PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073478

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073478

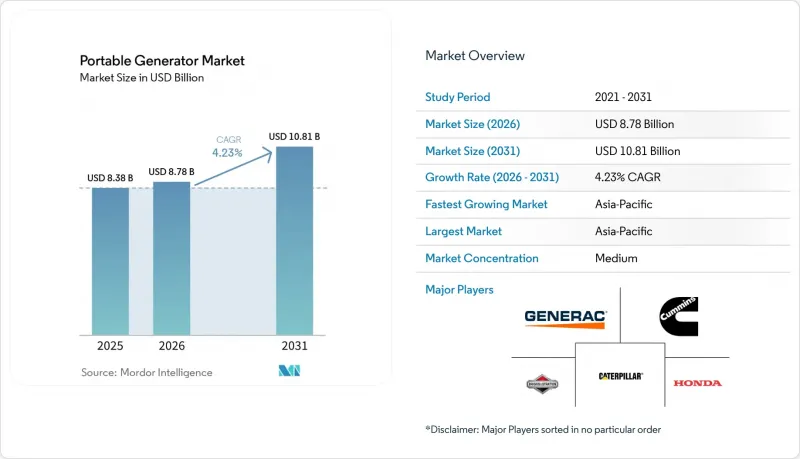

Portable Generator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the portable generator market size is expected to increase from USD 8.38 billion in 2025 to USD 8.78 billion in 2026 and reach USD 10.81 billion by 2031, growing at a CAGR of 4.23% over 2026-2031.

This report is Segmented by Fuel Type (Gasoline, Diesel, Dual-Fuel, LPG/Propane, and Solar-Integrated), Power Rating (Below 5 KW, 5 To 10 KW, and Above 10 KW), Technology (Conventional and Inverter), Application (Emergency/Stand-by, Prime/Continuous, and Recreational/Outdoor), End User (Residential, Commercial, and Industrial), and Geography (North America, Europe, Asia-Pacific, South America, and More).

Global Portable Generator Market Trends and Insights

Increasing Frequency of Power Outages & Grid Instability

Climate-driven storms, drought-strained hydropower, and utility de-energization events are lengthening outage hours, elevating the value of on-site generation. U.S. households endured 8.2 outage hours in 2024, up 27% from 2019, while Texas and California accounted for 40% of national downtime. India recorded 6.8 billion customer-hours of load-shedding during fiscal 2024-2025, with Uttar Pradesh, Bihar, and Jharkhand hardest hit. Brazil's outage duration rose to 14.3 hours in 2024 amid record heat and drought-hit dams. South Africa imposed stage-4 and stage-5 load-shedding on 118 days in 2024, driving 2.1 GW of incremental standby capacity, 35% of which involved portable units. Alongside steep insurance deductibles for spoiled inventory and frozen pipes, these trends are broadening the portable generator market beyond traditional hurricane-prone zones.

Rapid Growth in Residential Backup-Power Demand

Mortgage lenders now require backup-power attestations in FEMA flood and wildfire zones, embedding generator costs into closing fees. Remote work intensifies outage pain points: 28% of U.S. employees work from home at least three days weekly and cite power reliability as a top-three relocation factor. Germany's KfW financed EUR 87 million (USD 95 million) of home generator and battery upgrades for rural households in 2024. Australia's Clean Energy Regulator found that 18% of 2024 rooftop-solar installs included a generator-ready hybrid inverter. Collectively, subsidies, insurance incentives, and telework economics lift attach rates above historical norms.

Stringent Emission Regulations on Small Engines

The U.S. EPA's Tier 4 rules for sub-19 kW spark-ignition engines took effect in January 2025, forcing three-way catalysts and closed-loop fueling that add USD 80-120 per unit. EU Stage V raises particulate-number limits, driving diesel particulate filters and SCR on portable diesels. China's National IV standards mandate EFI and onboard diagnostics from July 2025. Japan now requires Tier-4-equivalent engines in all public-sector procurements. Compliance costs squeeze entry pricing and accelerate the shift toward inverter and hybrid-solar architectures.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Construction Activities in Emerging Economies

- Recreational Vehicle & Outdoor Leisure Boom

- Adoption of Residential Battery-Storage Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gasoline units retained 44.5% portable generator market share in 2025, benefiting from widespread fuel availability and USD 400-1,200 pricing, yet solar-integrated hybrids are growing 9.7% CAGR on off-grid telecom and RV demand. Diesel models face weight and cost penalties from Stage V after-treatment, losing ground outside heavy-duty sites. Dual-fuel gasoline-propane designs win rural U.S. buyers who prize 18-month propane shelf life and lower carbon intensity.

Hybrid solar-battery-generator systems slash diesel use by up to 80% at African tower sites, trimming annual fuel logistics by USD 3,200 per node. Power-station brands such as Jackery and EcoFlow shipped 890,000 solar-ready units in 2024, combining foldable PV with 1-3 kWh batteries. Levelized energy costs drop below USD 0.30/kWh in high-insolation zones, a 40% edge over diesel-only setups.

The 5-10 kW class represented 47.9% of the portable generator market size in 2025, addressing whole-home backup and food-truck power, yet sub-5 kW units are advancing 6.1% CAGR on apartment and tailgating use cases. Units above 10 kW remain industrial staples but face rental-fleet substitution.

Urban decibel caps, such as Los Angeles' 60 dBA at 7 m, disqualify most open-frame models, pushing consumers toward compact inverters under 58 dBA. Tokyo and Singapore impose similar nighttime limits, spurring OEM acoustic enclosures. A 7 kW inverter weighing 55 kg meets 80% of single-family loads without permanent transfer switches, balancing portability with capacity.

Complete Report Scope:

- By Fuel Type

- Gasoline

- Diesel

- Dual-Fuel (Gasoline-Propane)

- LPG/Propane

- Solar-Integrated

- By Power Rating

- Below 5 kW

- 5 to 10 kW

- Above 10 kW

- By Technology

- Conventional

- Inverter

- By Application

- Emergency/Stand-by

- Prime/Continuous

- Recreational/Outdoor

- By End User

- Residential

- Commercial

- Industrial

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Spain

- NORDIC Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Geography Analysis

Asia-Pacific controlled 38.6% of 2025 revenue, and the portable generator market size in the region will grow at a 4.9% CAGR through 2031 on infrastructure and rural-telecom build-outs. India logged 6.8 billion outage-hours, spurring residential and SME purchases, while China deployed 87,000 rural 5G base stations, 41% powered by solar-diesel hybrids. ASEAN PPP pipelines worth USD 89 billion specify portable units for bridge and tunnel works.

North America ranks second, anchored by the United States' 142 million single-family homes. Outage hours rose to 8.2 in 2024, elevating attach rates, while Canada's northern mines rely on hybrid gensets to offset USD 2.50-per-liter air-lifted diesel. Mexico's near-shoring wave pushes construction demand, with 68% of industrial-park tenders in 2024 requiring temporary generators.

Europe's growth hinges on emission-compliant inverters and hybrids amid high diesel costs. Germany's rural-resilience loans covered 14,300 households in 2024, while Storm Arwen-style blackouts prompted U.K. compensation reforms that favor onsite backup. France warns of winter peak constraints, driving industrial standby installs, whereas Nordic markets see modest recreational growth tied to camper-van adoption.

- Generac Holdings Inc.

- Honda Motor Co. Ltd.

- Caterpillar Inc.

- Briggs & Stratton LLC

- Cummins Inc.

- Kohler Co.

- Yamaha Motor Co. Ltd.

- Atlas Copco AB

- Wacker Neuson SE

- Champion Power Equipment Inc.

- Westinghouse Electric Corp.

- Doosan Portable Power

- Hyundai Power Equipment Co.

- FG Wilson (Caterpillar UK)

- Perkins Engines Company Ltd.

- DuroMax Power Equipment

- Wen Products

- Jackery Inc. (Solar)

- EcoFlow Tech Ltd. (Battery)

- Anker Innovations Ltd. (Battery)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing frequency of power outages & grid instability

- 4.2.2 Rapid growth in residential backup-power demand

- 4.2.3 Expanding construction activities in emerging economies

- 4.2.4 Recreational vehicle & outdoor leisure boom

- 4.2.5 Growth of home-based micro-data-centres (edge)

- 4.2.6 Hybrid solar-diesel use at off-grid telecom towers

- 4.3 Market Restraints

- 4.3.1 Stringent emission regulations on small engines

- 4.3.2 Adoption of residential battery storage systems

- 4.3.3 Urban noise-zoning curfews on generator run-time

- 4.3.4 Lithium portable power-stations cannibalising <2 kW sales

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Investment Analysis

5 Market Size & Growth Forecasts

- 5.1 By Fuel Type

- 5.1.1 Gasoline

- 5.1.2 Diesel

- 5.1.3 Dual-Fuel (Gasoline-Propane)

- 5.1.4 LPG/Propane

- 5.1.5 Solar-Integrated

- 5.2 By Power Rating

- 5.2.1 Below 5 kW

- 5.2.2 5 to 10 kW

- 5.2.3 Above 10 kW

- 5.3 By Technology

- 5.3.1 Conventional

- 5.3.2 Inverter

- 5.4 By Application

- 5.4.1 Emergency/Stand-by

- 5.4.2 Prime/Continuous

- 5.4.3 Recreational/Outdoor

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Spain

- 5.6.2.5 NORDIC Countries

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN Countries

- 5.6.3.6 Australia and New Zealand

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Colombia

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Egypt

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Generac Holdings Inc.

- 6.4.2 Honda Motor Co. Ltd.

- 6.4.3 Caterpillar Inc.

- 6.4.4 Briggs & Stratton LLC

- 6.4.5 Cummins Inc.

- 6.4.6 Kohler Co.

- 6.4.7 Yamaha Motor Co. Ltd.

- 6.4.8 Atlas Copco AB

- 6.4.9 Wacker Neuson SE

- 6.4.10 Champion Power Equipment Inc.

- 6.4.11 Westinghouse Electric Corp.

- 6.4.12 Doosan Portable Power

- 6.4.13 Hyundai Power Equipment Co.

- 6.4.14 FG Wilson (Caterpillar UK)

- 6.4.15 Perkins Engines Company Ltd.

- 6.4.16 DuroMax Power Equipment

- 6.4.17 Wen Products

- 6.4.18 Jackery Inc. (Solar)

- 6.4.19 EcoFlow Tech Ltd. (Battery)

- 6.4.20 Anker Innovations Ltd. (Battery)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment