PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073466

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073466

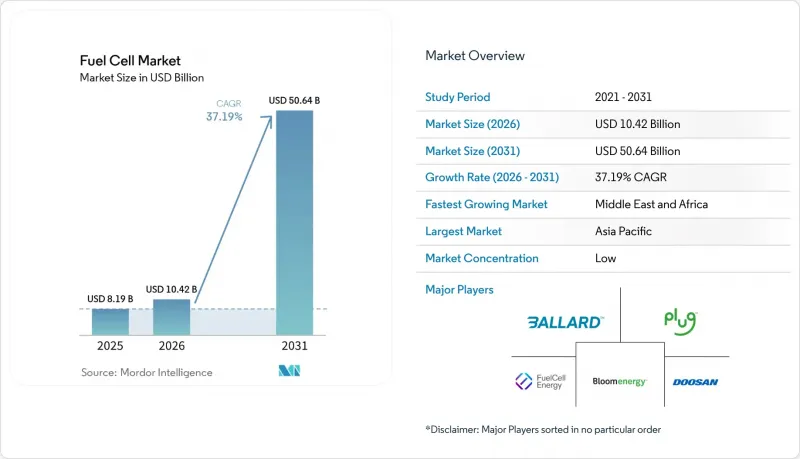

Fuel Cell - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the fuel cell market size was valued at USD 8.19 billion in 2025 and is estimated to grow from USD 10.42 billion in 2026 to reach USD 50.64 billion by 2031, at a CAGR of 37.19% during the forecast period (2026-2031).

This report is Segmented by Technology (Polymer Electrolyte Membrane Fuel Cell, Solid Oxide Fuel Cell, Alkaline Fuel Cell, and Others), Fuel Type (Hydrogen, Natural Gas, Ammonia, and Others), Application (Vehicular and Non-Vehicular), End-User Industry (Transportation, Utilities, Commercial and Industrial, and Others), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Global Fuel Cell Market Trends and Insights

Falling Costs of Green & Blue Hydrogen Generation

Electrolyzer capital expenditure declined to USD 2,100 per kilowatt in 2025 and is projected to hit USD 1,494 by 2030, pushing levelized hydrogen prices below USD 2 per kilogram in solar-rich zones. This trajectory narrows the parity gap with diesel and natural gas, unlocking new opportunities for forklifts, telecom towers, and distributed generation. Blue hydrogen at USD 1.50-2.50 per kilogram remains viable where low-cost gas is available, offering a bridge until renewable supply scales. Sovereign-backed projects such as Saudi Arabia's 600-tons-per-day NEOM complex de-risk early giga-scale facilities and create export benchmarks. Complementary renewable curtailment (California shed 2.4 TWh in 2024) provides negative-priced electricity windows that further lower hydrogen costs. Together, these trends strengthen fuel cell market economics across mobility and stationary use cases.

Automaker Commitments to FCEVs in Asia-Pacific

Toyota targets 75,000 annual fuel cell units by 2030, and Hyundai is building a KRW 930 billion plant aiming for 30,000 units a year by 2027. These moves signal long-term confidence despite near-term retail softness; South Korean FCEV sales fell 27.2% in H1 2025. Third-generation Toyota stacks doubled durability to 10,000 hours and cut platinum loadings by 30%, trimming total cost of ownership for heavy trucks. Chinese provincial incentives of up to RMB 300,000 per vehicle partially offset the national subsidy phase-out, keeping captive bus and logistics fleets in play. Overall, committed production capacity anchors supply-chain investment and propels the fuel cell market toward scale.

Scarcity of Hydrogen Refueling Infrastructure Outside Japan & South Korea

Japan operates 160 stations and South Korea 200, while the United States fields just 60, nearly all in California, and Europe tallies 250, with 40% in Germany. This uneven build-out confines passenger cars to fleet and pilot regions, suppressing broader adoption. China has 500 stations, but geography skews to coastal hubs, leaving inland provinces underserved. Capital costs of USD 2-4 million per site and high delivered hydrogen prices keep private investors cautious. California's temporary closure of 15 stations during supply shortages in 2024 damaged consumer confidence, illustrating fragility at early rollout stages.

Other drivers and restraints analyzed in the detailed report include:

- Government Zero-Emission Mandates in Heavy-Duty Transport

- Demand for Long-Duration Backup Power in Data Centers

- PGM & Nickel Price Volatility Inflating Stack Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polymer electrolyte membrane designs delivered 70.1% of 2025 revenue by virtue of automotive dominance. However, solid oxide solutions are expected to realize a 48.1% CAGR to 2031, twice the pace of PEM, as utilities value 60% electrical efficiency and fuel flexibility. Bloom Energy's platform operates on natural gas today and can transition to 100% hydrogen, lowering infrastructure hurdles. Alkaline systems hold a 4.2% share, confined to aerospace and submarine projects. Phosphoric acid, molten carbonate, and direct-methanol cells comprise the remainder but face competition from gas engines and lithium-ion storage. Innovations such as Ceres Power's steel-cell architecture, which reduces manufacturing cost by 40%, are widening technology choices in the fuel cell market.

Hydrogen supplied 65.3% of 2025 demand, undergirded by existing production infrastructure and broad stack compatibility. Natural-gas-derived hydrogen supports 26.9% of installations, mostly within North American stationary SOFC arrays, where pipeline availability lowers delivered costs. Ammonia, at an 8% baseline, is positioned for a 51.8% CAGR as maritime operators pivot toward zero-carbon bunkers. NYK Line and Samsung Heavy Industries expect to deploy ammonia-fueled SOFC vessels by 2028, leveraging a global ammonia trade network. Methanol and biogas occupy niche roles; each must overcome efficiency and impurity challenges before scaling within the wider fuel cell market.

Complete Report Scope:

- By Technology

- Polymer Electrolyte Membrane Fuel Cell (PEMFC)

- Solid Oxide Fuel Cell (SOFC)

- Alkaline Fuel Cell (AFC)

- Others [Phosphoric Acid Fuel Cell (PAFC), Molten Carbonate Fuel Cell (MCFC), Direct Methanol Fuel Cell (DMFC)]

- By Fuel Type

- Hydrogen

- Natural Gas/Methane

- Ammonia

- Others (Methanol, Biogas)

- By Application

- Vehicular (Passenger Cars, Buses & Coaches, Trucks, Material Handling Equipment, Rail, Marine Vessels)

- Non-Vehicular (Stationary Power, Portable Power, Micro-Combined Heat & Power)

- By End-User Industry

- Transportation

- Utilities

- Commercial and Industrial

- Others (Defense, Residential)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Spain

- NORDIC Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Geography Analysis

Asia-Pacific secured 57.5% of revenue in 2025 and is forecast to compound at a 36.8% CAGR through 2031. Japan's 160 refueling stations and 400,000 residential units spearhead adoption, while South Korea's KRW 500 billion hydrogen roadmap backs domestic suppliers. China's 500-station network and provincial subsidies sustain bus and logistics fleets amid retail softness. India and Southeast Asia trail in infrastructure, yet Australia's renewable surplus positions it as a future export hub. Divergent OEM strategies - with Toyota expanding while Honda scales back - underscore uneven market confidence but collectively reinforce regional leadership within the fuel cell market.

North America accounted for 22.3% revenue in 2025 and is expected to grow at a 34.2% CAGR. California anchors infrastructure with 60 stations and USD 240,000 vehicle vouchers, complemented by the federal USD 3-per-kilogram hydrogen production credit. Plug Power's forklift ecosystem dominates material handling, while Nikola targets long-haul freight. Canada's 40% investment credit leverages hydro resources for green hydrogen, yet station networks outside Vancouver and Toronto remain sparse. Mexico's early initiatives focus on cross-border trucking corridors. Policy continuity and electrolyzer cost declines will shape the region's trajectory.

Europe held a 15.8% share in 2025. Germany's 100 stations and IPCEI Hy2Tech funding underpin leadership, while Regulation 2024/1610 accelerates truck adoption. Nordic countries leverage renewable surpluses for export-oriented green hydrogen. Alstom's trains in Lower Saxony and Lombardy validate rail traction. The UK and France trail in deployment density, reflecting fragmented strategies. The Middle East and Africa, at 4.4% share, will grow fastest at 38.7% CAGR, propelled by the USD 8.4 billion NEOM and USD 1 billion Masdar-ADNOC complexes that target 2026-2027 commissioning. South America, at a 2.5% share, remains an early stage, with Chile and Brazil positioning as export suppliers rather than domestic consumers.

- Ballard Power Systems Inc.

- Plug Power Inc.

- FuelCell Energy Inc.

- Bloom Energy Corporation

- Doosan Fuel Cell Co., Ltd.

- Cummins Inc. (Hydrogenics)

- Toshiba Energy Systems & Solutions Corp.

- Panasonic Corporation

- Horizon Fuel Cell Technologies Pte. Ltd.

- Intelligent Energy Ltd.

- Nuvera Fuel Cells, LLC

- SFC Energy AG

- Mitsubishi Power Ltd.

- Hyundai Mobis Co., Ltd.

- Toyota Motor Corporation

- Nikola Corporation

- Ceres Power Holdings plc

- Ballard Motive Solutions Ltd.

- PowerCell Sweden AB

- AFC Energy plc

- Advent Technologies Holdings Inc.

- Gencell Ltd.

- Proton Motor Power Systems plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Recent Trends & Developments

- 4.3 Market Drivers

- 4.3.1 Falling Costs of Green & Blue Hydrogen Generation

- 4.3.2 Automaker Commitments to FCEVs in Asia-Pacific

- 4.3.3 Government Zero-Emission Mandates in Heavy-Duty Transport (NA & EU)

- 4.3.4 Demand for Long-Duration Backup Power in Data Centers

- 4.3.5 Maritime Decarbonization Targets Accelerating Fuel Cell Adoption

- 4.3.6 Corporate Net-Zero Investment into On-Site Distributed Generation

- 4.4 Market Restraints

- 4.4.1 Scarcity of Hydrogen Refueling Infrastructure Outside JP & KR

- 4.4.2 PGM & Nickel Price Volatility Inflating Stack Costs

- 4.4.3 SOFC Performance Degradation in Maritime High-Sulfur Environments

- 4.4.4 Certification Gaps in US Building Codes Slowing Stationary Installations

- 4.5 Supply-Chain Analysis

- 4.6 Regulatory Outlook

- 4.7 Technological Outlook

- 4.8 Porte's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products & Services

- 4.8.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Polymer Electrolyte Membrane Fuel Cell (PEMFC)

- 5.1.2 Solid Oxide Fuel Cell (SOFC)

- 5.1.3 Alkaline Fuel Cell (AFC)

- 5.1.4 Others [Phosphoric Acid Fuel Cell (PAFC), Molten Carbonate Fuel Cell (MCFC), Direct Methanol Fuel Cell (DMFC)]

- 5.2 By Fuel Type

- 5.2.1 Hydrogen

- 5.2.2 Natural Gas/Methane

- 5.2.3 Ammonia

- 5.2.4 Others (Methanol, Biogas)

- 5.3 By Application

- 5.3.1 Vehicular (Passenger Cars, Buses & Coaches, Trucks, Material Handling Equipment, Rail, Marine Vessels)

- 5.3.2 Non-Vehicular (Stationary Power, Portable Power, Micro-Combined Heat & Power)

- 5.4 By End-User Industry

- 5.4.1 Transportation

- 5.4.2 Utilities

- 5.4.3 Commercial and Industrial

- 5.4.4 Others (Defense, Residential)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Malaysia

- 5.5.3.6 Thailand

- 5.5.3.7 Indonesia

- 5.5.3.8 Vietnam

- 5.5.3.9 Australia

- 5.5.3.10 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Ballard Power Systems Inc.

- 6.4.2 Plug Power Inc.

- 6.4.3 FuelCell Energy Inc.

- 6.4.4 Bloom Energy Corporation

- 6.4.5 Doosan Fuel Cell Co., Ltd.

- 6.4.6 Cummins Inc. (Hydrogenics)

- 6.4.7 Toshiba Energy Systems & Solutions Corp.

- 6.4.8 Panasonic Corporation

- 6.4.9 Horizon Fuel Cell Technologies Pte. Ltd.

- 6.4.10 Intelligent Energy Ltd.

- 6.4.11 Nuvera Fuel Cells, LLC

- 6.4.12 SFC Energy AG

- 6.4.13 Mitsubishi Power Ltd.

- 6.4.14 Hyundai Mobis Co., Ltd.

- 6.4.15 Toyota Motor Corporation

- 6.4.16 Nikola Corporation

- 6.4.17 Ceres Power Holdings plc

- 6.4.18 Ballard Motive Solutions Ltd.

- 6.4.19 PowerCell Sweden AB

- 6.4.20 AFC Energy plc

- 6.4.21 Advent Technologies Holdings Inc.

- 6.4.22 Gencell Ltd.

- 6.4.23 Proton Motor Power Systems plc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment