan and Google's USD 3 billion in mainland Southeast Asia, lift the segment's historic 18.4% CAGR to 21.8%. Providers that integrate submarine-cable landing rights with direct GPU capacity create a defensible moat against domestic competitors. Meanwhile, the Asia-Pacific artificial intelligence data center market continues to reward colocation groups that obtain AI-governance stamps and bundle low-latency interconnect fabrics, allowing tenants to stitch private clusters to hyperscale GPUs when export limits relax.

Software still commands 45.83% of 2024 spend because model frameworks, orchestration layers, and observability platforms remain foundational for AI buildout. Yet hardware, the fastest rising slice at 23.67% CAGR, is forecast to top USD 10 billion of Asia-Pacific artificial intelligence data center market size by 2030, propelled by the pivot from cloud-based experimentation to at-scale inference clusters that stress rack density thresholds. Operators now reserve more than half of 2025-capex for cooling loops, busways, and medium-voltage switchgear that can sustain thermals above 40 kW per rack.

Power and cooling swallows the largest hardware outlay; each GPU rack draws up to 10X the current of a CPU rack, pushing many halls to 30 MVA utility feeds. Liquid-cooling procurement alone is growing at 35% annually in Japan, raising the country's Asia-Pacific artificial intelligence data center market share inside the hardware category. Services, representing 31.52% of spend, are skewing toward managed offerings as customers outsource tuning of replicas, gradient checkpoints, and energy-aware scheduling. Professional-services growth lags as hyperscalers internalize design skills and smaller providers rely on reference architectures from vendors like Schneider Electric. Across the region, supply-chain constraints in GPUs and network fabric cause operators to hold three-month inventory buffers, tying up working capital but ensuring deployment continuity.

Complete Report Scope:

- By Data Center Type

- Cloud Service Providers

- Colocation Facilities

- Enterprise / On-Prem / Edge

- By Component

- Hardware

- Power Infrastructure

- Cooling Infrastructure

- IT Equipment

- Racks and Other Hardware

- Software Technology

- Machine Learning

- Deep Learning

- Natural Language Processing

- Computer Vision

- Services

- Managed Services

- Professional Services

- Hardware

- By Tier Standard

- Tier III

- Tier IV

- By End-user Industry

- IT and ITES

- Internet and Digital Media

- Telecom Operators

- BFSI

- Healthcare and Life Sciences

- Manufacturing and Industrial IoT

- Government and Defense

- By Country

- China

- Japan

- India

- Malaysia

- South Korea

- Singapore

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- Alibaba Cloud (Alibaba Group)

- Tencent Cloud

- Amazon Web Services

- Microsoft Azure

- Google Cloud

- Huawei Technologies

- NVIDIA Corp.

- Advanced Micro Devices

- Baidu Inc.

- NTT Global Data Centers

- Equinix Inc.

- Digital Realty

- STT GDC

- GDS Holdings

- Yotta Infrastructure

- AirTrunk

- OneAsia Network

- Sunbird Software

- Nlyte Software

- Schneider Electric

- Delta Electronics

- Vertiv Group

- Fuji Electric

- Daikin Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hyperscale cloud build-outs in Southeast Asia

- 4.2.2 Government-backed AI compute subsidies in China and South Korea

- 4.2.3 AI-led retrofit of brownfield facilities to liquid cooling

- 4.2.4 Surging generative-AI inference traffic at telecom edge nodes

- 4.2.5 On-prem GPU clusters by Japanese keiretsu manufacturers

- 4.2.6 Sovereign-AI mandates accelerating ASEAN colo pre-leasing

- 4.3 Market Restraints

- 4.3.1 Acute transformer-grade power shortages in Tier-2 Indian cities

- 4.3.2 ASIC/GPU export controls impacting supply lead-times

- 4.3.3 Rising seawater-intake restrictions on coastal mega-sites

- 4.3.4 Talent crunch for AI-optimized DC-IM software engineers

- 4.4 Impact on Sustainability and Carbon-Neutral Energy Goals

- 4.4.1 Sustainable Power Source and Management

- 4.4.1.1 Renewable vs Non-Renewable Sources of Power (Green DCs and AI Innovations)

- 4.4.1.2 Carbon-Footprint Reduction (Heat Pumps, District Cooling and Heating, others)

- 4.4.2 Sustainable Cooling Solutions and Management

- 4.4.2.1 Efficient Cooling Solutions for AI-Optimised DCs

- 4.4.2.2 PUE Ratio, WUE Ratio - Analysis

- 4.4.1 Sustainable Power Source and Management

- 4.5 Industry Ecosystem Analysis

- 4.6 Regulatory or Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Data Center Type

- 5.1.1 Cloud Service Providers

- 5.1.2 Colocation Facilities

- 5.1.3 Enterprise / On-Prem / Edge

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.1.1 Power Infrastructure

- 5.2.1.2 Cooling Infrastructure

- 5.2.1.3 IT Equipment

- 5.2.1.4 Racks and Other Hardware

- 5.2.2 Software Technology

- 5.2.2.1 Machine Learning

- 5.2.2.2 Deep Learning

- 5.2.2.3 Natural Language Processing

- 5.2.2.4 Computer Vision

- 5.2.3 Services

- 5.2.3.1 Managed Services

- 5.2.3.2 Professional Services

- 5.2.1 Hardware

- 5.3 By Tier Standard

- 5.3.1 Tier III

- 5.3.2 Tier IV

- 5.4 By End-user Industry

- 5.4.1 IT and ITES

- 5.4.2 Internet and Digital Media

- 5.4.3 Telecom Operators

- 5.4.4 BFSI

- 5.4.5 Healthcare and Life Sciences

- 5.4.6 Manufacturing and Industrial IoT

- 5.4.7 Government and Defense

- 5.5 By Country

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 Malaysia

- 5.5.5 South Korea

- 5.5.6 Singapore

- 5.5.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Alibaba Cloud (Alibaba Group)

- 6.4.2 Tencent Cloud

- 6.4.3 Amazon Web Services

- 6.4.4 Microsoft Azure

- 6.4.5 Google Cloud

- 6.4.6 Huawei Technologies

- 6.4.7 NVIDIA Corp.

- 6.4.8 Advanced Micro Devices

- 6.4.9 Baidu Inc.

- 6.4.10 NTT Global Data Centers

- 6.4.11 Equinix Inc.

- 6.4.12 Digital Realty

- 6.4.13 STT GDC

- 6.4.14 GDS Holdings

- 6.4.15 Yotta Infrastructure

- 6.4.16 AirTrunk

- 6.4.17 OneAsia Network

- 6.4.18 Sunbird Software

- 6.4.19 Nlyte Software

- 6.4.20 Schneider Electric

- 6.4.21 Delta Electronics

- 6.4.22 Vertiv Group

- 6.4.23 Fuji Electric

- 6.4.24 Daikin Industries

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment